Value Added Tax (VAT) serves as the fiscal backbone for most European economies, providing a stable and reliable stream of government revenue. Yet, tucked away within the complex machinery of national tax codes lies a critical policy lever: the VAT registration threshold. By exempting small businesses from the obligation to collect and remit VAT, governments aim to reduce administrative burdens on micro-enterprises. However, a closer look at the European landscape reveals that these thresholds are far from neutral. They act as invisible economic boundaries that dictate business growth, influence competition, and frequently incentivize firms to artificially cap their own success.

The Landscape of VAT Exemptions: Nominal vs. Real Economic Weight

When examining the 32 major European economies, the variation in VAT registration thresholds is staggering. At the nominal level, Switzerland leads the pack, setting its exemption bar at CHF 100,000 (approximately €106,724). This high threshold allows a significant portion of Swiss sole proprietorships and small businesses to operate outside the VAT collection system entirely. The United Kingdom and France follow closely, with thresholds of £90,000 (€105,043) and €87,000, respectively.

At the opposite end of the spectrum, some nations have eschewed the exemption model altogether. Spain and Turkey stand as unique examples, maintaining no VAT threshold at all. In these jurisdictions, every business entity—from the largest conglomerate to the smallest independent freelancer—is enrolled in the VAT system. This "universal inclusion" model ensures a wider tax base and eliminates the administrative complexity of monitoring turnover to determine tax eligibility, though it places a higher compliance burden on the smallest market participants.

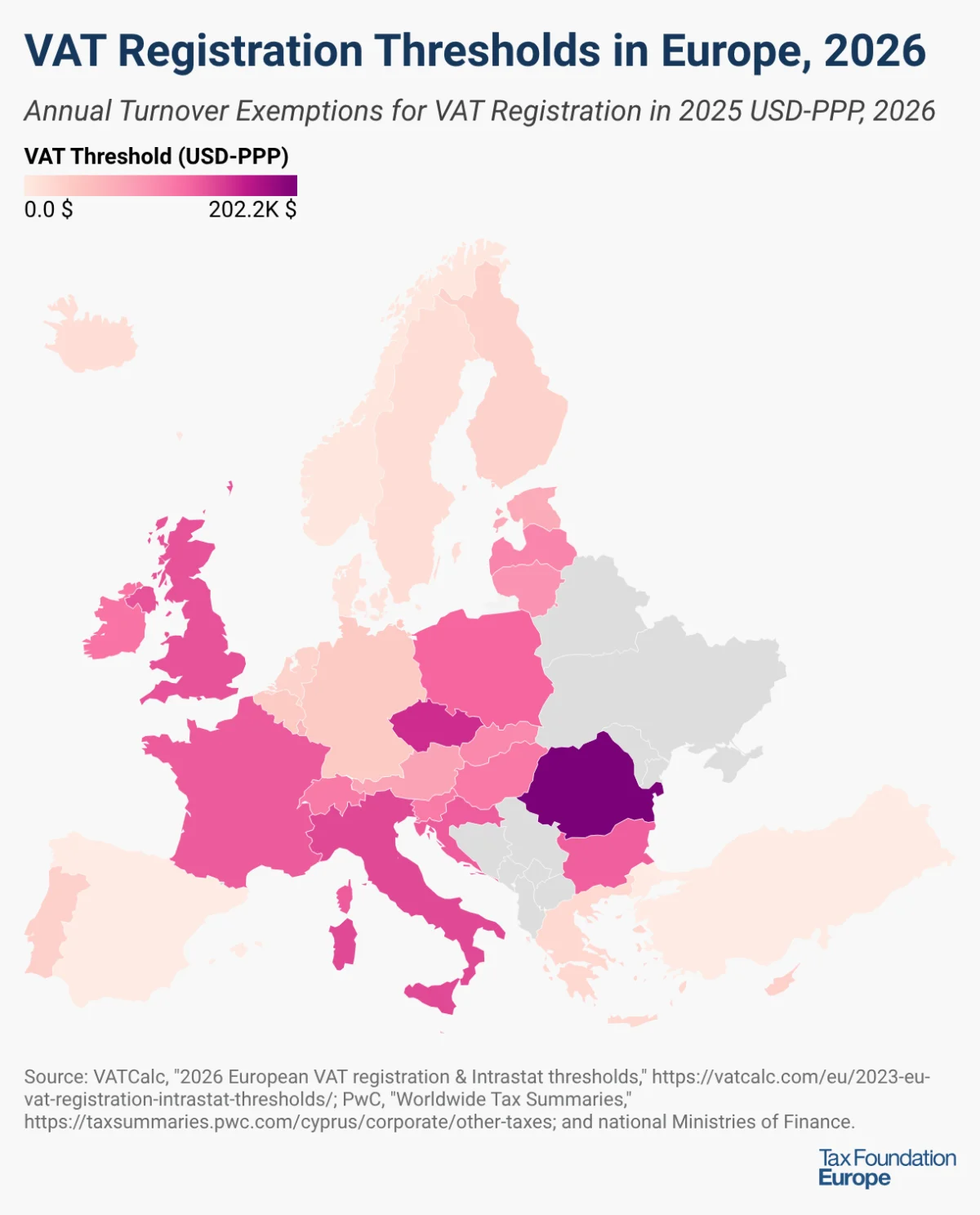

However, comparing nominal figures provides only a partial picture. The true economic impact of a threshold is felt relative to local price levels—a concept best captured by Purchasing Power Parity (PPP). When adjusted for PPP, the leaderboard shifts dramatically. Romania emerges as the frontrunner, with an effective threshold of RON 395,000 ($202,206). The Czech Republic and Italy also maintain exceptionally high thresholds in real terms, at $155,039 and $140,246, respectively. These figures suggest that in some European nations, the "small business" exemption is far more generous than a simple currency conversion would imply.

