Main Facts: The Great Sentiment Paradox

In May, the University of Michigan’s consumer sentiment index registered a reading of 44.8. To place this figure in historical perspective, it represents the lowest level recorded since the survey’s inception in 1952. The print is lower than the depths of the 2008 Great Financial Crisis, more severe than the inflation panic of 1980, and lower than the acute anxiety during the 2020 COVID-19 lockdowns. Under normal economic paradigms, a sentiment reading of this magnitude would point to a nation mired in a severe, multi-year economic depression.

Yet, the broader United States economy continues to show remarkable resilience, presenting a stark paradox for economists and market participants alike. While consumers tell surveyors they are deeply pessimistic, their actual economic behavior paints an entirely different picture:

- Robust Gross Domestic Product (GDP): Real GDP has been growing at a healthy annualized rate of 2.7%.

- Strong Corporate Earnings: First-quarter corporate earnings posted 27% year-over-year growth, with an 84% beat rate on the S&P 500—well above the five-year average of 78%. Aggregate earnings beat estimates by 20.7%, marking the strongest positive surprise rate since the first quarter of 2021.

- A Resilient Labor Market: Weekly jobless claims remain near cyclical lows, printing at 209,000 for the week ending May 16, while the national unemployment rate sits at a historically low 4.3%.

- Active Consumer Spending: Retail sales rose 0.5% in April, representing a 4.9% increase compared to the previous year.

- Strong Growth Projections: The Atlanta Fed’s GDPNow forecasting model estimated annualized second-quarter growth at 4.3% as of late May.

This glaring disconnect between subjective consumer feelings and objective economic data has sparked intense debate. On social media and among heterodox economic commentators, assertions have spread that official GDP statistics are "completely broken" and fail to reflect a hidden recession. However, when multiple independent hard data series—including labor market strength, retail sales, corporate earnings, and credit trends—all align in a positive direction, it is far more likely that the sentiment surveys themselves are failing to capture true economic reality.

Chronology of the Divergence

To understand how this disconnect formed, it is necessary to examine the historical relationship between consumer sentiment and macroeconomic growth.

[Pre-2022] Sentiment & GDP move in tandem (e.g., 2001, 2008, 2020 Recessions)

│

[2022] ───► High inflation begins; GDP remains stable at +2% to +3%

│ UMich Sentiment plunges and stays below 70 (Historical Recession Levels)

│

[2024] ───► UMich transitions from phone to online-only surveys (April-July)

│ An 8.9-point structural drop is introduced into the index

│

[2025] ───► Political transition triggers sharp partisan sentiment shifts

│ (Republicans surge; Democrats plunge)

│

[May 2026]► Gasoline shocks and tariff fears cause bipartisan drop to 44.8

Hard economic data (spending, jobs, earnings) remains robustFor the quarter-century preceding 2022, consumer sentiment and economic growth moved roughly in tandem. During the mild recession of 2001, the devastating 2008 financial crisis, and the sudden economic stoppage of the 2020 pandemic lockdowns, consumer sentiment and GDP contracted and recovered in lockstep.

This historical correlation broke down in 2022. For over three years, US GDP has consistently expanded between 2% and 3% year-over-year. Yet, over this entire period, the University of Michigan’s consumer sentiment index has remained stubbornly below the key threshold of 70—a level that historically occurred only during deep economic contractions.

The divergence deepened due to political transitions. In January 2021, following the inauguration of President Joe Biden, Democratic sentiment surged while Republican sentiment plunged. This dynamic repeated itself in January 2025: Republican sentiment surged from 67 to 93 within two months, while Democratic sentiment plummeted from 78 to 56.

By May 2026, the sentiment index reached its historic low of 44.8. This drop occurred alongside a 12.3% monthly spike in gasoline prices due to geopolitical tensions in the Middle East and supply disruptions in the Strait of Hormuz, alongside rising concerns over tariff-related price pressures. Despite these headwinds, real-world metrics like retail sales and employment have remained highly stable.

Supporting Data and Methodological Shifts

The divergence between consumer sentiment and economic reality is driven by three main factors: partisan polarization, a major structural change in survey methodology, and differing survey designs.

The Partisan Gap and Asymmetric Amplification

The gap in economic perception between self-identified Democrats and Republicans has reached unprecedented levels. Research published by the Richmond Federal Reserve in 2024 revealed that the partisan gap in consumer sentiment is now larger than differences based on income, age, or education.

Under President George W. Bush, the sentiment gap between the two major parties averaged 21 points. This gap widened to 25 points under President Barack Obama, and expanded to 45 points under President Biden.

Partisan Sentiment Gap Over Time (Richmond Fed Study):

======================================================

George W. Bush Era: █████████████ 21 pts

Obama Era: ███████████████ 25 pts

Biden Era: ████████████████████████████ 45 ptsThis polarization is amplified by what researchers at BriefingBook call "asymmetric amplification." When a political party loses the White House, its supporters’ economic sentiment drops significantly more than their opponents’ sentiment rises when they win.

