Main Facts: A New Chair Faces a Historic Monetary Policy Dilemma

This week, all eyes in the global financial community are fixed on Washington as Kevin Warsh chairs his inaugural Federal Open Market Committee (FOMC) meeting. Warsh assumes leadership of the Federal Reserve at a highly volatile juncture. With headline inflation on track to surpass 4% in May, the central bank faces a critical policy decision: should it maintain its current interest rate posture or initiate a new round of rate hikes to combat persistent price pressures?

The federal funds rate currently sits in a range of 3.50% to 3.75%. The debate unfolding around the FOMC table will be pivotal for the trajectory of the U.S. economy. However, a parallel institutional battle is complicating this policy decision. Warsh has long been a vocal critic of the Fed’s communication strategies, particularly the Summary of Economic Projections (SEP) and its famous "dot plot." His efforts to rein in forward guidance could inadvertently obscure a hawkish shift within the committee.

If the Fed’s internal deliberations are masked, market participants could face an unwelcome surprise if the central bank ultimately decides to raise rates later this year. Economists warn that such communication gaps and the resulting market uncertainty could drive up borrowing costs across the economy, complicating the Fed’s primary mission.

Key Variables in the Fed's Current Equation:

┌────────────────────────────────────────────────────────────────────────┐

│ • Current Fed Funds Rate: 3.50% – 3.75% │

│ • Projected May Inflation: > 4.0% │

│ • Inflation Duration: Above the 2% target for over 5 consecutive years │

│ • Primary Catalyst: Middle East energy supply shock │

│ • Institutional Tension: Warsh's push to scale back the SEP "dot plot" │

└────────────────────────────────────────────────────────────────────────┘Chronology: The Path to a Five-Year Inflation Overshoot

To understand the stakes of this week’s FOMC meeting, one must trace the compounding economic developments of the last several years. The current policy dilemma is the culmination of structural supply shocks, evolving monetary frameworks, and geopolitical instability.

CHRONOLOGY OF THE INFLATION CRUCIBLE

─────────────────────────────────────────────────────────────────────────

2021–2024: Pandemic Recovery & Structural Shocks

Supply chain disruptions and massive fiscal stimulus push

inflation well above the Fed's 2% target. The central bank

embarks on an aggressive tightening cycle.

Late 2025: Labor Market Stabilization

The intense labor shortages of the post-pandemic era begin

to cool. The employment side of the Fed's dual mandate

returns to a sustainable equilibrium.

Early 2026: The Geopolitical Energy Shock

Conflict in the Middle East triggers a major energy supply

disruption. Oil and gas prices spike globally, layering new

inflationary pressures onto an already elevated baseline.

March 2026: The Dovish March SEP

The FOMC's Summary of Economic Projections continues to

signal that rate cuts are the most likely next step for

the policy rate in 2026.

May 2026: Inflation Accelerates

Headline inflation metrics surge, tracking to top 4% for

the month. Markets begin pricing in the possibility of

rate hikes rather than cuts.

June 2026: The Warsh Debut

Kevin Warsh chairs his first FOMC meeting amid a deeply

divided committee and intense debate over whether to

abandon the "look-through" approach to supply shocks.

─────────────────────────────────────────────────────────────────────────For more than five years, U.S. inflation has stubbornly remained above the Federal Reserve’s formal 2.0% target. Initially triggered by pandemic-era supply chain snarls and fueled by unprecedented fiscal and monetary accommodation, price pressures proved far more durable than policymakers originally anticipated.

By late 2025, there was brief cause for optimism. The labor market, which had been overheating for years, began to stabilize. The risk of a wage-price spiral appeared to recede, suggesting that the Fed might successfully engineer a soft landing.

However, this stabilization was quickly overshadowed by a severe geopolitical shock. Escalating conflict in the Middle East disrupted global energy supplies, causing crude oil and fuel prices to surge. This energy shock hit an economy that had already endured half a decade of elevated living costs.

Consequently, by May, headline inflation was accelerating toward the 4% threshold. This forced a dramatic shift in market expectations. While the FOMC’s March Summary of Economic Projections had signaled that rate cuts would be appropriate by the end of the year, the reality of persistent inflation has turned the policy debate upside down as the committee convenes this week.

Supporting Data: Diverging Forecasts and the Policy Split

The division within the monetary policy community is illustrated by contrasting data points from recent surveys and official projections.

