In the realm of personal finance, a persistent myth suggests that wealth is primarily a function of income. While a high salary certainly provides more fuel for the engine of prosperity, it is not the sole driver. Financial experts have long observed a phenomenon where two individuals with identical earnings arrive at vastly different net worths after a decade. The discrepancy rarely stems from luck or secret investment tips; rather, it is the result of the "Financial Order of Operations."

Most individuals approach money management with a disorganized, reactionary mindset—saving what is left after spending, paying off debt sporadically, and investing in whatever financial instrument happens to be trending. This "randomized" approach is fundamentally inefficient. By adopting a structured, prioritized sequence for every dollar earned, you can ensure that your capital is always working in its most advantageous capacity.

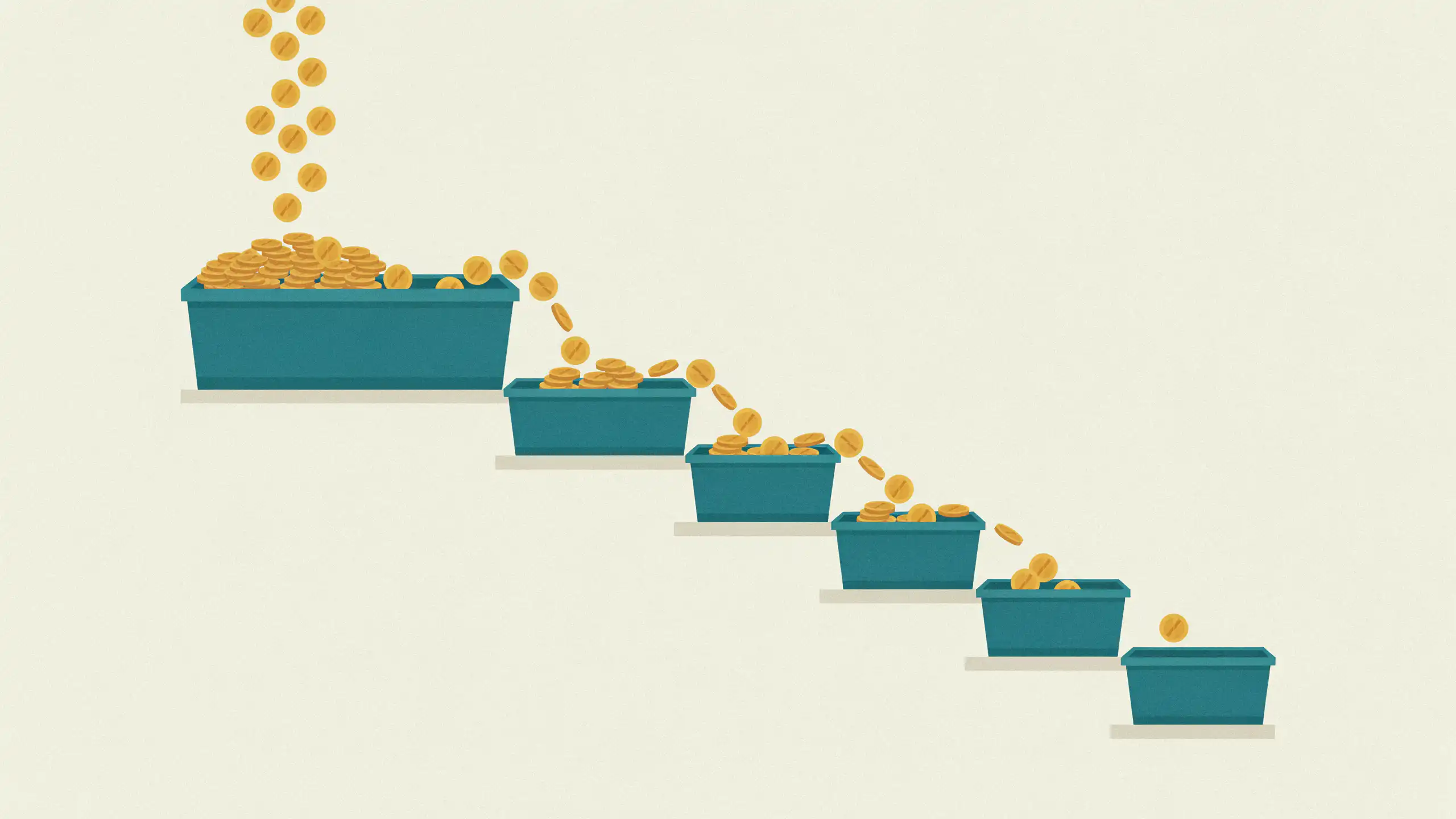

The Financial Hierarchy: A Six-Step Sequence

To optimize your net worth, you must stop viewing your finances as a collection of isolated accounts and start viewing them as a pipeline. Every dollar that enters your possession should be funneled through the following six steps in order.

