As the mercury climbs and summer approaches, millions of Americans will reach for a cold beer to cap off a long day. It is a quintessential American ritual, a staple of backyard barbecues, ballgames, and quiet evenings. Yet, for the average consumer, the sticker price on a six-pack is often a mystery of economic engineering. While the ingredients—water, hops, barley, and yeast—are the soul of the brew, they are far from the most expensive component of the final price. That title belongs to the government.

In the United States, taxes represent the single largest ingredient in beer. When consumers reach for their wallet at the checkout counter, they are unknowingly paying a complex, multi-layered tribute to local, state, and federal coffers. This hidden tax burden, often amounting to more than 40 percent of the retail price, is a testament to an archaic, Byzantine regulatory framework that affects everyone from the smallest craft brewer to the largest global distributor.

The Anatomy of the Beer Tax: Beyond the Retail Price

To the casual observer, the price of beer is a simple reflection of supply and demand. However, the reality is far more intricate. The tax burden on beer is a composite of federal excise taxes, state-level excise taxes, municipal levies, and a dizzying array of secondary fees.

The Federal Layer

At the federal level, the Alcohol and Tobacco Tax and Trade Bureau (TTB) dictates the baseline. The excise tax on beer is tiered, designed to account for production volume. Small domestic brewers, defined by their ability to produce under 60,000 barrels annually, pay a reduced rate of $0.113 per gallon. Conversely, large-scale imports or massive domestic production operations face a steeper rate of $0.581 per gallon.

The State and Local Patchwork

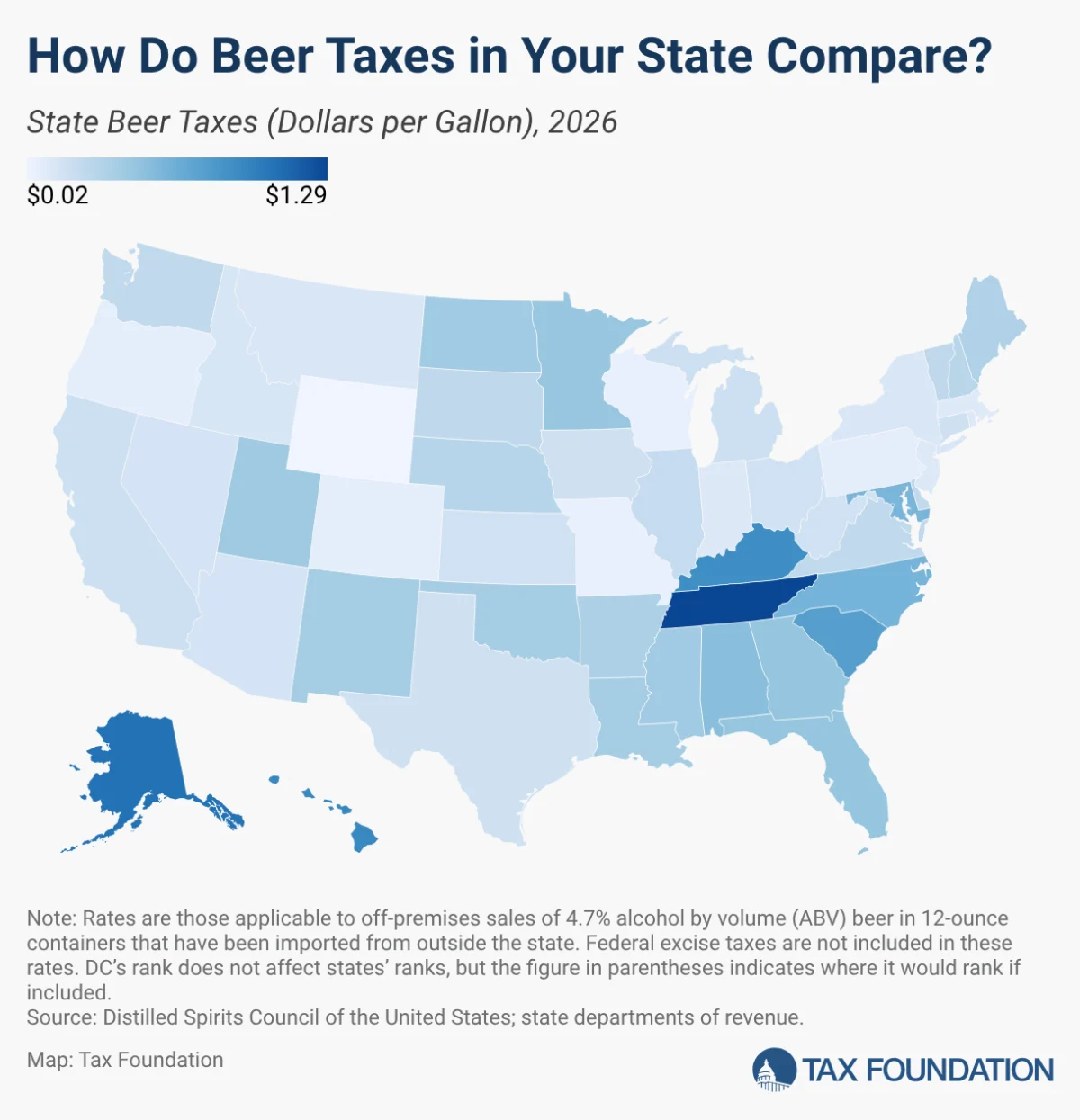

The federal rate is merely the starting line. Every one of the 50 states, plus the District of Columbia, levies its own excise tax on top of the federal mandate. These state taxes are rarely uniform. They are influenced by a state’s fiscal priorities, regional politics, and, in some cases, protectionist attitudes toward local industries.

