Executive Summary: Navigating a New Normal

Fixed income markets have spent the last several months in a state of high-velocity adaptation. Following the escalation of the conflict involving Iran, global financial markets have been forced to reconcile heightened geopolitical volatility with a U.S. economy that continues to defy conventional wisdom regarding its growth trajectory. The result has been a significant repricing of Treasury yields, driven not merely by inflationary fears, but by a fundamental recalibration of what constitutes "normal" in the post-pandemic era.

Despite the sharp upward shift in the yield curve, the underlying data remains remarkably resilient. Long-term inflation expectations have remained anchored, and the economic pulse of the United States continues to beat with surprising vigor. This suggests that the "bad news"—including the prospect of higher-for-longer interest rates and geopolitical instability—has largely been digested by the markets. For investors, this creates a landscape that is cautious but far from bearish, where the most aggressive yield spikes may already be in the rearview mirror.

Chronology: The Repricing of the Treasury Curve

Since the initial onset of the Iran conflict, the U.S. Treasury market has undergone a classic "bear flattening." In this scenario, front-end yields have ascended more aggressively than their long-term counterparts. Data through late last week reveals that the 2-year Treasury yield has climbed approximately 60 basis points (bps), while the 10-year yield has surged by 77 bps.

This rapid adjustment represents a multi-layered response by market participants. First, the conflict triggered immediate concerns regarding energy price volatility, which naturally stoked inflation expectations. Second, investors demanded a higher "term premium"—essentially a risk-adjustment payment for holding long-term debt in an increasingly uncertain global climate. Finally, the market began a fundamental reassessment of the Federal Open Market Committee’s (FOMC) policy path. Unlike the reactionary panic seen in previous cycles, this move has been orderly. Liquidity in core fixed income sectors has remained robust, suggesting that the market is processing these geopolitical tremors with mechanical efficiency rather than emotional distress.

Supporting Data: Dissecting the Yield Increase

To understand the current environment, it is necessary to deconstruct the nominal Treasury yield. When analyzing the 10-year Treasury movement since the start of the regional conflict, roughly 35 basis points of the increase can be attributed to heightened real growth expectations. In contrast, only about 14 basis points are directly tied to inflation expectations.

This distinction is profound. It indicates that the market is not pricing in a "stagflationary" doom loop. Instead, investors are betting on a "soft landing plus" scenario—a reality where the economy remains resilient, potentially bolstered by sustained investment in artificial intelligence and productivity-enhancing technologies.

Furthermore, economic data has consistently surprised to the upside, as measured by the Bloomberg Economic Surprise Index. This momentum has provided the Federal Reserve with a unique form of "policy cover." Because inflation expectations remain anchored—unlike the 2022 period where the Fed was visibly behind the curve—policymakers are not currently forced into a corner. They possess the optionality to remain on hold, watching for further data, rather than being compelled to react to short-term price spikes.

Recent Treasury auctions further corroborate this stability. Auctions for 2-year, 5-year, and 7-year notes, totaling $183 billion, were met with sufficient demand from both domestic and foreign participants. While not euphoric, these auctions demonstrated that investors are comfortable with current yield levels, suggesting that the "worst-case" scenario for bond pricing has likely been discounted.

