For the average American consumer, a trip to the local grocery store to pick up a six-pack is a routine errand. Yet, beneath the price tag lies a labyrinthine regulatory and fiscal framework that varies wildly from state to state, and sometimes from city to city. As we move into 2026, the taxation of beer remains one of the most arcane and misunderstood aspects of American consumer policy. While the average shopper may notice the total price at the register, few realize that a significant—and often invisible—portion of that cost is a mosaic of federal and state excise taxes, licensing fees, and local levies.

The Anatomy of a Beer Tax

To understand the cost of beer in 2026, one must first distinguish between the visible sales tax and the "hidden" excise taxes. Unlike a standard sales tax, which is explicitly added as a separate line item on a receipt, excise taxes are levied at the manufacturer, wholesale, or distributor level. These costs are then "baked into" the final retail price.

The baseline metric often used for comparison is the tax applicable to an off-premises sale of a standard 4.7 percent alcohol-by-volume (ABV) beer in a 12-ounce container. However, this figure is deceptive in its simplicity. In 16 states, the tax rate is not a flat fee; it is a variable calculation dependent on a cocktail of factors, including the alcohol content of the product, the size of the container, the geographic place of production, and even the specific location of the retail purchase.

A Chronology of Regulatory Shifts and State-Level Maneuvering

The landscape of beer taxation has seen significant shifts as states attempt to balance revenue generation with economic development.

