For the average portfolio manager, gold has long been relegated to a niche category—a “commodity” to be held as a tactical inflation hedge or a disaster insurance policy. However, this narrow classification ignores the metal’s historical function as the bedrock of monetary confidence. Each year, the publication In Gold We Trust, authored by Ronald-Peter Stöferle and Mark Valek, challenges this reductionist view. Rather than treating gold as merely another asset class, the report utilizes it as a vantage point—a high-resolution lens through which to examine the tectonic shifts in interest rates, debt cycles, fiscal policies, and the evolving architecture of the global financial system.

Their latest edition, Back to the Monetary Future, serves as a comprehensive diagnostic of the current era. It suggests that we are witnessing the unwinding of assumptions that have governed global capital flows for the past thirty years. Whether one holds physical gold or not, the report’s conclusions offer a roadmap for understanding the structural pressures currently reshaping the world economy.

The Structural Realignment: Main Facts

The core thesis of this year’s report is that the world is transitioning into a phase of heightened volatility, where the "rules-based" international order is increasingly strained by fiscal profligacy and geopolitical fragmentation. Gold, in this context, acts as an organizing principle.

As central banks struggle to manage record-high debt-to-GDP ratios and navigate the complexities of the post-pandemic inflationary environment, the "flight to quality" has moved beyond retail investors. We are seeing a systemic shift: nations are prioritizing "hard" assets over the digital or paper-based credit instruments that dominated the late 20th-century financial order. The report argues that we are not necessarily looking at an overnight collapse of the current system, but rather a profound, subtle re-evaluation of what constitutes a "safe" asset in an era of waning trust.

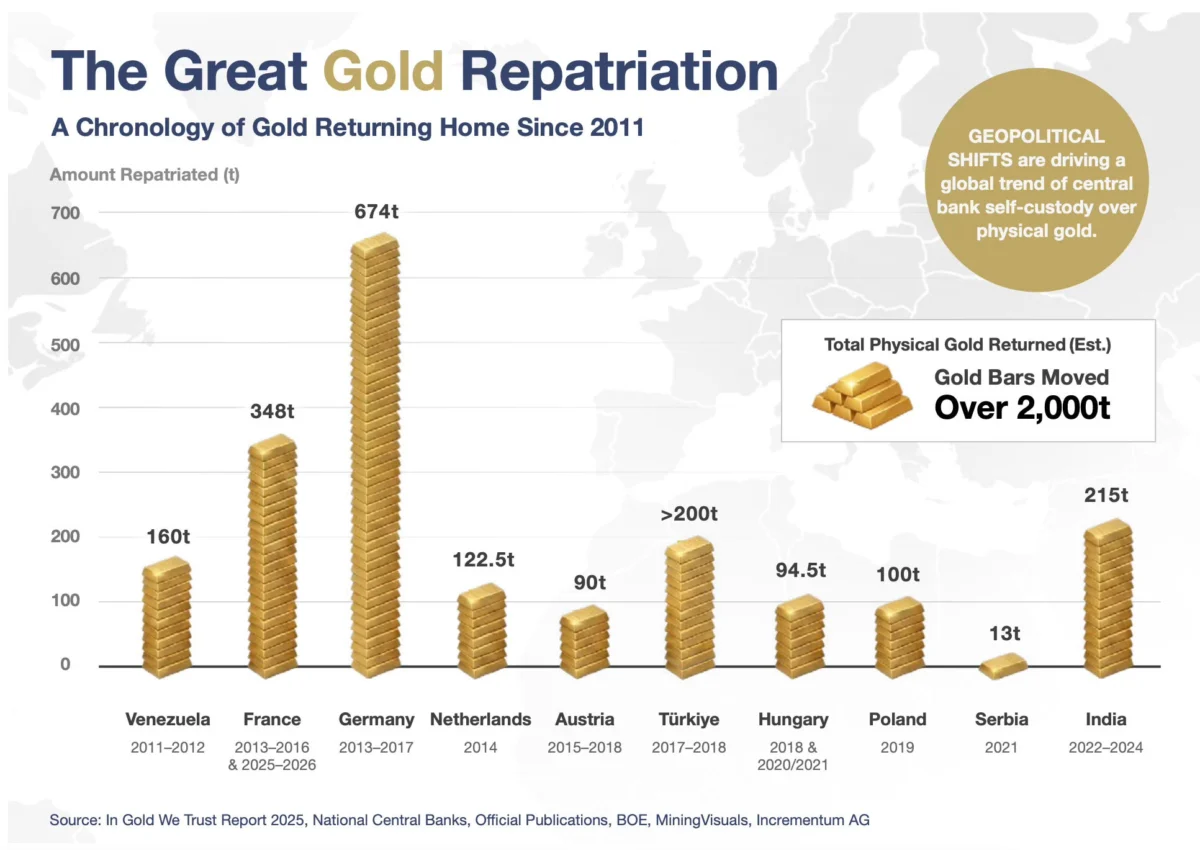

A Chronology of Neglect and Rebirth

To understand the current obsession with gold, one must look at the historical timeline of the mining industry and its relationship with equity markets.