Historically, the standard central banking response to an energy supply shock is to "look through" it. Because raising interest rates cannot produce more oil or repair disrupted shipping lanes, tightening policy in response to a supply shock typically serves only to depress domestic demand, making households poorer without resolving the underlying supply constraint.

However, the argument for an interest rate hike is gaining traction due to the duration of the inflation overshoot.

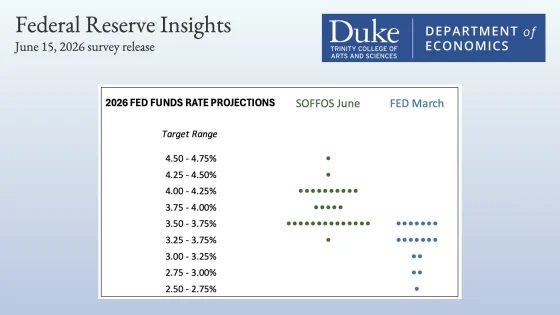

The shift in sentiment is highly visible when comparing the official March FOMC projections with the June Survey of Former Fed Officials and Staff (SOFFOS), conducted by veteran financial journalist Jon Hilsenrath.

The Policy Shift: March SEP vs. June SOFFOS Survey

| Source / Cohort | Favoring Rate Cuts | Favoring No Change (Hold) | Favoring Rate Hikes |

|---|---|---|---|

| March FOMC SEP (Current Officials) | Majority | Minority | Very Few / None |

| June SOFFOS Survey (Former Officials/Staff) | 1 | 14 | 17 (Most favoring $ge$ 50 bps) |

The SOFFOS survey reveals a significant hawkish shift among monetary policy insiders:

- 17 respondents argued that a rate hike is appropriate this year.

- 14 respondents favored keeping rates unchanged.

- Only 1 respondent advocated for a rate cut.

- Notably, of those favoring a hike, the majority argued that a substantial move of 50 basis points or more is required to regain control of the inflation narrative.

This stands in stark contrast to the actual March SEP, where the consensus of sitting Fed officials pointed toward rate cuts. While markets have partially adjusted to this reality by pricing in higher-for-longer yields, a formal shift in the Fed’s own projections—such as the median dot in the June SEP plotting a rate hike—would still represent a major shock to the financial system.

Official Responses: The Intellectual Battle Lines

The debate over how to handle prolonged, supply-driven inflation has divided some of the most prominent minds in monetary economics. The dispute centers on whether the central bank should adhere to traditional economic models or adapt its strategy to address the psychological toll of multi-year inflation.

THE INTELLECTUAL DIVIDE ON SUPPLY SHOCKS

─────────────────────────────────────────────────────────────────────────

▲ THE DURATION CAMP (Pro-Hike)

• Proponents: Christy & David Romer, Beth Hammack (Cleveland Fed)

• Core Argument: Five years of inflation has eroded public trust.

Even if a shock is technically transitory, its extended duration

requires a policy response to anchor expectations and demonstrate

commitment.

• Action: Raise interest rates to curb demand and show resolve.

▼ THE STANDARD CAMP (Pro-Hold)

• Proponents: Janet Yellen, Traditional Monetary Economists

• Core Argument: Supply shocks cannot be resolved by monetary policy.

Raising rates does not solve energy shortages; it merely punishes

consumers twice—once via high fuel prices, and again via higher

borrowing costs.

• Action: Maintain a watchful hold; avoid unnecessary economic damage.

─────────────────────────────────────────────────────────────────────────The Romer-Romer Argument for Action

At a recent conference analyzing the legacy of the Powell Fed, monetary policy experts Christina and David Romer presented a paper arguing that the traditional "look-through" approach has clear limits when supply shocks persist over long horizons. They noted:

"…faced with a shock whose impact on the price level is likely to play out over an extended period, but whose effect on inflation is likely to ultimately be transitory if inflation expectations remain stable, policymakers should focus less on inflation expectations and more on the inflation itself, and so be more willing to respond. This could temper the inflation, and so reduce its harms. And more speculatively, by showing policymakers’ concern, it might at least marginally reduce the anger caused by the inflation."

This perspective has found support within the FOMC. Cleveland Fed President Beth Hammack has echoed similar logic regarding duration, suggesting that rate hikes may be necessary this year to defend the credibility of the 2% target, even if the primary driver is an energy supply disruption.

