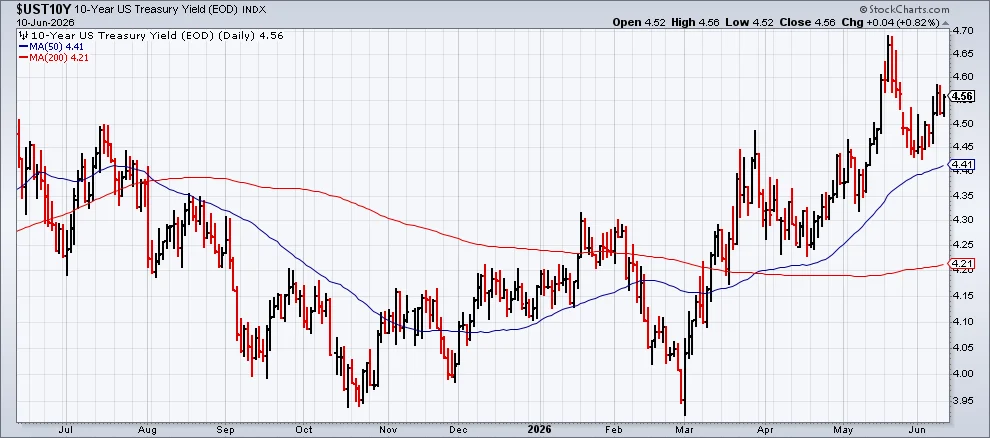

The global financial landscape is currently navigating a period of heightened recalibration, as the convergence of geopolitical instability in the Middle East and persistent domestic inflationary pressures forces a fundamental reassessment of long-term debt pricing. Central to this shift is the U.S. 10-year Treasury yield, which has seen a marked departure from its theoretical "fair-value" equilibrium. As of the latest market close on June 10, the 10-year yield reached 4.56%, hovering near a 12-month high and signaling a significant shift in investor sentiment that threatens to complicate the Federal Reserve’s path toward normalization.

Main Facts: The Growing Divergence

The widening gap between the market-traded 10-year Treasury yield and its estimated fair value—a metric often referred to as the "market premium"—is the defining story of the current bond market. Data through May, synthesized via The Capital Spectator’s ensemble model, reveals that the 10-year yield is currently trading 48 basis points above its fair-value estimate.

This is not merely a statistical anomaly; it is a manifestation of investor anxiety. The fair-value model, which aggregates multiple economic indicators to determine what the yield should be under stable conditions, has been consistently outpaced by the actual market yield. This 48-basis-point spread represents the highest premium observed since July 2025, effectively ending the period of "normalization" that characterized the earlier months of the year. Investors are no longer pricing Treasuries based solely on interest rate policy and economic output; they are now demanding a significant risk premium to account for the unpredictable nature of the current global macro environment.

Chronology: From Pandemic Recovery to Geopolitical Reversal

To understand the current state of the bond market, one must examine the timeline of the last few years, which can be broken down into three distinct phases:

1. The Post-Pandemic Normalization (2022–2023)

Following the massive inflationary surge caused by the COVID-19 pandemic and the subsequent supply chain disruptions, the Federal Reserve embarked on an aggressive campaign of interest rate hikes. During this period, the market premium on the 10-year Treasury reached extreme highs as investors grappled with the uncertainty of "transitory" vs. "structural" inflation. By late 2023 and early 2024, as inflation began to show signs of cooling, the market entered a phase of normalization. The premium began to trend lower, suggesting that the market had finally priced in a "new normal" for interest rates.

2. The Geopolitical Inflection Point (Early 2024)

The trajectory shifted dramatically with the intensification of the conflict in the Middle East. As regional tensions escalated, the global energy markets experienced renewed volatility. The prospect of supply chain bottlenecks, combined with a potential surge in oil and commodity prices, triggered a "risk-off" sentiment in the bond market. The trend of a declining premium—which had been the dominant theme for several months—abruptly stalled.

3. The Current Volatility (May–June 2024)

The most recent data from May serves as a stark confirmation of this trend reversal. The 10-year yield, which had been attempting to stabilize, surged upward to breach the 4.5% threshold. This movement signifies that the market is actively hedging against the possibility of "higher-for-longer" inflation caused by external, non-monetary factors. The transition from a declining premium to a rapidly expanding one illustrates that the market is currently in a state of reactive recalibration.

