For generations, a wry observation has circulated through the hallowed halls of commodity trading: gold never truly moves; it simply changes the address of the vault in which it resides. For most of the modern era, that vault was almost invariably located in London. While gold might be mined in the rugged outback of Australia, refined in the pristine facilities of Switzerland, and purchased by a central bank in East Asia, the "nervous system" of the gold market—the clearing, settling, and pricing mechanisms—remained firmly anchored in the United Kingdom.

However, as we move through 2026, the global financial architecture is undergoing a tectonic shift. The "uncomfortable truth" that defined the 20th-century gold market is fraying. Driven by geopolitical realignment, the weaponization of reserve currencies, and the sheer volume of Asian demand, the center of gravity for the world’s most enduring asset is migrating. The next chapter of the gold story is no longer being written in the City of London; it is being drafted in Hong Kong, Shanghai, and Singapore.

The Rise of the Neutral Reserve

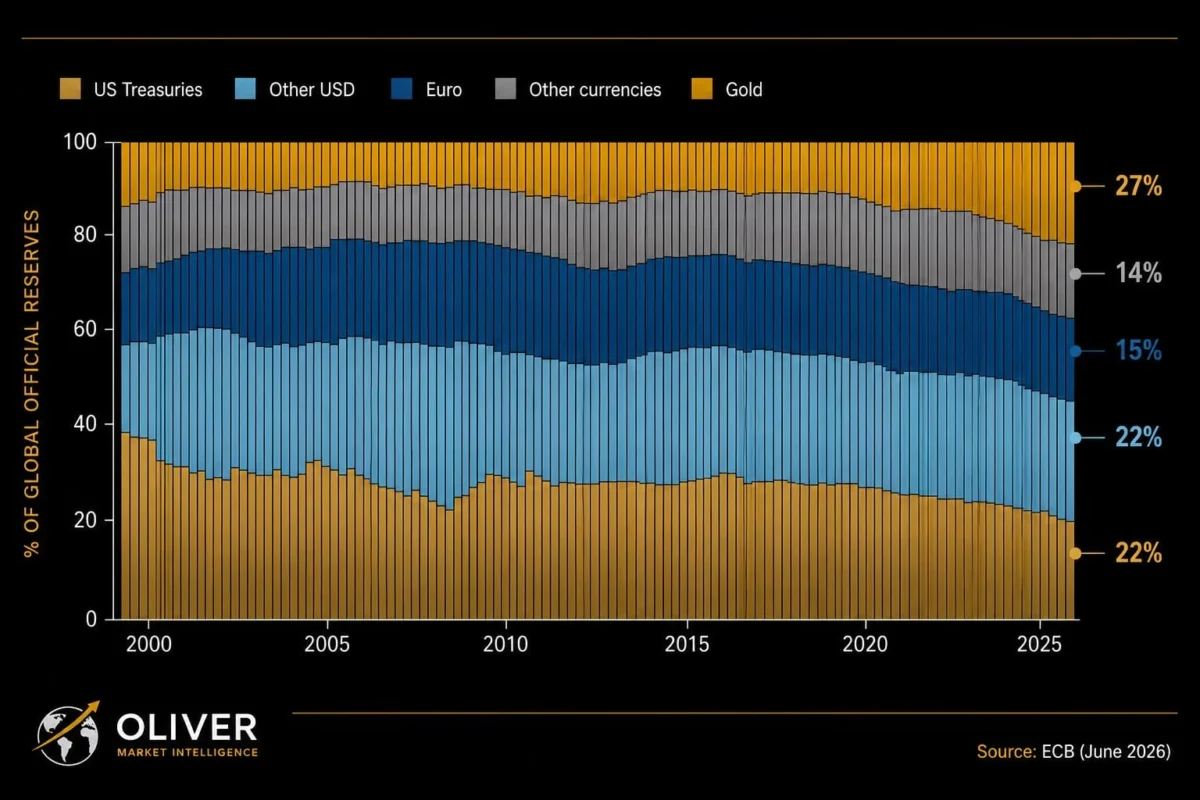

The most significant indicator of this shift is the changing composition of central bank reserves. According to data released by the European Central Bank (ECB) at the close of 2025, gold has officially overtaken U.S. Treasuries as the world’s primary reserve asset. Gold now accounts for 27% of global central bank reserves, compared to 22% for Treasuries.

This is not merely a tactical adjustment; it is a strategic retreat from the Western-led financial order. Collectively, central banks now hold over 36,000 tonnes of gold—a level of accumulation not seen since the height of the Bretton Woods era. The primary architects of this shift—China, India, Turkey, and Poland—are not buying gold to hedge against temporary inflation; they are buying it as an insurance policy against political volatility.

The freezing of Russia’s foreign exchange reserves in the wake of the 2022 Ukraine invasion served as a geopolitical "alarm bell." For central bankers, it transformed the definition of risk. Sovereign bonds, previously considered the bedrock of safety, were revealed to be vulnerable to political sanction. Gold, by contrast, has no issuer, no counterparty risk, and carries no dependency on the fiscal or foreign policy of a foreign power. In an increasingly fragmented world, gold has emerged as the ultimate neutral asset.

