In the modern financial landscape, the primary obstacle to personal prosperity is rarely a lack of information or the complexity of investment vehicles. Rather, it is the fundamental fallibility of human decision-making. As financial behavioralists have long argued, the "willpower gap"—the distance between what we intend to do with our money and what we actually do—is where most wealth-building efforts collapse.

The solution is not more discipline; it is the strategic removal of the human element from the equation. By shifting from manual management to a system of total financial automation, individuals can transform good intentions into guaranteed, mathematical outcomes.

The Failure of Manual Management: The "Random Tuesday" Problem

Most personal finance plans do not fail because of poor arithmetic. They fail on a "random Tuesday" when the friction of daily life intervenes. When an individual relies on their own memory to transfer funds to a high-yield savings account or initiate a manual contribution to an IRA, they introduce a point of failure.

The Psychology of Decision Fatigue

Every manual financial move requires a conscious decision. Behavioral economics suggests that we possess a finite reservoir of "decision energy" each day. When we are exhausted, stressed, or distracted, our brain naturally seeks the path of least resistance. If that path involves leaving money in a checking account—where it is easily accessible for impulsive spending—the brain will choose that route every time.

Skipping a single manual transfer might seem inconsequential. However, it creates a psychological precedent. Once the decision to "skip just this once" is made, the barrier to skipping the next month becomes significantly lower. Automation eliminates this moral hazard entirely. By removing the need for a decision, you remove the possibility of a "wrong" decision.

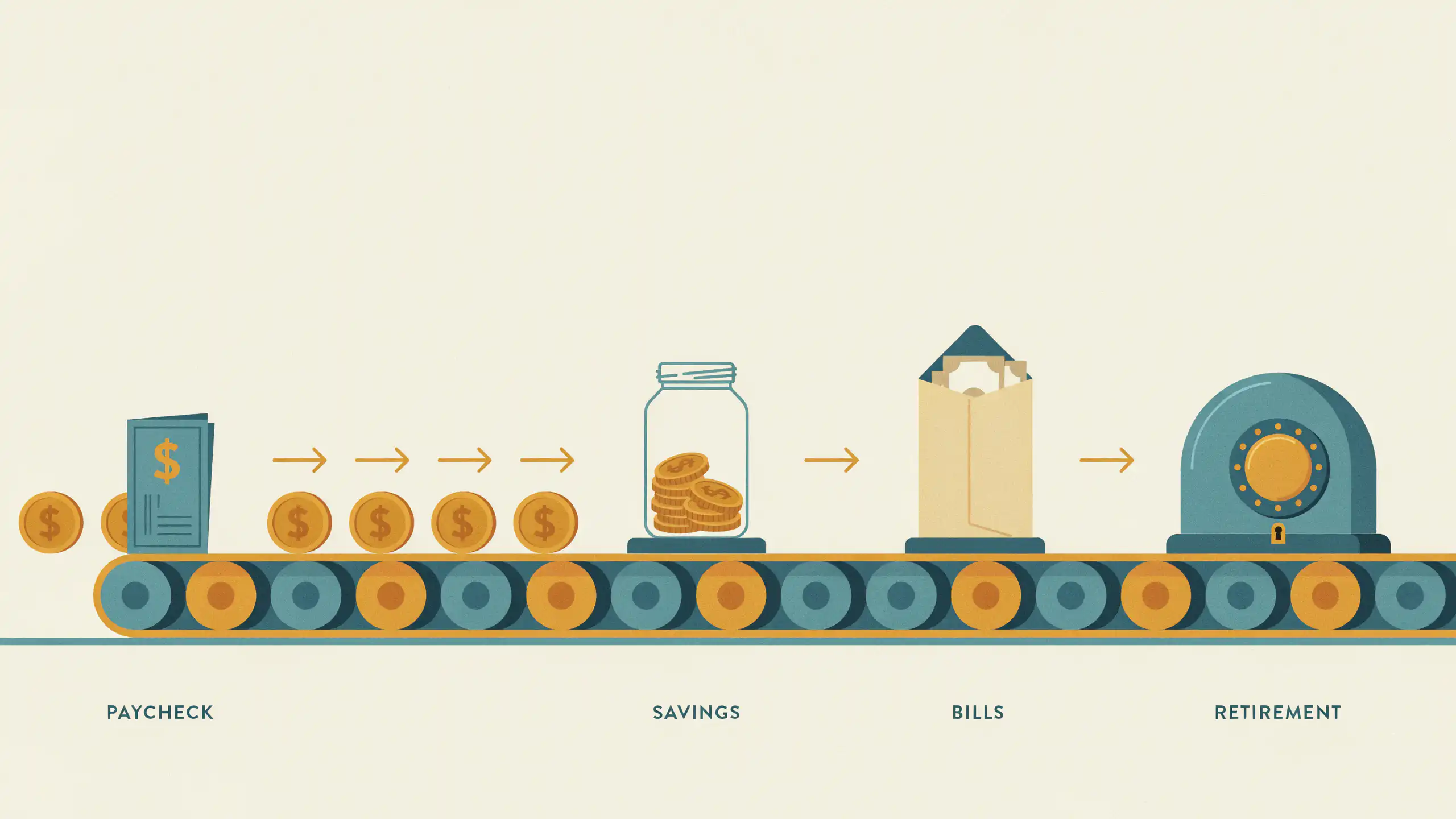

Chronology of Financial Automation: From Payroll to Portfolio

The concept of "paying yourself first" has been a cornerstone of fiscal advice for decades, yet its implementation has evolved significantly with the advent of digital banking.