The Twentieth Century: From Dominance to Marginalization

At the dawn of the 1900s, mining equities accounted for nearly 10% of global market capitalization. It was an era where raw material extraction was seen as the primary engine of civilization. Following the post-war commodity boom, the sector maintained a robust presence. However, the last few decades have seen a catastrophic decline in the sector’s standing. Today, mining companies represent approximately 1% of global equity value.

The Modern Disconnect

We are currently in a bizarre period of historical asymmetry. While the world is in a frenzy over the AI-driven "electrification of everything"—which requires massive amounts of copper, silver, lithium, and rare earth elements—the producers of these materials are being ignored by the broader market. This creates a "neglect premium." Investors are bidding up the valuations of the software and data center companies that consume these raw materials, while ignoring the companies that provide the physical components required for that growth. History suggests that such extreme divergences rarely last; eventually, the leverage between commodity prices and equity performance tends to reassert itself.

Supporting Data: Five Key Indicators

The In Gold We Trust report highlights five critical data points that underscore the current monetary shift.

1. The Marginalization of Mining

The "Century of Neglect" chart is perhaps the most striking visual in the report. It demonstrates that the mining sector has been hollowed out from a pillar of the global market to a footnote. This isn’t just a cyclical downturn; it is a fundamental shift in capital allocation. Should commodity prices continue to rise—driven by the sheer demand for infrastructure—the current lack of investment in mining capacity may lead to a supply-side crisis that triggers a massive re-rating of mining stocks.

2. Silver and the AI Infrastructure

While gold is the primary focus, silver has emerged as the "hidden" beneficiary of the AI boom. Data centers are thermal-intensive environments; silver’s unique conductive and thermal management properties make it virtually irreplaceable in high-end semiconductor packaging and circuitry. Current projections indicate that silver demand from the technology sector will rise sharply over the next decade. Investors who are searching for "AI plays" might be looking at the wrong end of the supply chain.

3. The Central Bank Reserve Revolution

Perhaps the most consequential trend identified is the divergence in central bank behavior. Data shows a steady rise in gold holdings among global central banks, occurring simultaneously with a reduction in exposure to U.S. Treasury debt. For decades, the global system relied on the recycling of trade surpluses into U.S. debt. That cycle is now showing signs of fatigue. Gold is favored by central banks because it carries no counterparty risk and no duration risk—a necessity in a world defined by sanctions and geopolitical rivalry.

4. The Discipline of Geological Scarcity

In an era of unprecedented money printing and fiscal expansion, gold remains the only asset that cannot be "printed" by a committee. The annual growth rate of above-ground gold stocks has remained consistently between 1.7% and 1.8% for over a century. This supply-side discipline acts as a constant anchor in a world of financial excess, where sovereign debt can expand by trillions of dollars in a matter of months.

5. The Repatriation of Sovereignty

Since 2011, a significant number of nations—including Germany, Poland, Turkey, and India—have brought substantial portions of their gold reserves home. This is a symbolic and practical shift. It signifies a move away from the "trusted" custody arrangements of the past toward a model of decentralized control. It is an expression of a world becoming increasingly cautious about external dependencies.

Official Responses and Perspectives

While mainstream financial institutions often downplay the significance of gold as an asset class, the actions of the world’s most powerful central banks tell a different story. The People’s Bank of China, the Reserve Bank of India, and various European central banks have consistently added to their gold reserves over the last three years.

Official statements from these institutions often focus on "diversification," but the underlying message is clear: they are preparing for a more fragmented world. Skeptics argue that gold is a "barbarous relic" that yields no interest. However, the proponents of the In Gold We Trust methodology counter that in a world where real yields are suppressed by inflation or fiscal policy, the "zero yield" of gold becomes competitive. When the alternative is a currency losing purchasing power or a bond market facing inflationary risks, the utility of a non-sovereign, physical asset becomes clear.

Implications for the Global Future

The findings of the In Gold We Trust report suggest that we are entering a period of "monetary realism."

- Inflationary Volatility: With debt levels reaching unsustainable peaks, governments will likely continue to favor inflationary policy over austerity. Gold serves as the primary hedge against this erosion of currency.

- The End of the "Easy" Global Order: The repatriation of gold and the diversification of reserves by central banks suggest that the dollar-centric global order is being augmented by a multi-polar system where hard assets carry more weight than paper promises.

- The Infrastructure Gap: The disconnect between the demand for AI hardware and the investment in the mining industry suggests that we are headed toward a long-term commodities supercycle. Investors who remain fixated on digital assets while ignoring the physical foundation of the economy may find themselves on the wrong side of a major historical transition.

In conclusion, the In Gold We Trust report is not merely a document for gold bugs; it is an essential read for anyone attempting to map the future of the global financial system. It forces us to confront the fact that our modern, digital, and hyper-leveraged world still rests upon the physical realities of mining, energy, and, ultimately, the scarcity of precious metals. As trust in institutions wanes, the "boring" reality of gold becomes the most interesting story in finance.