In global financial capitals, the phrase "rate cut" has transformed from a policy objective into an unspoken taboo. Across the Federal Reserve, the European Central Bank (ECB), and the Bank of England (BoE), monetary policymakers are publicly projecting a stern, unyielding commitment to restrictive policy. Inside the ECB’s Frankfurt headquarters, observers jokingly whisper that mentioning a downward shift in interest rates is a punishable offense—perhaps resulting in a mandatory seminar at the German Bundesbank on the inflation crises of the 1970s.

Yet beneath this hawkish consensus lies a growing disconnect between official rhetoric and shifting macroeconomic fundamentals. While futures markets are pricing in higher interest rates across the developed world—with no meaningful cuts expected before 2028—a contrarian case is building.

Led by insights from ING’s economics team, including Developed Markets Economist James Smith, a alternative narrative suggests that central banks could be forced to reverse course much sooner than investors realize. Rather than entering an era of permanently elevated interest rates, the global economy may be on the cusp of a significant policy easing cycle within the next 12 to 18 months.

Main Facts: The Great Monetary Disconnect

The core divergence in today’s macroeconomic landscape lies between market pricing and underlying economic indicators. Currently, financial markets are betting heavily on a "higher-for-longer" interest rate environment:

- Market Expectations: Investors have priced in an additional 50 basis points of rate hikes in the United States over the next twelve months, with the Eurozone and the United Kingdom projected to follow a similar upward trajectory.

- The Consensus View: Driven by fears of sticky service-sector inflation and resilient labor markets, consensus pricing suggests that benchmark interest rates will not return to neutral levels until the end of the decade.

- The Contrarian Case: Analysts at ING argue that this outlook fundamentally misinterprets the structural forces driving inflation and employment. They project that monetary policy will be looser, not tighter, by mid-2026.

This counter-thesis rests on a systematic overestimation of labor market strength, a failure to account for the lag in housing cost calculations, and an overreaction to temporary "second-round" inflation fears in Europe and the UK.

Market Expectations vs. Macroeconomic Reality

┌──────────────────────────────────────┬──────────────────────────────────────┐

│ Market Consensus │ Contrarian Analysis │

├──────────────────────────────────────┼──────────────────────────────────────┤

│ • Rates 50bp higher in 12 months │ • Policy easing within 12-18 months │

│ • No rate cuts priced before 2028 │ • Housing/rent deflation accelerating│

│ • Labor markets unsustainably tight │ • Job growth concentrated, slowing │

│ • Sticky European service inflation │ • Food & energy pressures fading │

└──────────────────────────────────────┴──────────────────────────────────────┘Chronology: How the "Higher-for-Longer" Consensus Was Forged

To understand why markets are mispricing the interest rate path, it is necessary to trace the policy shifts and narrative transitions of the recent past.

Timeline of the Monetary Policy Shift

┌───────────────────┬────────────────────────────────────────────────────────┐

│ Period │ Key Monetary & Macroeconomic Event │

├───────────────────┼────────────────────────────────────────────────────────┤

│ Late 2024 │ Initial hopes of rapid global rate cuts fade as │

│ │ inflation exhibits persistent volatility. │

├───────────────────┼────────────────────────────────────────────────────────┤

│ Mid-2025 │ The Bank of England pauses its easing cycle, citing │

│ │ rising food prices and minimum wage pressures. │

├───────────────────┼────────────────────────────────────────────────────────┤

│ Late 2025 │ Kevin Warsh assumes the Chairmanship of the Federal │

│ │ Reserve, immediately adopting a hawkish stance. │

├───────────────────┼────────────────────────────────────────────────────────┤

│ Early 2026 │ The Fed's "Wednesday Meeting" confirms a shift toward │

│ │ policy "recalibration" rather than near-term cuts. │

├───────────────────┼────────────────────────────────────────────────────────┤

│ Mid-2026 (Current)│ Markets price in hikes; food inflation begins to │

│ │ drop sharply across Europe and the UK. │

└───────────────────┴────────────────────────────────────────────────────────┘The pivot began in earnest in late 2024 and early 2025, when initial expectations of rapid, synchronized global rate cuts began to stall. In the United Kingdom, the Bank of England’s hawkish wing sounded alarms over a confluence of domestic cost pressures, including rising food prices, hikes in employer taxes, and a substantial increase in the national minimum wage. Consequently, the BoE slowed its projected path of policy easing, setting a cautious tone for other central banks.

By the time Kevin Warsh assumed the Chairmanship of the Federal Reserve, the institutional mood had shifted entirely toward caution. Warsh lost no time in asserting his hawkish credentials, establishing five separate internal taskforces in his first week to evaluate systemic inflation risks and structural changes in the U.S. economy.

The Fed’s recent Wednesday policy meeting served as a stark wake-up call for remaining market doves. Rather than signaling an imminent "recalibration" of interest rates downward, the meeting revealed a deeply divided Federal Open Market Committee (FOMC). Warsh emerged as just one of twelve voters, with a significant faction of the remaining eleven members actively making the case for further rate hikes before the end of the year.

