Introduction

For the past several years, the global financial and technological markets have been captivated by the software layer of artificial intelligence. Wall Street and Silicon Valley alike have poured hundreds of billions of dollars into large language models, generative design interfaces, and neural network algorithms. Yet, beneath this digital gold rush lies a stark physical reality: the virtual world is entirely dependent on physical infrastructure.

As the training and deployment of AI models expand at an exponential pace, the technological race is rapidly shifting from the abstract realm of software engineering to the concrete challenges of heavy industry. The future of AI will not be decided solely by who writes the most elegant code, but by who secures the largest power grids, engineers the densest cooling hardware, and builds the most robust physical networks. The industry is hitting a physical wall, and overcoming it requires a complete reimagining of the hardware stack.

Main Facts: The Triple Constraint of AI Infrastructure

The physical constraints currently threatening to slow down the artificial intelligence boom can be categorized into three distinct, yet interconnected, physical bottlenecks:

- The Power Grid and Climate Strain: AI data centers require unprecedented amounts of baseload electricity. This surging demand is colliding with aging, underinvested power grids in Europe and North America, a situation further exacerbated by volatile climate anomalies that threaten grid stability.

- The Thermal Bottleneck: The power density of modern AI chips has surpassed the physical limits of traditional air-based cooling systems. Server racks are transitioning from historical power draws of 10–15 kilowatts (kW) to levels exceeding 100 kW, making liquid cooling an absolute operational necessity rather than an optional upgrade.

- The Limits of Copper (The Bandwidth Wall): As data transfer speeds inside data centers reach 224 Gigabits per second (Gbps) and beyond, copper cables suffer from extreme signal degradation and heat generation. Light-based data transmission, or photonics, is emerging as the only viable pathway to scale internal networks without running into a physical bandwidth wall.

Chronology: The Evolution of the AI Infrastructure Bottleneck

To understand how the technology sector arrived at this physical impasse, it is necessary to trace the evolutionary phases of the modern AI boom:

+---------------------------------------------------------------------------------+

| CHRONOLOGY OF THE AI BOOM |

+---------------------------------------------------------------------------------+

| |

| [2020 - 2023] PHASE 1: Algorithmic Scaling & Software Breakthroughs |

| * Launch of GPT-3 and early LLMs. |

| * Focus remains on parameter counts, fine-tuning, and algorithmic efficiency. |

| * The industry views AI primarily as a software and cloud application play. |

| |

| [2023 - 2025] PHASE 2: Silicon Scarcity & GPU Land Grabs |

| * Massive capital expenditures on NVIDIA H100s, H200s, and early Blackwell. |

| * Tech giants rush to secure advanced semiconductor manufacturing capacity. |

| * Physical bottlenecks emerge in packaging (CoWoS) and basic chip supply. |

| |

| [2025 - 2027+] PHASE 3: The Infrastructure Wall & Physical Realism |

| * Power grids hit capacity limits; utilities require multi-year lead times. |

| * Server rack densities cross 50kW-100kW, forcing a pivot to liquid cooling. |

| * Copper cables fail at 224Gbps; photonics investments surge past $6.5bn. |

| * Macro-climate events (El Niño 2026-27) strain utility baseloads. |

| |

+---------------------------------------------------------------------------------+Phase 1 (2020–2023): The Algorithmic Scaling Era

During this period, the market viewed AI primarily through a software lens. The release of groundbreaking models like GPT-3 and early generative image tools convinced investors that the primary battleground was algorithmic. Companies focused heavily on parameter counts, reinforcement learning from human feedback (RLHF), and software-level optimizations.

Phase 2 (2023–2025): The Silicon Scarcity Era

As enterprises rushed to integrate AI, the bottleneck shifted from software design to chip availability. This era was defined by the scramble for high-end graphics processing units (GPUs). Hyperscalers (Microsoft, Alphabet, Amazon, and Meta) committed tens of billions of dollars in capital expenditures to secure advanced silicon. Hardware bottlenecks during this phase were largely confined to semiconductor fabrication and advanced packaging technologies, such as Chip-on-Wafer-on-Substrate (CoWoS).

Phase 3 (2025–2027 and Beyond): The Physical Infrastructure Era

Today, the industry has entered a third, highly complex phase. Even when chips are readily available, there is often nowhere to plug them in. Data center developers are facing multi-year delays to secure grid connections. At the same time, the extreme thermal output of new chip architectures is rendering existing data center designs obsolete, while internal network cabling is hitting the fundamental physical limits of electromagnetism.

Supporting Data: Quantifying the Constraints

The shift from the virtual to the physical is backed by rigorous data across meteorology, thermodynamics, and optoelectronics.