Supporting Data: Deconstructing the Ensemble Model

The Capital Spectator’s ensemble model provides a robust framework for understanding this disconnect by averaging three distinct fair-value estimates. By comparing the 10-year Treasury yield against this average, analysts can isolate the "market premium"—the portion of the yield that cannot be explained by fundamental economic variables alone.

Analyzing the Spread

The spread, defined as the current 10-year yield minus the fair-value estimate, serves as a barometer for market fear. When the spread is narrow, market participants are confident in the economic outlook. When it widens—as it has done over the past few weeks—it indicates that the market is pricing in an "inflation risk premium."

The data indicates that while inflation is technically cooling, the expectations for future inflation are rising. Because the 10-year bond is a long-duration asset, it is highly sensitive to these long-term inflationary expectations. When geopolitical events threaten to disrupt the global supply chain, investors demand higher yields to compensate for the purchasing power risk, even if the current Federal Reserve policy remains relatively static.

Official Responses and Institutional Perspectives

While the Federal Reserve has remained largely focused on core PCE (Personal Consumption Expenditures) data and labor market resilience, the bond market is sending a different signal.

The Federal Reserve’s Dilemma

Central bank officials have frequently cited "data dependency" as their guiding principle. However, the market’s current behavior suggests that investors are looking beyond the Fed’s traditional metrics. If the 10-year yield continues to remain elevated due to a risk premium, it acts as a form of "de facto" tightening. Even if the Fed holds the federal funds rate steady, the rise in the 10-year yield increases the cost of borrowing for mortgages, corporate loans, and consumer credit.

Institutional analysts note that the Fed is in a difficult position. If they signal a pivot toward rate cuts, they risk further stoking inflation if the Middle East conflict leads to energy price shocks. Conversely, if they maintain a hawkish stance, they risk stifling growth just as the economy attempts to navigate the headwinds of global instability.

Investor Sentiment

Institutional investors are increasingly moving toward defensive positioning. The rise in the 10-year yield is being viewed not just as a reflection of interest rates, but as a flight to quality that is simultaneously being offset by the fear of fiscal irresponsibility and external shocks. Many bond traders are now waiting for clear signals from both the geopolitical front and the upcoming inflation reports before re-entering the market, leading to a period of heightened sensitivity to any news headlines originating from conflict zones.

Implications: What Lies Ahead?

The widening of the market premium has profound implications for the broader economy and the financial future of the average citizen.

1. Increased Borrowing Costs

The 10-year Treasury yield serves as the benchmark for a wide array of lending products, most notably the 30-year fixed-rate mortgage. As the market premium expands, the cost of credit rises, regardless of central bank policy. This threatens to cool the housing market further and increase interest expenses for corporations that are currently looking to refinance debt accumulated during the era of low interest rates.

2. The "Risk Premium" Ceiling

One of the most critical questions for investors is: how much higher can this premium go? Historically, periods of extreme geopolitical instability have seen the market premium reach even higher levels than the current 48 basis points. If the Middle East conflict results in a sustained spike in oil prices, we could see the premium widen further, pushing the 10-year yield toward the 5% mark. Such a move would likely trigger a broader sell-off in equities, as the "risk-free" rate becomes more attractive compared to the earnings yield of the stock market.

3. Structural Reassessment of Portfolios

Investors are being forced to rethink the "60/40" portfolio model. Traditionally, bonds served as a hedge against equity market volatility. However, when both bonds and stocks are pressured by the same inflationary and geopolitical fears, that correlation breaks down. Investors are now looking toward alternative assets, including commodities and inflation-protected securities (TIPS), to mitigate the risks associated with this widening yield gap.

Conclusion: A Market in Search of Equilibrium

The recent surge in the 10-year Treasury yield to 4.56%, accompanied by a 48-basis-point premium, is a clear warning sign from the bond market. The era of pandemic-era normalization has been replaced by a new era defined by geopolitical risk and persistent inflation uncertainty.

As we look toward the remainder of the year, the primary driver for the Treasury market will be the evolution of the Middle East conflict and its secondary effects on global energy prices. Until there is a cooling of these geopolitical tensions, it is unlikely that the market premium will return to historical norms. For policy makers and investors alike, the message is clear: the path to economic stability is no longer just about interest rates; it is about managing the risks of a world that has become significantly more volatile. The coming months will be a test of resilience for the global financial system, as it attempts to reconcile the realities of a shifting macro-landscape with the need for stable, long-term growth.