Specifically, Republican respondents adjust their sentiment responses roughly 2.5 times more intensely than Democrats depending on which party controls the presidency. Adjusting the historical data to account for this asymmetry alone resolves approximately 30% of the post-2020 gap between predicted and observed consumer sentiment.

Furthermore, analysis by Fundstrat’s Tom Lee highlighted that during highly polarized periods, sentiment surveys can function as political protest votes rather than objective economic assessments. Lee noted that in recent survey cohorts, 51% of Democratic respondents reported sentiment readings below the survey’s historical all-time low of 47.6, while nearly 25% of respondents claimed that inflation was running above 100%—a figure completely detached from actual price indices.

The Shift to Online Surveying

A major structural shift in how the University of Michigan collects its data has also contributed to the decline in its sentiment index. Between April and July of 2024, the university transitioned its data collection from random-digit-dialed cell phone interviews to an online-only, address-based sampling method.

Impact of Survey Methodology Shift (2024):

┌────────────────────────────────────────────────────────┐

│ Old Method: Random-Digit Cell Phone Dialing │

└───────────────────────────┬────────────────────────────┘

│ Methodology Change

▼

┌────────────────────────────────────────────────────────┐

│ New Method: Online-Only Address-Based Sampling │

│ • Introduces self-selection bias │

│ • Depresses index by an estimated 8.9 points (~11%) │

│ • Resulting panel: ~66% Dem / ~33% Rep (Tom Lee) │

└────────────────────────────────────────────────────────┘While the survey’s director, Joanne Hsu, stated that the transition yielded comparable results, independent research suggests otherwise. An analysis by economists Cummings and Tedeschi published in BriefingBook concluded that the transition to online-only surveying introduced a structural downward bias, lowering the headline sentiment index by approximately 8.9 points, or more than 11%.

When benchmarked against Morning Consult’s continuous online sentiment survey—which has used the same five core questions since 2018—the University of Michigan index showed a unique drop that was not replicated in Morning Consult’s data.

Additionally, critics have pointed out potential demographic distortions in the online panel. Tom Lee reported that the online format produced a highly skewed respondent pool consisting of roughly 66% Democrats and 33% Republicans, which does not accurately reflect the broader US electorate and introduces a structural bias to the final index.

Comparing the Michigan Survey and the Conference Board

To verify whether the consumer sentiment decline is systemic or survey-specific, economists compare the University of Michigan index with the Conference Board’s Consumer Confidence Index.

The two surveys show a clear divergence:

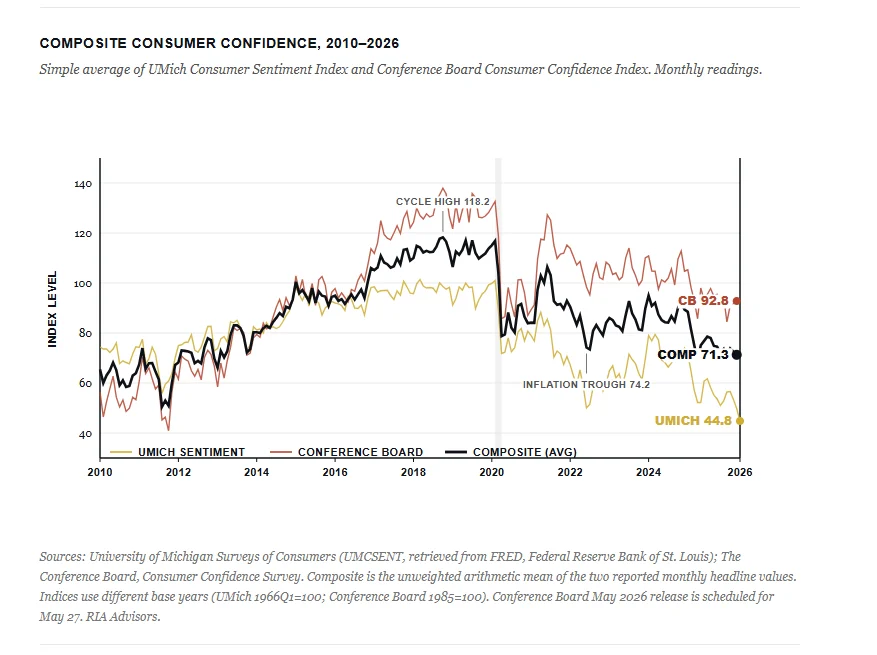

- The University of Michigan Index: Focuses heavily on personal finances, long-term inflation expectations, and big-ticket purchasing conditions. Its Current Economic Conditions component fell 26% below its 2008 financial crisis low.

- The Conference Board Index: Places greater emphasis on labor market health and current business conditions. Its index remains near its long-term average at 92.8—well above its historical recessionary lows, such as the 25.3 reading in 2009 or the 85.7 reading during the 2020 COVID-19 shock.

