In the world of personal finance, most people are chasing the wrong numbers. We obsess over the daily fluctuations of our checking account balances, stress over the monthly volatility of our credit card bills, and feel a momentary rush when a paycheck hits. However, these figures are merely "noise"—snapshots of a fleeting moment that rarely tell the full story of your financial health.

If you want to know if you are truly building wealth or merely running on a financial treadmill, there is only one number that matters: your net worth.

Net worth is the ultimate barometer of financial security. It is the simple, honest math of your life: total assets minus total liabilities. While your monthly spending and income are critical components, they are the gears, not the destination. Net worth is the speedometer that tells you exactly where you are heading.

The Core Concept: Assets vs. Liabilities

At its most fundamental level, your net worth is an objective accounting of your financial standing.

- Assets: Everything you own that holds value—cash in savings, retirement accounts, brokerage portfolios, real estate, and personal property like vehicles.

- Liabilities: Everything you owe—mortgage balances, student loans, credit card debt, and personal loans.

The beauty of the net worth calculation is that it strips away the psychological clutter of daily transactions. When you pay off $500 of credit card debt, your checking account balance drops, which can feel like a setback. However, when viewed through the lens of net worth, that transaction is a clear victory: your liabilities have decreased, and your equity has increased.

By focusing on the "big picture" number rather than individual transactions, you gain a clearer view of your long-term trajectory.

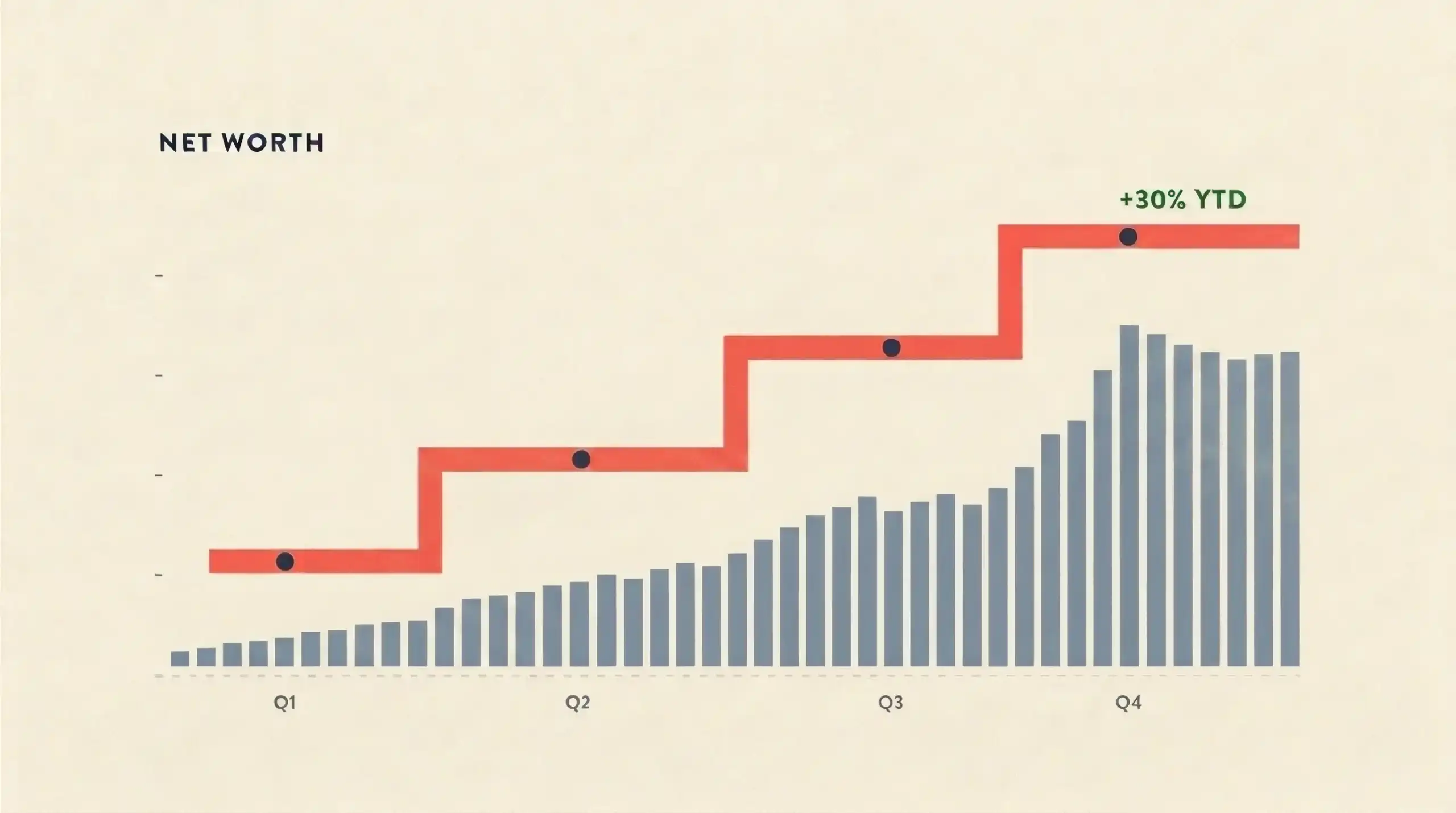

Chronology: Why Quarterly Tracking is the "Goldilocks" Rhythm

One of the most common pitfalls in personal finance is the frequency of monitoring. Many people check their accounts daily, which leads to anxiety over market volatility or minor spending blips. Others check once a year, leaving them vulnerable to drifting off course for months at a time without realizing it.