This hawkish shift solidified the market belief that interest rates would remain elevated through the end of the decade.

Supporting Data: Debunking the Three Pillars of Hawkishness

The Federal Reserve’s hawkish posture rests on three core assumptions: a booming labor market, sticky core inflation running above the 2% target, and a belief that the neutral rate of interest ($r^*$) has risen, meaning current policy is not as restrictive as once thought. However, a closer inspection of the economic data reveals vulnerabilities in each of these assumptions.

1. The Illusion of US Labor Market Strength

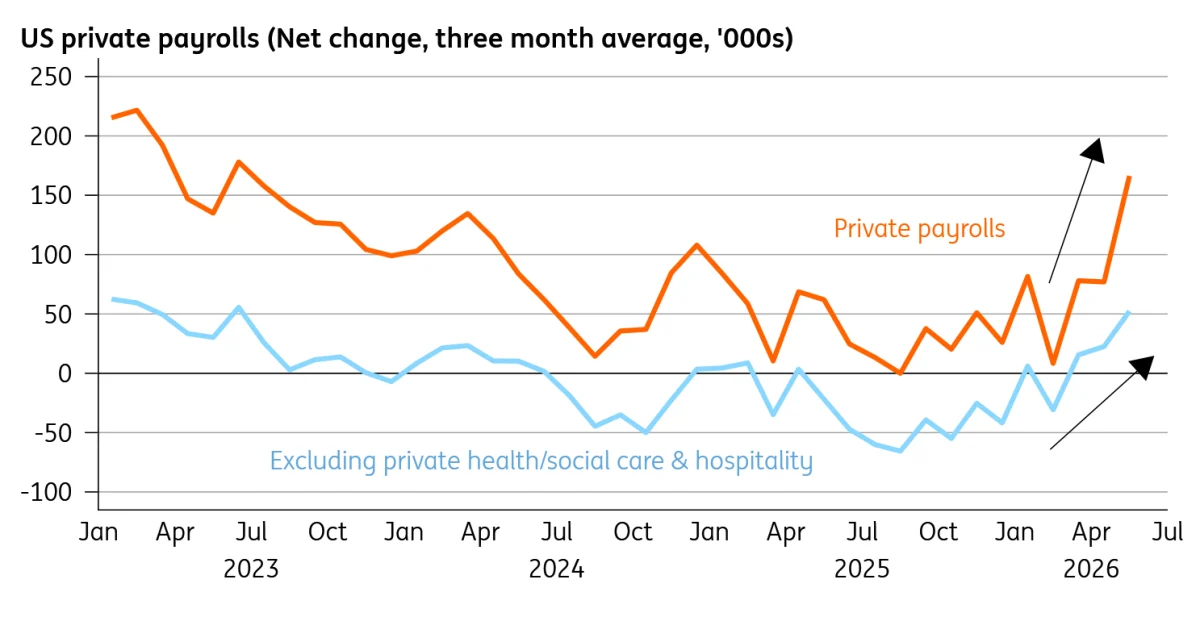

While headline payroll figures continue to surprise to the upside, the composition of this job growth is highly unbalanced.

An analysis of recent private payroll data reveals that two sectors—private healthcare/social assistance and hospitality—account for nearly two-thirds of all job growth, despite representing only a quarter of total employment.

U.S. Private Payroll Growth Distribution

┌──────────────────────────────────────────────┐

│ ████████████████████████ 66% Healthcare/Hospitality (1/4 of Total Jobs)

│ ████████████ 34% All Other Sectors Combined (3/4 of Total Jobs)

└──────────────────────────────────────────────┘When these highly specific, non-cyclical sectors are excluded, the broader hiring landscape appears far more subdued. More importantly, this concentrated employment growth has failed to translate into systemic wage growth. Without broad-based wage-push pressures, the labor market does not pose the structural inflation risk that hawkish policymakers fear.

2. The Impending Rental Deflation Wave

The second pillar of the hawkish thesis is core inflation, which has remained sticky. However, core consumer price index (CPI) calculations are heavily weighted toward housing costs, specifically rents and Owners’ Equivalent Rent (OER). These metrics are notoriously lagging indicators, reflecting lease agreements signed up to a year prior.

As noted by ING’s James Knightley, real-time rental market indicators show that spot rents are barely rising. As these current market dynamics gradually filter into the official government calculations over the coming quarters, core CPI is poised to decline significantly. When combined with falling fuel prices, a correction in volatile airfare costs, and the fading impact of international tariffs, the domestic drivers of U.S. inflation are set to weaken.

3. European Food Inflation and the January Price Resets

In Europe, the narrative of sticky inflation is also showing signs of strain. Although ECB President Christine Lagarde has warned of potential "second-round effects"—where initial energy and food price shocks lead to spiraling wage demands—the empirical evidence tells a different story.