For instance, the tax environment is starkly different depending on one’s zip code. Tennessee currently holds the title for the highest beer tax burden in the nation, at $1.287 per gallon. Alaska and Hawaii follow closely, with rates of $1.07 and $0.93 per gallon, respectively. On the other end of the spectrum, Wyoming offers a significantly lower barrier to entry, taxing at just $0.019 per gallon, with Missouri and Wisconsin also keeping their tax burdens in the $0.06 range.

A Chronology of Policy and Change

The regulation of alcohol has always been a contentious issue in American history, characterized by the pendulum swing between moral regulation and economic pragmatism.

- Pre-Prohibition and the Tax Foundation: Since the inception of modern federal tax codes, beer has been a primary target for "sin taxes." The ability to generate consistent revenue from a popular consumer good made alcohol a pillar of the federal budget.

- The Modern Era: The latter half of the 20th century saw the ossification of state-level tax structures. Many of the laws currently on the books were drafted in the 1970s and 80s, long before the craft beer revolution fundamentally changed the industry’s dynamics.

- 2020–2025: Shifts in Legislation: Recent years have seen states attempting to modernize or adjust these rates. In 2025, the industry faced significant pressure from tariff-related cost increases on imported aluminum and raw ingredients. In response, some states have moved to support local economies. For example, Missouri recently signed legislation to cut taxes on beer manufactured within the state to a mere $0.02 per gallon, a move intended to foster regional economic development and keep local breweries competitive.

- 2026 and Beyond: Looking toward the 2026 fiscal year, the conversation is shifting toward "tax neutrality." Policymakers are increasingly being pressured by industry advocates to abandon the rigid, categorical system in favor of taxing alcohol by volume (ABV), a move intended to simplify the tax code and prevent the penalization of innovative, low-alcohol, or non-alcoholic products that are currently gaining market share.

The Complexity of Categorical Taxation

One of the most persistent issues in the current tax framework is the "categorical" system. Under this model, the law treats beer, wine, and spirits as distinct legal entities, regardless of their actual alcohol content.

This creates significant market distortions. For example, Idaho treats beer with an ABV over 5 percent as legally equivalent to wine, triggering a tax rate that is triple the standard beer rate—$0.45 per gallon compared to $0.15. Virginia utilizes an even more granular system, assessing tax based on the size of the container, creating a administrative burden for retailers and wholesalers who must track inventory with near-surgical precision.

The "Hidden" Nature of the Cost

Perhaps the most deceptive aspect of these taxes is that they are rarely seen by the consumer. Unlike a sales tax, which is added at the register and clearly marked on a receipt, excise taxes are "baked in." They are levied on the manufacturer or the wholesaler and then passed down the supply chain. Because these costs are embedded in the wholesale price, the average consumer remains blissfully unaware that they are paying a heavy premium to the government with every sip.

Implications for the Future: A Shrinking Market?

The beer industry is currently navigating a period of unprecedented volatility. Beyond the regulatory burden, there is a clear shift in consumer behavior. Younger demographics, particularly Gen Z and Millennials, are increasingly moving toward health-conscious, low-alcohol, or "sober-curious" lifestyles.

The Fiscal Trap for States

State governments that have come to rely on beer taxes as a reliable source of general revenue are facing a "fiscal cliff." As the popularity of traditional, high-taxed beer wanes, and as the market fragments into low-ABV categories that may fall under different tax rules, the revenue streams are becoming increasingly unpredictable.

Furthermore, inflation and currency debasement are eating away at the real value of ad quantum (fixed amount) taxes. When states set a tax at a fixed number of cents per gallon, that money buys less and less for the state government as the years go by. When they try to offset this with ad valorem (percentage-based) taxes, they find their revenue subject to the volatile whims of consumer behavior.

The Call for Modernization

Industry experts and the Tax Foundation have repeatedly argued for a fundamental modernization of the system. The current framework, which treats a 4.7 percent ABV lager as a fundamentally different taxable good than a similarly potent craft cider or seltzer, is increasingly viewed as an obstacle to innovation.

"Taxing according to actual alcohol content," notes one industry advocate, "would make the broader alcohol tax system simpler and more neutral. It removes the guesswork for manufacturers and ensures that consumers aren’t being taxed based on outdated definitions of what a ‘beer’ is."

Conclusion: The Path Forward

The American beer industry is at a crossroads. While it remains one of the most cherished sectors of the national economy, it is being throttled by a regulatory and tax apparatus that has failed to evolve alongside it.

As we look toward the future, the challenge for policymakers is twofold: they must create a system that is transparent enough for consumers to understand the true cost of their purchases, and flexible enough to accommodate the rapidly changing landscape of the beverage industry. Without reform, the "cold beer at the end of a long day" may become an increasingly expensive luxury, not because of the quality of the brew, but because of the archaic layers of taxation that surround it.

For now, the next time you hold a cold one, remember: you aren’t just paying for the beer. You are paying for a complex, century-old legacy of government policy that has, quite literally, become the most expensive ingredient in your glass.