1. The Grid and Climate Risk: The 2026–2027 El Niño Threat

The expansion of AI data centers is occurring at a time of heightened vulnerability for global energy grids. Decades of underinvestment have left Western grids fragile. This vulnerability is set to collide with severe climate anomalies.

According to the latest reports from the National Oceanic and Atmospheric Administration (NOAA) and its Climate Prediction Center (CPC), an official El Niño watch has been declared, with forecasts indicating a significant strengthening of the phenomenon as the Northern Hemisphere moves toward the winter of 2026–2027.

NOAA CPC ENSO STRENGTH PROBABILITIES (WINTER 2026-2027)

------------------------------------------------------

[====================================] 63% Very Strong El Niño

[==================] 37% Moderate/Weak El NiñoThere is a 63% probability that this El Niño event will enter the "very strong" category between November and January. This would place it among the most powerful climate episodes recorded since the 1950s.

The economic implications are twofold:

- Grid Strain: Extreme winter conditions followed by intense summer heatwaves will drive residential heating and cooling demand to record levels, directly competing with the continuous, non-negotiable baseload power required by AI data centers.

- Agricultural Disruption: Strong El Niño conditions historically bring severe droughts to major agricultural corridors. This uncertainty over crop yields is already driving up demand for soft commodities and agricultural inputs, notably potash-based fertilizers, as producers attempt to buffer yields against climate volatility.

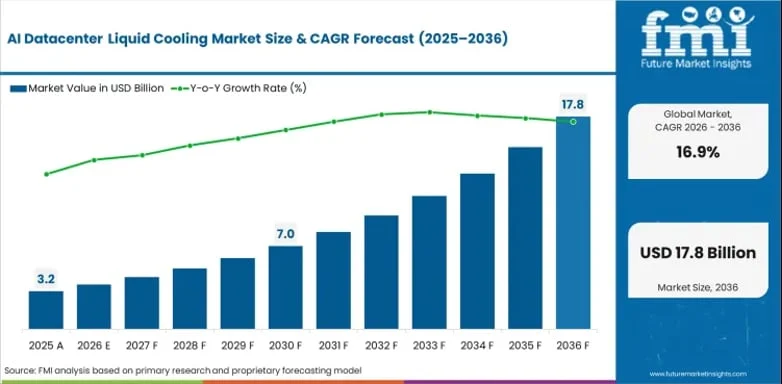

2. The Thermal Bottleneck: The Rise of Liquid Cooling

The thermal output of the latest generation of AI processors has rendered traditional air-cooling systems obsolete. Standard server racks historically operated at densities of 5kW to 15kW. Today, state-of-the-art AI clusters demand densities of 50kW to 100kW per rack.

A single modern AI accelerator chip can consume over 700 to 1,000 watts of power, converting nearly 100% of that electricity into heat. Air simply lacks the heat capacity to dissipate thermal energy at this concentration.

AI DATA CENTER LIQUID COOLING MARKET GROWTH

(Source: Future Market Insights)

$20B |--------------------------------------------------- $17.83B

| /

$15B | /

| /

$10B | /

| /

$5B | $3.20B /

| / /

$0 |--------------------/------------------------/-----

2025 2036

* Projected Compound Annual Growth Rate (CAGR): 16.9%Data from Future Market Insights (FMI) projects that the global liquid-cooling market for AI data centers will undergo a massive structural expansion, growing from $3.2 billion in 2025 to $17.83 billion by 2036, representing a compound annual growth rate (CAGR) of 16.9%.

3. The Death of Copper and the Shift to Photonics

For decades, copper wires have been the circulatory system of digital networks. However, as chip-to-chip communication speeds reach 224 Gbps, copper has reached its physical limits. At these frequencies, copper suffers from extreme high-frequency signal attenuation (loss of signal strength) and electromagnetic interference, meaning it cannot carry data even one single meter without severe degradation.

COPPER VS. SILICON PHOTONICS AT 224 GBPS

----------------------------------------

CHARACTERISTIC COPPER CABLES SILICON PHOTONICS

---------------------------------------------------------------------

Effective Range < 1 Meter Several Kilometers

Signal Degradation Severe at high speed Negligible

Energy Consumption Baseline (100%) 70% to 90% Less per Bit

Data Throughput Speed Baseline (1x) Up to 16x IncreaseTo bypass this barrier, the industry is turning to silicon photonics—using light (lasers) instead of electrons to transmit data. Photonics offers:

- Up to a 16-fold increase in data transmission speeds.