May Food Inflation Trends (Year-over-Year Change)

┌─────────────────────────────────┬───────────────────┐

│ Region │ Inflation Trend │

├─────────────────────────────────┼───────────────────┤

│ Eurozone │ Sharp Decrease │

│ United Kingdom │ Sharp Decrease │

│ Eastern Europe │ Sharp Decrease │

└─────────────────────────────────┴───────────────────┘In May, food inflation fell sharply across the Eurozone, the UK, and key Eastern European markets. Because food is a highly visible, high-frequency purchase, its rapid decline is crucial for anchoring household inflation expectations.

Furthermore, as noted by Carsten Brzeski, January remains the critical month for European inflation, as it is the period when the vast majority of corporations execute their annual price resets. If energy prices continue to stabilize and consumer demand softens, these resets are likely to be far more conservative than in previous years, undermining the ECB’s justification for "insurance" rate hikes.

Official Responses: Rhetoric vs. Policy Realities

The public pronouncements from major central banks remain resolutely hawkish, even as economic indicators begin to turn.

At the Federal Reserve, Chair Kevin Warsh has focused on institutional restructuring, using his newly formed taskforces to investigate structural inflation risks. This administrative focus has signaled to markets that the Fed is in no hurry to ease policy, viewing current interest rate levels as appropriate or even slightly accommodative given the headline data.

Central Bank Stances vs. Underlying Indicators

┌─────────────────┬───────────────────────────────┬───────────────────────────────┐

│ Central Bank │ Public Policy Stance │ Undercurrents & Indicators │

├─────────────────┼───────────────────────────────┼───────────────────────────────┤

│ Federal Reserve │ Recalibration of policy; │ Warsh acknowledges tight │

│ │ potential hikes on the table │ housing conditions; jobs soft │

├─────────────────┼───────────────────────────────┼───────────────────────────────┤

│ European │ Warning of second-round │ Sharp drops in May food CPI; │

│ Central Bank │ effects; summer hike bias │ wage pressures stabilizing │

├─────────────────┼───────────────────────────────┼───────────────────────────────┤

│ Bank of │ Cautious pause; vigilance │ Historical victory of doves; │

│ England │ on minimum wage and taxes │ core inflation cooling │

└─────────────────┴───────────────────────────────┴───────────────────────────────┘Meanwhile, the ECB continues to emphasize the risk of wage-price spirals. Christine Lagarde’s recent statements highlight a persistent anxiety that wage growth could trigger a self-reinforcing inflationary loop. This hawkishness has set the stage for a potential "insurance" rate hike this summer, intended to guarantee that inflation returns to the 2% target.

Yet, this official stance closely mirrors the Bank of England’s policy trajectory from a year ago. In mid-2025, BoE hawks warned of wage-push inflation and fiscal policy shocks, slowing their projected path of rate cuts.

By early 2026, however, those fears had largely dissipated. Internal BoE analyses concluded that the risk of second-round effects had faded, allowing the doveish faction of the Monetary Policy Committee to declare victory as wage and price data normalized. This British experience serves as a highly plausible blueprint for both the Federal Reserve and the ECB over the next twelve months.

Implications: The Looming Bond Market Reversal

If the contrarian analysis presented by James Smith and the ING economics team proves correct, the implications for global financial markets will be profound, particularly for fixed-income assets.

Currently, bond markets are priced for a "higher-for-longer" scenario, with yield curves reflecting expectations of elevated policy rates for years to come. A sudden realization that central banks must transition from hiking or holding to active policy easing would trigger a sharp downward adjustment in yields.

Portfolio Reallocation Under Policy Pivot

┌──────────────────────────────┬──────────────────────────────┐

│ Current High-Rate Position │ Projected Easing Position │

├──────────────────────────────┼──────────────────────────────┤

│ • Short-duration cash focus │ • Lock in long-term yields │

│ • Floating-rate debt bias │ • Shift to fixed-rate assets │

│ • Defensive equity posture │ • Growth & rate-sensitive eq.│

└──────────────────────────────┴──────────────────────────────┘Investors who have locked in short-term, high-yielding cash instruments may find themselves reinvesting at much lower rates. Conversely, long-duration government and corporate bonds would see significant capital appreciation.

For the real economy, a shift toward rate cuts in late 2026 would provide timely relief to highly leveraged corporate borrowers and the residential real estate sector. In the United States, where housing activity has been constrained by mortgage rates hovering near multi-decade highs, a Fed pivot would help unfreeze the housing market. In Europe, avoiding unnecessary "insurance" hikes would prevent central banks from inadvertently pushing the continental economy into a deeper, structural slowdown.

Ultimately, the current hawkishness of global central banks may represent the high-water mark of the tightening cycle. While policymakers feel compelled to maintain a stern countenance to manage public expectations, the underlying economic data is quietly preparing the ground for a policy reversal. By this time next year, the debate may no longer be about how high rates must go, but how quickly they need to come down.