1. The Starter Emergency Buffer

Before you consider aggressive debt repayment or market participation, you must secure a "starter" emergency fund. This is typically a small, liquid sum—often $1,000 to $2,000—held in a high-yield savings account. The purpose is not to cover a total loss of income, but to act as a shock absorber. Without this, the smallest unexpected bill—a flat tire or a broken appliance—forces you to lean on high-interest credit cards, effectively resetting your progress and trapping you in a cycle of interest payments.

2. Employer 401(k) Match

Once your buffer is established, the next priority is capturing "free money." Many employers offer a 401(k) match, where they contribute a percentage of your salary to your retirement account if you contribute your own funds. This represents an instant, guaranteed return on investment—often 50% to 100%. In the financial world, where the average annual stock market return is closer to 7-10%, passing up a 100% return is mathematically equivalent to walking away from a raise.

3. Eliminating High-Interest Debt

Debt is the silent killer of wealth. Specifically, "high-interest" debt—defined as any liability carrying an interest rate above 7% to 10%—must be prioritized. Credit card interest rates, which frequently exceed 20%, grow at a pace that almost no market investment can reliably match. Paying off a 20% credit card is effectively a guaranteed 20% return on your money. By retiring this debt, you stop the hemorrhage of interest that prevents your capital from compounding.

4. The Full Emergency Fund

With high-interest debt neutralized, you can transition from the "starter" buffer to a robust, fully funded emergency account. A rule of thumb is to maintain three to six months of essential living expenses. This fund serves as your personal insurance policy, granting you the stability to make career changes, weather economic downturns, or handle major life events without incurring new, high-cost debt.

5. Individual Retirement Accounts (IRAs)

Once your immediate risks are managed and high-cost debt is gone, you should maximize tax-advantaged accounts like a Roth or Traditional IRA. These vehicles allow your money to grow tax-free or tax-deferred, providing a massive advantage over the course of decades. If you have already secured your employer match, the IRA is the next most efficient tax-sheltered home for your long-term capital.

6. Taxable Brokerage Accounts and Long-Term Investing

Only after you have secured your buffer, captured your match, paid off high-interest debt, built a full safety net, and maxed out tax-advantaged retirement accounts should you consider taxable brokerage accounts. At this stage, your financial foundation is solidified, and your excess capital can be deployed into diversified market indices with a long-term horizon.

Supporting Data: The Cost of Improper Sequencing

The importance of this sequence is grounded in the reality of compound interest and the "drag" created by debt. Consider the opportunity cost: If an individual chooses to invest $500 per month into a brokerage account while simultaneously carrying a $10,000 credit card balance at 22% interest, they are making a losing trade.

The interest accrued on the debt will far outpace the capital gains realized in the brokerage account. Furthermore, the volatility of the stock market means that in a downturn, the investor could lose principal, whereas the debt interest remains a fixed, compounding liability. This is why financial advisors emphasize that the order of operations is not a suggestion—it is a mathematical necessity for wealth accumulation.

The Psychology of the "Pipeline"

Why do so many struggle with this? Behavioral finance experts suggest that human beings are wired for "immediate gratification over systematic optimization." We feel the urge to "invest" because it feels like building wealth, whereas paying off debt feels like a chore. However, clearing a 22% interest rate is, in practical terms, a better investment than almost any asset class available to the public.

The sequence also removes the emotional burden of decision-making. When a bonus, a tax refund, or a raise occurs, the temptation to spend is high. By adhering to the pipeline, you eliminate the deliberation process. You simply look at your current standing in the sequence, identify the next unfinished step, and direct the funds accordingly.

Implications for Future Net Worth

The implications of following this sequence are profound. Over a 30-year career, the difference between someone who haphazardly saves and someone who follows a strict order of operations can be hundreds of thousands of dollars—or even millions, depending on the starting salary and market conditions.

This strategy also provides a psychological benefit: the "peace of mind" that comes from knowing your money is being utilized optimally. When you know that your emergency fund is full, your high-interest debt is gone, and your retirement accounts are growing, you are shielded from the anxiety that typically accompanies financial volatility.

Navigating the "Multi-Tasking" Phase

It is important to clarify that this sequence is not necessarily a strict, linear "one-at-a-time" schedule. Life is rarely that binary. For many, the process involves a "staggered" approach. For example, while you are paying down high-interest debt, you should ideally continue contributing enough to your 401(k) to secure the employer match.

This is the only acceptable "overlap." Once the match is secured and the debt is gone, you move forward with the next step in the hierarchy. The only scenario that should be avoided at all costs is "skipping ahead." Attempting to build a luxury investment portfolio while high-interest credit card debt accumulates is a fundamental error that compromises your entire financial future.

Conclusion: The Path Forward

Wealth is not merely a product of what you earn; it is a product of where you place your earnings and in what order. By treating your financial life like a high-functioning system rather than a series of disconnected decisions, you transform your income into an engine of compounding growth.

The next time you find yourself with "extra" capital, resist the urge to act randomly. Check the sequence. Secure the match. Kill the debt. Build the safety net. Invest for the future. By following this hierarchy, you ensure that every dollar you earn works as hard as possible for your long-term success. The order matters more than the amount; master the order, and the amount will follow.