The Yellen Counter-Argument

This activist view is not universally accepted. Treasury Secretary and former Fed Chair Janet Yellen strongly disputed the Romers’ conclusions during the same event. Yellen reaffirmed the classic consensus: raising rates in response to a supply shock is an inefficient tool that risks causing unnecessary economic pain. Because rate hikes suppress demand rather than restoring supply, they can lead to lower growth and employment without directly lowering energy prices.

Warsh’s Communication Dilemma

Compounding this policy debate is Kevin Warsh’s philosophy on central bank communication. Warsh has spent years criticizing the "dot plot" and explicit forward guidance, arguing that these tools:

- Promote a false sense of certainty among investors.

- Pressure committee members toward a premature consensus.

- Limit the Fed’s flexibility to react to sudden economic data changes.

Reports suggest that Warsh might choose not to submit his own interest rate forecasts for the June SEP, and other officials may follow his lead. While this would align with his goal of reducing the market’s reliance on forward guidance, doing so during a period of high inflation and internal division carries significant risks.

Implications: The High Cost of Central Bank Silence

The intersection of a deeply divided FOMC and a potential reduction in policy communication has significant implications for financial markets and the broader economy.

┌────────────────────────────────────────┐

│ Kevin Warsh Limits SEP / Dot Plot │

└───────────────────┬────────────────────┘

│

┌─────────────┴─────────────┐

▼ ▼

┌──────────────────────────┐ ┌──────────────────────────┐

│ Obscures Hawkish Shift │ │ Creates Communication │

│ Within the Committee │ │ Vacuum │

└─────────────┬────────────┘ └────────────┬─────────────┘

│ │

└─────────────┬─────────────┘

▼

┌──────────────────────────────────────────────────────┐

│ • Markets are caught off guard by eventual rate hike │

│ • Investors demand higher risk premiums │

│ • Borrowing costs rise due to uncertainty │

│ • Central bank credibility is eroded │

└──────────────────────────────────────────────────────┘1. The Risk of a Communication Vacuum

If the Fed dampens the signal from the SEP, it risks creating a communication vacuum at a highly sensitive moment. With headline inflation rising, any reduction in transparency could be interpreted by markets as an attempt to downplay or hide a hawkish shift within the committee. This perception of complacency could erode the Fed’s hard-won inflation-fighting credibility.

2. Market Volatility and Risk Premiums

While markets have already begun pricing in the possibility of a rate hike, there is a distinct difference between investors hedging their bets and the Fed officially signaling a policy pivot. If the central bank conceals its internal debate, the eventual realization that a rate hike is on the table could trigger significant market volatility. To compensate for this uncertainty, investors may demand higher risk premiums, leading to a tightening of financial conditions.

3. Real-World Borrowing Costs

An increase in market uncertainty is not just an issue for Wall Street; it has tangible consequences for the broader public. When investors cannot clearly discern the Fed’s policy path, they demand higher yields on Treasury securities. This upward pressure quickly transmits to consumer borrowing costs, driving up interest rates on mortgages, auto loans, and business credit.

4. Squeezing the Consumer

If the Fed decides to hike rates, the economic consequences will be felt directly by American households. A rate hike does not drill more oil or lower utility bills; instead, it reduces aggregate demand by squeezing the financial capacity of families already dealing with high prices. For many workers, the primary cost of such tightening is not necessarily a lost job, but rather stagnant wages and reduced economic opportunity.

How Policy Decisions Transmit to Households:

┌────────────────────────────────────────────────────────────────────────┐

│ • Standard Hold: Allows energy shock to pass; avoids further squeeze │

│ on households, but risks unanchoring long-term expectations. │

│ │

│ • Duration-Based Hike: Seeks to anchor expectations and lower prices │

│ by curbing demand; risks raising borrowing costs and slowing wage │

│ growth for families already facing high energy costs. │

└────────────────────────────────────────────────────────────────────────┘The Path Forward

To manage these risks, some analysts suggest that Chair Warsh should participate in the June SEP while using his press conference to clarify its role. By framing the "dot plot" as a collection of individual, non-binding assessments rather than a rigid policy commitment, Warsh could address his concerns about forward guidance without sacrificing transparency during a critical policy debate.

Ultimately, the key task for the Fed this week is not just deciding whether to hold or hike, but ensuring that its decision-making process is clear to the public. In a complex economic environment, demonstrating a thorough, well-debated response is the most effective way for the central bank to maintain credibility and anchor long-term expectations.