Chronology of a Market Transformation

The shift of the gold market away from the Atlantic axis was not an overnight phenomenon, but a process accelerated by two decades of evolving global trade patterns.

- 2008–2012 (The Post-Crisis Awakening): Following the Global Financial Crisis, central banks began a slow, deliberate pivot back toward bullion. The volatility of the dollar and the expansion of balance sheets in the West prompted developing economies to re-evaluate their reliance on fiat reserves.

- 2014–2020 (The Rise of Eastern Infrastructure): As physical gold demand began to dominate in Asia, the mismatch between physical flows and Western-centric pricing became glaring. China, through the Shanghai Gold Exchange (SGE), began asserting its role as a global price setter, moving beyond domestic consumption to influence international premiums.

- 2022–2024 (The Geopolitical Pivot): The freezing of Russian assets acted as a catalyst. Central bank buying reached decadal highs, with a noticeable trend of nations repatriating gold holdings or shifting storage toward jurisdictions viewed as geopolitically "safe" or neutral.

- 2025–2026 (The Infrastructure Migration): The current phase represents the move from holding to clearing. As Asian nations hold more physical gold, they are demanding the infrastructure to trade, settle, and clear that gold locally, reducing their reliance on the London Over-the-Counter (OTC) system.

The Plumbing of Power: Why Clearing Matters

To understand why this shift is profound, one must look past the price of gold and toward the "plumbing"—the clearing and settlement infrastructure. In the modern market, physical bars rarely move. Instead, ownership is transferred electronically through clearing systems, which net positions to reduce costs and increase liquidity.

Historically, the institutions that control this infrastructure hold the power. By controlling the ledger, London has maintained a gravitational pull that has kept global liquidity centered in the West for over a century. If you control the clearinghouse, you control where the market participants must congregate.

Hong Kong is currently challenging this monopoly. The Hong Kong Precious Metals Central Clearing Company, developed in strategic partnership with the Shanghai Gold Exchange, aims to replicate the institutional efficiency of London while rooting it within the Asian financial ecosystem. This is supported by massive investments in local vaulting, logistics, and direct connectivity to mainland China.

The implications are clear: if an international institution wants access to the world’s largest physical gold market—China—they will increasingly find that the path of least resistance leads to Hong Kong, not London.

Official Responses and Strategic Positioning

The response from financial authorities across Asia has been calculated and diverse. While Hong Kong focuses on its direct link to the massive Chinese market, Singapore is carving out a different niche.

The Monetary Authority of Singapore (MAS) has formed a consortium involving giants like JPMorgan, UBS, DBS, and ICBC Standard Bank. Their strategy is rooted in "neutrality." Where Hong Kong offers proximity to the Chinese economic engine, Singapore offers a "Switzerland of the East" proposition—a safe, highly regulated, and politically neutral environment for international capital that may be wary of the political complexities inherent in Chinese markets.

Neither city is currently engaged in a "race to the bottom" to displace the other. Instead, they are engaged in a collective effort to displace an assumption: the assumption that the global gold market must, by necessity, remain tethered to the Atlantic.

Implications for the Future of Finance

The transition of the gold market is not merely a story about bullion; it is a window into the future of the global monetary system.

1. The Death of the "Unified" Financial Framework

The post-Cold War consensus relied on the belief that financial globalization would continue under a single, unified framework. That era is effectively over. We are entering a period of "multi-polar finance," where regions will increasingly operate their own clearing, settlement, and reserve management systems.

2. The Premium on Sovereignty

We are witnessing a shift where "location matters." As reserve managers prioritize assets that cannot be frozen, the geographic location of the physical gold—and the jurisdiction governing the electronic ledger of its ownership—is becoming as important as the metal’s purity.

3. The Gradual Decay of Legacy Centers

It is important to note that London will not collapse overnight. Financial centers possess deep institutional memory, entrenched relationships, and immense liquidity. However, history suggests that financial power follows the flow of trade. Just as London’s dominance was built on its role as the center of 19th-century commerce, the current accumulation of gold in Asia will inevitably force the infrastructure to follow.

4. The End of the "Gold Doesn’t Move" Myth

The old adage that gold never moves is becoming a relic of the past. While the bars may remain in vaults, the control of the gold, the settlement of the gold, and the valuation of the gold are all undergoing a migration.

Conclusion

The rise of Asia as the primary center for gold clearing and trading is not a revolution that will be announced with a bang. It is a slow-moving, structural change disguised as administrative upgrades and new clearing partnerships.

As we look toward the end of the decade, the global map of finance is being redrawn. The vault doors themselves may be static, but the gravity of the gold market has undeniably shifted. The world is witnessing the "long journey home" for the world’s most precious metal—back to the east, where the demand is, and increasingly, where the power to manage it resides. The institutions that fail to recognize this shift may soon find themselves presiding over an empty infrastructure, while the real business of gold happens thousands of miles away.