- The Pre-Digital Era: Historically, saving required a physical trip to the bank or a manual check deposit. Success was entirely dependent on individual character and the ability to delay gratification.

- The Payroll Deduction Revolution: The introduction of automated payroll deposits for 401(k) accounts proved that when money is diverted before it ever reaches a checking account, it is rarely missed. This "out of sight, out of mind" phenomenon is the bedrock of modern wealth accumulation.

- The Current Digital Ecosystem: Today, consumers have access to sophisticated banking APIs and automated clearing house (ACH) scheduling. We are now in an era where an entire financial ecosystem can be built to operate on "autopilot," effectively decoupling the act of earning from the act of spending.

Supporting Data: The Efficiency of Systematized Savings

Data from behavioral finance studies consistently show that automated savers are significantly more likely to achieve their long-term goals than those who rely on manual budgeting.

The "Default Effect"

Research indicates that when individuals are automatically enrolled in savings or retirement plans (with an opt-out rather than an opt-in requirement), participation rates skyrocket. This is known as the "Default Effect." By setting your bank account to "default" to saving, you align your financial behavior with the most powerful force in human psychology: the tendency to accept the status quo.

The Buffer Strategy

A common concern regarding automation is the fear of overdrafts. However, this is easily mitigated by implementing a "buffer" strategy. By maintaining a fixed, static cushion in a checking account that is never touched—a "dead zone" of capital—individuals can ensure that even if a bill is slightly higher than expected, the automated transfers for savings and investments remain undisturbed.

Strategic Implementation: The Three Pillars of Automation

To build an automated financial architecture, one must focus on three core pillars. These should be timed to coincide with payday, ensuring that money is allocated to its purpose before it is ever mentally categorized as "spendable."

1. Automated Savings

Your emergency fund and short-term savings goals should be funded by an automated transfer immediately following the receipt of your paycheck. By treating your savings account like a non-negotiable monthly bill, you force your lifestyle to adapt to the remainder of your income, rather than trying to save whatever is left over at the end of the month.

2. Automated Bill Payments

Late fees and interest penalties are the silent killers of wealth. Automating your recurring bills—utilities, rent, subscriptions, and credit card payments—ensures you maintain a pristine credit score and avoid the "leakage" of unnecessary fees.

3. Automated Retirement Contributions

Whether through a workplace 401(k) or an individual IRA, these contributions should be automated at the source. This ensures that you are consistently buying into the market regardless of whether the market is up or down, effectively utilizing "dollar-cost averaging" to smooth out volatility over the long term.

Official Perspectives: The Expert Consensus

Financial planners and economists increasingly agree that "behavioral design" is more effective than traditional budgeting. While traditional advice focuses on spreadsheets and itemized lists, modern financial experts argue that the most effective budget is one that requires zero maintenance.

"Automation isn’t abandonment," notes the industry consensus. "It is the delegation of mundane, repetitive tasks to a system that doesn’t get tired, doesn’t get busy, and doesn’t forget." The goal is to move from a state of "active management"—which breeds stress and anxiety—to "passive oversight," where the individual simply monitors the system’s performance on a quarterly basis.

Implications: The Long-Term Wealth Effect

The implications of adopting a fully automated financial system are profound.

Scalability

One of the most significant advantages of an automated system is its scalability. As your income rises, you can adjust your automated contribution percentages with a single edit in your banking app. This prevents "lifestyle creep," where increased earnings are automatically swallowed by increased spending. By keeping the "save percentage" constant or increasing it, you ensure that your wealth grows in direct proportion to your career progression.

Freedom of Mind

Perhaps the greatest benefit is not the dollar amount in the account, but the cognitive freedom gained. When you stop worrying about whether you remembered to pay the electricity bill or if you set aside enough for your Roth IRA, you reclaim mental bandwidth. You stop being a "financial manager" and start being a "financial architect."

Quarterly Audits

Automation does not mean ignoring your finances entirely. A quarterly audit is essential to confirm that your system is still firing correctly and that your life circumstances—such as a marriage, a child, or a new job—are reflected in your settings. This "check-in" approach replaces the daily, exhausting grind of manual tracking with a healthy, manageable habit.

Conclusion

The pursuit of financial independence is not a sprint that requires peak performance every single day. It is a marathon that rewards consistency over intensity. By building a system that operates independently of your mood, your energy levels, or your schedule, you place your financial future on a trajectory that is almost impossible to derail.

Discipline is a test you have to retake every payday. A system passes that test for you, every time, on schedule. Spend ten minutes in your banking app tonight to set up your automations, and stop counting on the version of you who remembers to do it later. In the world of finance, the most successful strategy is the one that happens without you.