Because the Conference Board’s methodology focuses on job availability rather than direct inflation expectations, it is less vulnerable to political protest responses regarding cost-of-living increases.

Official Responses and Institutional Perspectives

Major financial and policymaking institutions have long questioned the usefulness of consumer sentiment surveys for predicting actual economic behavior.

Key Institutional Findings on Sentiment vs. Spending:

┌─────────────────────────┬─────────────────────────────────────────────────────────┐

│ Institution │ Core Conclusion / Quote │

├─────────────────────────┼─────────────────────────────────────────────────────────┤

│ Kansas City Fed (2026) │ Sentiment-augmented models do not improve spending │

│ │ forecasts over traditional economic data. │

├─────────────────────────┼─────────────────────────────────────────────────────────┤

│ Federal Reserve Chair │ "The link between sentiment data and consumer spending │

│ Jerome Powell (2025) │ has been weak. It's not been a strong link at all." │

├─────────────────────────┼─────────────────────────────────────────────────────────┤

│ Boston Fed (2014) │ Sentiment's role in predicting consumption is marginal │

│ │ once income, employment, and wealth are controlled. │

└─────────────────────────┴─────────────────────────────────────────────────────────┘In a February 2026 working paper titled "Forecasting with Feelings," researchers at the Kansas City Federal Reserve analyzed thirty years of economic data to determine if consumer sentiment improves consumer spending forecasts. The study compared a standard forecasting model based on hard economic data with an augmented model that included sentiment indices. The researchers concluded that adding sentiment data did not provide any statistically significant improvement in forecasting accuracy.

This conclusion is supported by other Federal Reserve research. A 2014 paper published by the Boston Federal Reserve found that when standard economic fundamentals—such as disposable income, employment growth, and household wealth—are controlled for, the predictive value of consumer sentiment surveys becomes marginal.

Federal Reserve Chair Jerome Powell addressed this issue directly during a May 2025 press conference, stating:

"The link between sentiment data and consumer spending has been weak. It’s not been a strong link at all."

Financial markets have also consistently looked past low sentiment readings. While the composite consumer confidence index—which combines both the Michigan and Conference Board surveys—currently sits at 71 (down 47 points from its 2018 peak of 118), the S&P 500 has more than doubled over the same period.

Historically, there have been three other periods where stock prices rose while consumer sentiment fell: the dot-com expansion of the late 1990s, the mid-cycle expansion of the mid-2000s, and the post-pandemic recovery. In all three instances, real economic activity and asset prices eventually aligned, but the periods of divergence lasted much longer than bearish forecasters anticipated.

Implications for Investors and the Economy

For institutional investors, economists, and corporate strategists, the key takeaway is clear: consumer behavior is a much more reliable indicator than consumer sentiment. When surveys and real-world actions diverge, investment decisions should be guided by hard data.

Tracking Consumer Behavior vs. Sentiment

| Economic Category | Sentiment Survey Response (What People Say) | Real-World Behavioral Data (What People Do) |

|---|---|---|

| Personal Finances | "Our household budget is in a state of crisis." | Real wages are rising; household balance sheets remain historically healthy. |

| Labor Market | "Good jobs are becoming increasingly scarce." | Jobless claims remain near historic lows at 209,000; unemployment is at 4.3%. |

| Retail Consumption | "We are cutting back heavily on discretionary spending." | Retail sales grew 0.5% in April, running 4.9% higher year-over-year. |

| Corporate Health | "The business environment is rapidly deteriorating." | S&P 500 Q1 earnings beat expectations by 20.7%, with an 84% beat rate. |

| Overall Growth | "The country is currently in a deep recession." | Real GDP is growing at 2.7%, with Q2 projections tracking at 4.3%. |

While subjective surveys can be distorted by political bias and methodology changes, several concrete metrics provide a more accurate picture of economic health:

- Gasoline Prices: Retail gasoline prices remain a highly influential variable. The 12.3% rise in April gas prices acts as a direct tax on household budgets and corporate margins. If geopolitical tensions in the Middle East continue to pressure energy markets, demand destruction in cyclical sectors remains a risk.

- Tariff Pass-Through: The fact that 30% of survey respondents spontaneously raised concerns about tariffs indicates that trade policy changes are beginning to affect household expectations. This represents a real inflationary risk that could eventually pressure corporate margins.

- Hard Financial Metrics: Rather than relying on sentiment indices, analysts should monitor credit card delinquency rates, container shipping costs, and corporate margin guidance to identify turning points in the economic cycle.

Ultimately, while consumer pessimism is real and influenced by persistent inflation concerns, history shows that negative sentiment alone does not drive economic recessions. As long as the labor market remains solid and wages grow, consumers are likely to keep spending. For investors, relying too heavily on sentiment surveys during a highly polarized era can lead to costly miscalculations. In the current economic environment, tracking actual consumer spending remains a much more reliable strategy than focusing on consumer sentiment.