The optimal rhythm for tracking net worth is quarterly. Here is why this specific cadence works:

1. The Monthly Trap

Monthly tracking is often too noisy. Market volatility can cause your investment portfolio to dip significantly in a 30-day window, even if your savings rate remains excellent. If you only look at your net worth monthly, you may be tempted to react impulsively to short-term market corrections, potentially sabotaging your long-term strategy.

2. The Annual Blind Spot

Annual tracking is insufficient in an age of rapid economic change. If you wait 12 months to audit your finances, you could be losing thousands of dollars to "financial leakage"—such as high-interest debt or unused subscriptions—without realizing it until the end of the year.

3. The Quarterly Sweet Spot

By checking your net worth every three months (January, April, July, and October), you smooth out the volatility of the stock market while maintaining enough agility to make course corrections. It is a "Goldilocks" approach: frequent enough to keep you accountable, but infrequent enough to ignore the daily white noise of the financial markets.

Supporting Data: How Automation Simplifies the Process

The primary reason most people fail to track their net worth is the perceived difficulty of manual calculation. In the past, this required complex spreadsheets and hours of manual data entry. Today, technology has rendered that hurdle obsolete.

Modern personal finance dashboards—such as Empower or Monarch Money—serve as the modern-day "command centers" for your wealth. These tools securely connect to your financial institutions, including banks, credit card issuers, and investment firms.

Setting Up Your Financial Dashboard

The initial setup takes approximately 20 minutes:

- Link Your Accounts: Aggregate every asset and liability into one portal.

- Input Fixed Assets: Manually add the current market value of assets that don’t have a digital feed, such as your home (use conservative estimates based on local comps) or high-value collectibles.

- Automate Tracking: Once linked, the software performs the "Assets minus Liabilities" math for you in real-time.

From this point forward, the habit requires only two minutes, four times a year. Simply open the app, record the number, and compare it to the previous quarter. If the trend line is moving upward, your financial life is working, even if individual months feel messy.

Implications of a Wealth-First Mindset

When you shift your focus from "how much money do I have in checking?" to "what is my total net worth?", the psychology of your spending begins to change.

The Power of "Direction Over Precision"

You do not need to know your net worth down to the exact penny. A rounded figure is perfectly acceptable. The goal is to identify the direction. If your net worth is consistently growing, you are winning. If it is stagnant or declining, you have identified a problem that requires immediate investigation.

Identifying "Financial Leaks"

If you notice that your net worth has remained flat for four consecutive quarters despite steady income, it is a signal that your money is "leaking." This could be due to lifestyle creep, high interest rates on debt, or poor asset allocation. A quarterly audit forces you to confront these leaks early, preventing them from snowballing into long-term financial distress.

Official Perspectives: Financial Experts on Wealth Metrics

Financial advisors and behavioral economists widely agree that net worth is the superior metric for gauging long-term success. While income levels (often called "the vanity metric") are important, they are often decoupled from actual wealth. A high-earner can have a low net worth if their liabilities and spending are equally high.

According to industry analysts, "Wealth is what you don’t see." It is the money that hasn’t been spent yet. By focusing on net worth, you are training your brain to prioritize the accumulation of assets over the consumption of goods. This mindset shift is the defining difference between those who live paycheck-to-paycheck and those who build generational security.

Conclusion: Making the Shift Today

If you are currently only looking at your account balances, you are viewing your financial life through a straw. It is time to step back and look at the whole picture.

The strategy is simple:

- Commit to the Habit: Set a recurring calendar reminder for the first week of every quarter.

- Leverage Technology: Use a trusted dashboard to do the heavy lifting.

- Prioritize the Trend: Don’t panic over a bad quarter; look at the year-over-year growth.

Building wealth is not about being perfect every month; it is about staying the course over the long term. By monitoring your net worth, you gain the clarity needed to make smarter decisions, eliminate wasteful spending, and ultimately achieve the financial freedom you deserve.

The next quarter begins soon. Take 20 minutes this weekend to set up your dashboard. It may be the most important financial decision you make all year.

Editorial & Advertiser Disclosure

The editorial content on this website is not provided, commissioned, reviewed, approved, or otherwise endorsed by any advertiser. Opinions expressed are ours alone, not those of any advertiser. The offers that appear are from companies from which we may receive compensation. However, this compensation does not impact where and how these companies are mentioned on the site. We do not include all companies or all available offers in the marketplace.