Silver has weathered a turbulent few weeks, characterized by sharp price swings and a paradoxical cooling of the physical market that has left many investors questioning the long-term thesis of a supply-side squeeze. As the metal retraced from its dizzying January heights of $121.67 toward the $68 mark in early June, the narrative of a "silver shortage" appeared to be unraveling. However, a deeper analysis of the market’s plumbing suggests that the apparent abundance in vaults is not a sign of supply-demand equilibrium, but rather a temporary byproduct of macroeconomic sentiment and speculative positioning.

The Macroeconomic Backdrop: A Volatile Spring

The recent price action in the silver market has been dictated less by industrial fundamentals and more by the shifting sands of global monetary policy and geopolitical tensions. Early June saw silver prices slide toward the $68-per-ounce level, pressured by a series of robust economic indicators that forced the market to reconsider the Federal Reserve’s trajectory. Investors braced for a "higher-for-longer" interest rate environment, which traditionally acts as a headwind for non-yielding assets like precious metals.

However, the tide turned mid-month. The emergence of a US-Iran peace framework acted as a significant catalyst, easing the energy-related inflationary pressures that had been plaguing global markets. As the energy shock subsided, silver prices found their footing, rallying back toward the $70.40 level by June 16. While the metal remains roughly 42% off its January peak, it has largely clawed back its year-to-date losses.

Market participants are now turning their attention to the Federal Reserve’s pivotal June 16–17 meeting. Under the new leadership of Chair Kevin Warsh, the central bank is expected to hold rates steady, a decision that has already been largely priced in by futures markets. With the immediate threat of a December rate hike dampened, the "macro tape" is once again providing a stable, if not supportive, environment for silver.

Chronology of a Market Correction

To understand why the silver market appears to have loosened, one must look at the sequence of events over the last quarter.

- Late 2025: The silver market was defined by a severe liquidity squeeze. London vault holdings drained rapidly, and the cost of borrowing physical silver—the lease rate—skyrocketed to an alarming 39%. During this period, the shortage was tangible, with premiums on physical bullion hitting record highs.

- May 2026: The narrative shifted. In a move that surprised many analysts, the US Mint reported zero sales of American Silver Eagle bullion coins for the month. Simultaneously, warehouse stocks in COMEX-approved facilities began to swell.

- Early June 2026: As macroeconomic data pointed toward tighter monetary policy, silver prices dipped, prompting a retreat by speculative traders.

- Mid-June 2026: Stabilization returned. The geopolitical easing in the Middle East stabilized energy markets, and the US-Iran framework cooled inflationary fears, allowing silver to recover from its June lows.

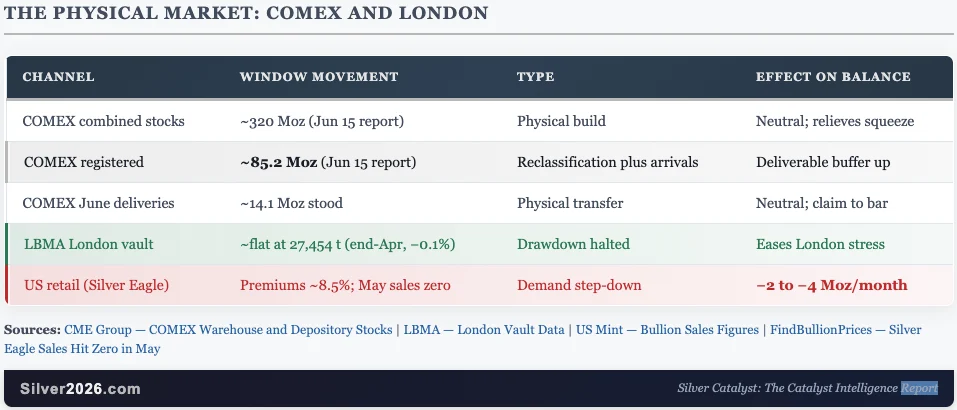

Deconstructing the Physical Market: COMEX and London

The most common error among retail investors is the interpretation of COMEX warehouse data. When vaults fill, the immediate assumption is that supply is finally meeting demand. Yet, the data tells a different story.

The COMEX Mechanics

By June 15, total silver stocks in COMEX warehouses reached approximately 320 million ounces. Of this, 85.2 million ounces were classified as "registered"—metal available for delivery against futures contracts. The growth in this category was not driven by a sudden influx of new mine supply, but by a logistical shift. Warehouses reclassified "eligible" metal (metal stored but not for sale) into the "registered" category to meet the physical requirements of the June delivery cycle.

Crucially, roughly 14.1 million ounces stood for June delivery. This indicates that despite the exit of speculative traders, institutional buyers were still aggressively seeking to secure real, physical metal. The "easing" of the market was a matter of administrative reclassification, not an end to the underlying scarcity.

The London Vault Stability

In the London market, the picture remained one of steadying after a chaotic late-2025. Vault holdings remained flat at 27,454 tonnes, representing a minor 0.1% decline over the month. This suggests that the "squeeze" has transitioned from an acute crisis to a persistent, structural tightness. The high lease rates seen earlier have normalized, but the market has not returned to the surplus conditions of previous years.

The Retail Divergence

The most striking anomaly remains the US Mint’s zero-sale month for Silver Eagles. This is a historical outlier; it is the first full month of zero sales since the program’s inception in the 1980s. However, context is vital: this was not a supply-side suspension by the Mint, but a demand-side strike by wholesalers.

Retail investors, discouraged by the price drop and the historically high premiums (which had surged between 12% and 20% during the squeeze), largely stepped away from the market. Dealers, left holding inventory purchased at higher prices, ceased their orders from the Mint to clear existing stock at discounted rates. This represents a localized retail slump, estimated at roughly 2 to 4 million ounces per month, rather than a global collapse in silver demand.

Implications for Investors

The primary takeaway from this volatility is the necessity of distinguishing between price-driven sentiment and structural supply-demand balances.

- The Structural Deficit Persists: According to projections from the Silver Institute and Metals Focus, 2026 is on track to record its sixth consecutive annual shortfall, estimated at 46.3 million ounces. The physical plumbing of the market has not resolved this fundamental disconnect between production and industrial/investment consumption.

- Sentiment vs. Reality: The recent filling of exchange vaults is a downstream effect of price fluctuations. When the price falls, speculative "paper" silver is sold off, and physical metal is moved to vaults to satisfy delivery obligations. This is not the same as a surge in new mine supply entering the market.

- The Role of Volatility: Silver’s round trip—from $121 to $68 and back—is a testament to how thin the market remains. Because the market is relatively small compared to gold or broader equity indices, it acts as a levered instrument that amplifies investor sentiment.

For the long-term investor, the lesson is clear: do not mistake a cooling retail market for a resolution of structural supply issues. The "shortage" narratives were never about coin availability at a local dealer; they were about the availability of large, good-delivery bars for institutional and industrial users. That market remains tight.

As the macroeconomic landscape stabilizes and the market prices out the immediate rate-hike risk, the silver market is showing signs of renewed vigor. A physical market that loosened during a period of price exhaustion is uniquely positioned to tighten again as the price trajectory turns upward. The "vault build" observed in June is a temporary state in a market that remains fundamentally short of the metal required to meet the demands of a modern, decarbonizing, and electrified economy. Investors would be well-advised to look past the monthly sales data and focus on the widening, persistent gap in the global supply chain.