- A 70% to 90% reduction in energy consumption per bit compared to traditional copper interconnects.

- The ability to transmit high-speed data across kilometers rather than centimeters without signal degradation.

Reflecting this critical transition, strategic investments in photonics and optical data transmission by major tech players have surged, exceeding $6.5 billion since March of this year alone.

Official Responses and Industry Perspectives

The realization that physical limits are dictating the pace of digital innovation has prompted a wave of strategic pivots and public acknowledgments from industry leaders and regulatory bodies.

Tech Executives Confront the Energy Crisis

Tech leaders are increasingly open about the energy challenges ahead. In industry forums, executives from Microsoft, Amazon, and Alphabet have noted that securing carbon-free baseload energy is now the primary constraint for data center expansion. This energy crunch has driven hyperscalers to bypass traditional utilities entirely, signing direct Power Purchase Agreements (PPAs) with nuclear power plants and investing directly in next-generation geothermal and small modular reactor (SMR) technologies.

Utility Providers Sound the Alarm

Regulatory and utility bodies are warning that the sheer scale of proposed data centers could destabilize local grids. Representatives from the Federal Energy Regulatory Commission (FERC) in the United States and ENTSO-E in Europe have publicly emphasized that grid interconnection queues are backed up by years. They warn that without massive public-private capital investments to rebuild transmission lines, utilities may have to choose between powering new AI clusters and maintaining reliable service for residential communities during peak climate events.

Semiconductor and Hardware Manufacturers

At recent hardware design conferences, major chip manufacturers have openly declared that the traditional method of improving system performance solely through silicon scaling is coming to an end. Leaders at NVIDIA and its manufacturing partners have stressed that co-packaged optics (CPO) and liquid-cooling integration are no longer secondary engineering considerations; they are now the primary design priorities for next-generation computing platforms.

Implications: The Great Sector Rotation

The return of physical constraints to the technology sector is triggering a major reallocation of capital across global markets. For nearly a decade, investors favored capital-light software companies that boasted high gross margins and low physical footprints. Now, the market is beginning a historic rotation back to capital-intensive, industrial-grade sectors.

THE GREAT AI SECTOR ROTATION

----------------------------

FROM: "Virtual Assets" (SaaS) ===> TO: "Physical Assets" (Industrials)

----------------------------- -----------------------------------

* Software-as-a-Service * Power Generation & Grid Equipment

* Digital-Only Platforms * Advanced Liquid-Cooling Systems

* High-Margin Algorithmic Models * Silicon Photonics & Optical Fiber1. Power Generation and Electrical Grid Equipment

The immediate beneficiaries of this rotation are companies that manufacture heavy electrical infrastructure. Grid developers and equipment manufacturers—such as Eaton and Schneider Electric—are experiencing unprecedented backlogs for transformers, switchgears, and high-voltage transmission lines. Similarly, clean energy producers capable of delivering constant, reliable baseload power are commanding premium valuations.

2. Thermal Management and Liquid-Cooling Providers

As air cooling becomes obsolete, thermal management has transformed from a mundane real estate utility into a highly specialized technology sector. Market leaders in cooling technologies, such as Vertiv and Supermicro, are seeing their thermal divisions revalued as high-growth tech assets. Companies capable of delivering direct-to-chip liquid cooling and two-phase immersion systems have become essential gatekeepers to the deployment of next-generation AI data centers.

3. Photonics and Optical Networking Pioneers

With copper failing to meet the demands of high-speed AI clusters, optical interconnects have become strategic assets. This is reflected in NVIDIA’s recent high-profile investments in photonics innovators like Ayar Labs and Celestial AI. Companies that specialize in silicon photonics, optical transceivers, and laser source technology are poised to capture a significant share of the hardware budget previously reserved for silicon processing units.

4. Macroeconomic and Commodity Impacts

The physical demands of AI are also rippling through global commodity markets. The push for electrical grid expansion is sustaining structural demand for industrial metals, particularly copper for transmission lines and power generators. Simultaneously, the macroeconomic threat of El Niño-induced droughts is driving agricultural hedging, supporting demand for critical crop inputs like potash-based fertilizers.

Conclusion

The artificial intelligence revolution is entering its mature, industrial phase. The narrative of an ephemeral, infinite digital cloud is being replaced by the realities of physical engineering: megawatt capacities, thermal dissipation rates, and optical wavelengths.

While software will continue to evolve, the ultimate speed limits of artificial intelligence will be set by the physical systems supporting it. The long-term winners of the AI era will not be found solely among those who design the most sophisticated models, but among the companies that build, power, cool, and connect the physical infrastructure of the modern world.