Official Responses and Policy Shifts

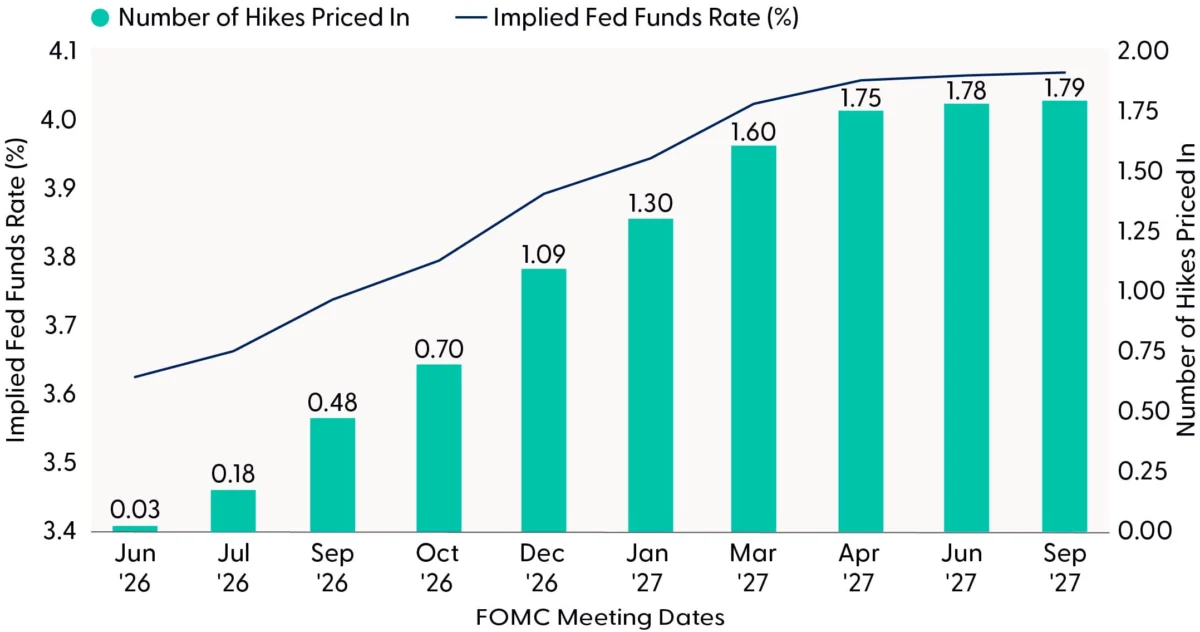

The most striking development in the current cycle is the sea change in Fed policy expectations. Earlier in 2026, the consensus was anchored on a series of rate cuts. Today, the market has performed a near-total reversal, pricing in a 100% probability of at least one rate hike this year, with a 67% chance of two hikes by mid-2027.

The implied neutral fed funds rate has been nudged upward to approximately 4%, aligning market expectations with the more hawkish contingent of the FOMC. Even Federal Reserve Governor Chris Waller, traditionally considered a relative dove, has signaled that if the data holds its current course, further tightening may be required.

However, it is vital to distinguish between a Fed that is "compelled" to hike and a Fed that is "flexible." The current narrative suggests that while the FOMC retains the tools to hike, they are not currently forced to do so unless inflation expectations break their current moorings. The market has essentially matured, moving away from the assumption that the post-pandemic cycle would mirror the low-rate environments of the past decade. There is a growing recognition that structural shifts—such as demographic changes and increased productivity—may necessitate a higher long-term equilibrium rate.

Strategic Implications and Asset Allocation

For the LPL Strategic and Tactical Asset Allocation Committee (STAAC), the current environment demands a balanced, disciplined approach. The committee maintains a neutral stance on duration relative to benchmarks, acknowledging that while the risk-reward profile is more favorable than it was months ago, it is not yet a "table-pounding" buying opportunity.

Tactical Recommendations:

- Duration Management: The committee remains neutral but stands ready to add duration if the 10-year Treasury yield climbs toward the 4.75%–5.00% range. At those levels, the yield would likely offer a compelling entry point relative to the stability of long-term inflation expectations.

- Equity Overweight: A tactical overweight in equities is maintained, balanced by a defensive factor tilt. This allows investors to participate in the "growth-plus" narrative while hedging against the potential for unexpected geopolitical volatility.

- Fixed Income Underweight: Within the bond portfolio, the committee recommends a cautious approach. Specifically, there is an underweight position in investment-grade corporates and mortgage-backed securities (MBS). Because credit spreads remain tight by historical standards, the compensation for the risk involved in these sectors is currently insufficient.

- Diversification: The emphasis remains on alternative assets and diversifying strategies to mitigate the impact of rate-sensitive sectors that may still face pressure if the conflict in the Middle East escalates further.

Conclusion: A Balanced Outlook

The Treasury market has undergone a rigorous stress test, successfully absorbing a shift in policy expectations, a rise in term premia, and the psychological weight of geopolitical conflict. The "bad news" of higher rates and stubborn inflation appears to be largely priced into current valuations.

While long-maturity yields are expected to remain elevated in the near term, the frantic pace of the recent yield surge is likely nearing a plateau. Absent a catastrophic reacceleration in energy prices or a sudden collapse in economic growth, the risk-reward profile for core fixed income is finally finding its equilibrium. For the investor, the current environment is no longer about predicting the "next" shock, but rather about managing a portfolio within a structurally higher—but stable—rate environment. The Fed, armed with renewed credibility and anchored expectations, remains in the driver’s seat, moving with caution rather than haste.