A Chronology of Recent Policy Shifts

The last 24 months have seen a trend toward liberalization, with several European governments opting to raise their VAT thresholds. This movement is largely framed as a relief measure for small businesses struggling with inflation and rising operational costs.

- September 2025: Romania took a significant step by increasing its VAT registration threshold from RON 300,000 to RON 395,000. This move effectively signaled a policy shift toward insulating a larger cohort of small and medium-sized enterprises (SMEs) from the administrative overhead of VAT compliance.

- 2026 (Beginning of Year): Hungary and Poland both enacted substantial adjustments. Hungary raised its limit from HUF 18 million to 20 million (approx. €50,280), with a further scheduled increase to 22 million (€55,310) by 2027. Poland followed suit, shifting its threshold from PLN 200,000 to 240,000 (€56,610).

- April 2026: The Belgian parliament moved to support its small business sector by approving an increase in the VAT exemption threshold from €25,000 to €30,000. While the measure has been approved, the regulatory community is currently awaiting the final official entry into force.

These changes represent a concerted effort across the continent to calibrate tax policy with the realities of modern business costs. Yet, while these increases offer immediate relief, they also exacerbate the underlying structural distortions inherent in VAT threshold systems.

The "Notch" Effect: The Economic Cost of Growth

The most significant critique of VAT thresholds is the creation of a "tax cliff" or "notch." In tax theory, a notch occurs when the tax liability changes drastically at a specific threshold, rather than being phased in gradually. If a firm’s annual turnover remains even one euro below the threshold, it remains exempt. If it crosses that threshold by a single euro, it suddenly becomes liable for VAT on its entire value added, not just the amount exceeding the limit.

This creates a perverse economic incentive. Empirical research, including studies published by the IMF, suggests that firms frequently engage in "bunching"—a phenomenon where businesses deliberately report turnover just below the threshold to avoid the compliance and tax burden.

The Czech Republic serves as a textbook case study. Because it maintains one of Europe’s highest thresholds in PPP terms, researchers have observed a distinct spike in the distribution of corporate turnover just below the cutoff. As the government increases the threshold, the "bunching" point shifts in tandem. This confirms that businesses are not merely organic in their growth; they are actively suppressing their output to avoid crossing the tax cliff. This behavior represents a net loss to the economy, as productive firms that could scale up and create jobs choose instead to stagnate to maintain their tax-advantaged status.

Implications for Productivity and Competition

Beyond the immediate compliance costs, VAT thresholds introduce a distortion that favors smaller firms over larger ones, often at the expense of overall market efficiency.

The Suppression of Economies of Scale

When firms are incentivized to stay small, they lose the ability to realize economies of scale. In a competitive market, larger firms are usually more productive because they can optimize supply chains, invest in technology, and lower unit costs. By effectively penalizing growth, high VAT thresholds prevent these efficiencies from manifesting. This protects "tax-advantaged" micro-enterprises, which may be less productive, while placing more efficient competitors at a disadvantage.

Administrative Distortion

The burden of tax compliance is real. Small businesses often lack the accounting infrastructure of larger firms, making the filing of VAT returns a costly and time-consuming endeavor. While the policy intention—reducing this burden—is well-founded, the "cliff" creates a "hump" in the cost-benefit analysis of expanding a business. The transition from an exempt micro-entity to a VAT-registered SME is not just a change in status; it is a fundamental shift in business operations that carries significant risk.

Revenue Leakage

Finally, there is the matter of fiscal sustainability. Every euro of turnover that is suppressed to stay below a threshold is a euro that does not contribute to the VAT tax base. In an era where European governments are facing increasing pressure to fund social services and infrastructure, the revenue sacrificed to maintain these thresholds must be carefully weighed against the benefits provided to the SME sector.

Policy Recommendations and Future Outlook

The prevailing consensus among economists is that while VAT thresholds serve a legitimate purpose in reducing administrative friction for the smallest entities, they are currently functioning as a drag on economic growth.

To mitigate these distortions, policymakers are increasingly encouraged to move away from "cliff" thresholds toward a "tapered" approach. A tapered system would allow for a gradual introduction of VAT obligations, smoothing the transition for growing firms and eliminating the incentive to suppress activity. By replacing the "all-or-nothing" approach with a phased transition, governments could capture more revenue and encourage businesses to grow according to market demand rather than tax policy.

Furthermore, the digitization of tax reporting—often referred to as "e-invoicing"—is rapidly reducing the administrative cost of compliance. As technology makes it easier and cheaper for small businesses to track and report VAT, the original justification for high thresholds (i.e., that compliance is too burdensome) is becoming increasingly obsolete.

In conclusion, while the recent increases in VAT thresholds across Europe provide temporary relief to small businesses, they also entrench a system of economic distortion. As European nations look to increase productivity and ensure the long-term viability of their tax systems, they must address the "notch" effect. The future of European tax policy likely lies in digitizing compliance and smoothing the transition into the tax system, ensuring that tax obligations are a byproduct of success rather than a barrier to it. By refining these thresholds, policymakers can foster a more dynamic and competitive business environment that rewards growth rather than stagnation.