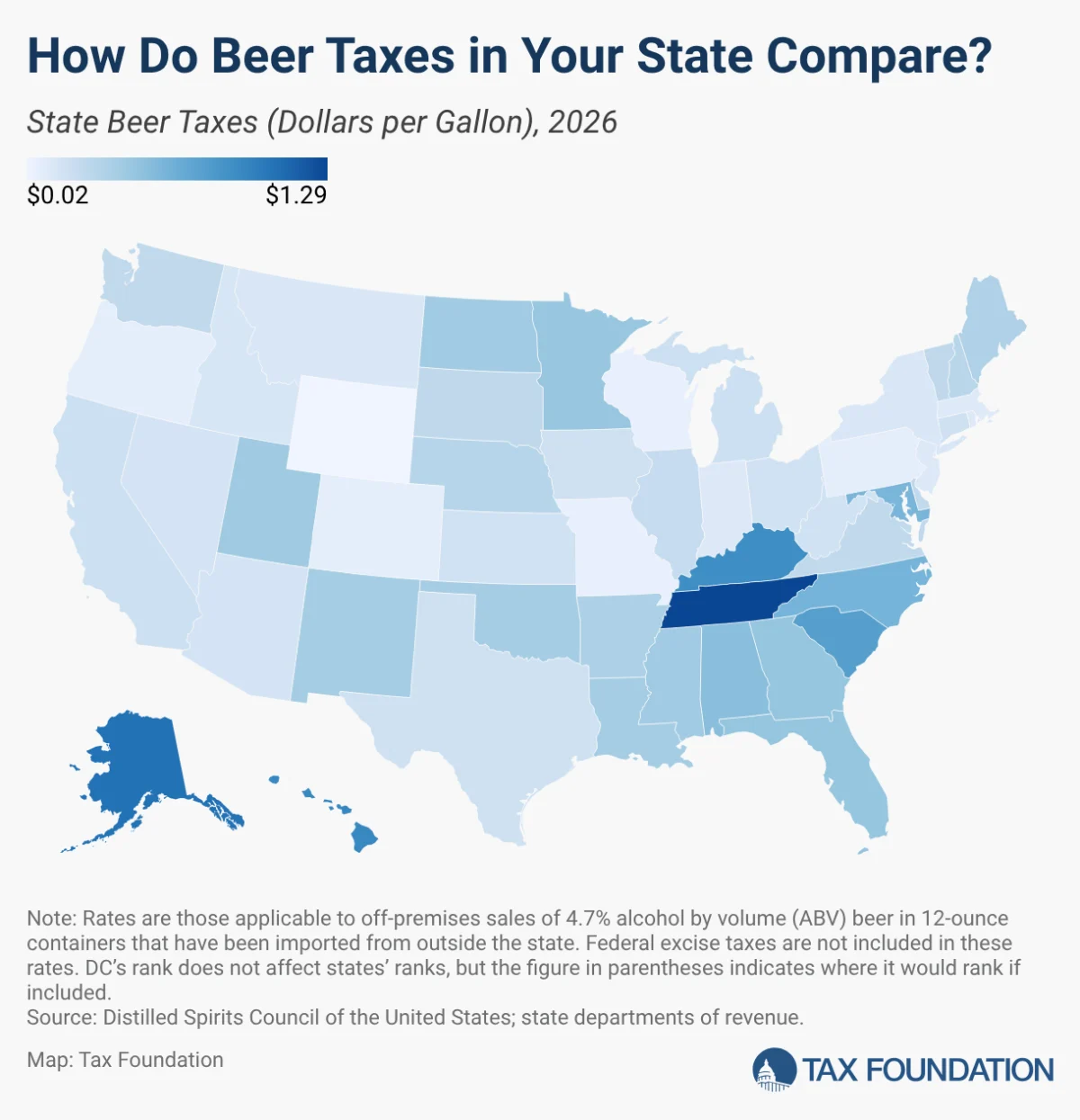

- 2023-2024: The Rise of Micro-Adjustments: States began experimenting with localized tax relief to bolster domestic production. Missouri, for example, successfully passed legislation to slash taxes on beer manufactured within American breweries, bringing the rate down to a mere $0.02 per gallon.

- 2025: Consumer Trend Realignment: The industry faced a "year of reckoning" as tariff-related cost increases collided with a measurable reduction in per-capita alcohol consumption. Younger consumers, in particular, began shifting toward low- or no-alcohol alternatives, forcing states to re-evaluate their reliance on beer excise taxes as a stable revenue stream.

- 2026: The New Normal: As of early 2026, the regulatory environment is characterized by a push for modernization against a backdrop of aging, rigid statutory definitions that struggle to keep pace with product innovation.

Supporting Data: The Disparity in Taxation

The sheer variance in state policy creates a patchwork of costs that defies simple logic. The following examples illustrate the complexity of the current system:

Container and Volume Sensitivity

Virginia serves as a primary example of regulatory complexity. The Commonwealth imposes different tax structures based on the physical size of the container, creating a tiered system for vessels up to 7 ounces, up to 12 ounces, and those exceeding 12 ounces. This requires retailers and distributors to maintain sophisticated inventory management systems to ensure compliance with shifting tax brackets.

The ABV Thresholds

Idaho remains a cautionary tale for those who ignore alcohol content. The state levies triple the standard tax rate if a beer exceeds 5 percent ABV. In this regulatory environment, high-gravity beers are statutorily reclassified—treated effectively as wine—and taxed at $0.45 per gallon rather than the $0.15 rate applied to lower-ABV options.

The Local "Hidden" Levy

Statewide figures often fail to capture the reality of local municipal taxes. The Municipality of Anchorage, for instance, adds an additional 5 percent local sales tax on top of statewide obligations. Similarly, Alabama and Georgia have implemented uniform local taxes that add approximately 50 cents per gallon to the cost of beer, regardless of the specific retail environment.

Official Perspectives: The Case for Modernization

Policy experts and industry advocates argue that the current categorical system—which treats beer, wine, and spirits as distinct, incompatible entities—is fundamentally broken.

"The current framework is an artifact of a bygone era," says a senior policy analyst at a leading tax research institute. "By relying on categories rather than the actual alcohol content of the product, we are creating a system that is not only inefficient but increasingly irrelevant as the beverage industry innovates with new types of hybrid drinks."

The argument for modernization is straightforward: shifting to a system that taxes products based on their actual ABV would ensure neutrality. It would remove the perverse incentives for manufacturers to "game" the system by adjusting recipes to fit into lower tax categories. Furthermore, it would simplify compliance for small-to-medium-sized businesses that currently struggle to navigate the Byzantine regulations of multiple jurisdictions.

The Economic Implications of Fiscal Reliance

For state governments, the reliance on beer taxes is becoming a strategic liability. There are two primary risks identified by fiscal experts:

- Currency Debasement: Many states employ ad quantum taxes (fixed rates per unit). Over time, these taxes lose their real-world value due to inflation and currency debasement. A tax rate that seemed substantial a decade ago now covers a smaller fraction of the government services it was originally intended to fund.

- Behavioral Volatility: States that rely heavily on ad valorem taxes (taxes based on the price of the item) are finding their budgets subject to the whims of consumer trends. As the younger demographic shifts away from alcohol, the revenue from these taxes is becoming increasingly volatile, leading to unforeseen budget gaps.

Future Outlook: The Intersection of Policy and Consumption

As we look deeper into 2026, the beverage industry is at a crossroads. Tariff pressures have increased the cost of raw materials like aluminum and imported hops, while consumer demand is shifting toward premiumization and health-conscious consumption.

Policymakers who continue to view beer as a "cash cow" for general revenue are likely to be disappointed. The structural decline in consumption, coupled with the difficulty of enforcing complex, multi-tiered tax codes, suggests that the current system is unsustainable.

Key Takeaways for the Consumer

- Invisible Costs: Consumers are rarely aware of the excise tax burden because it is embedded in the price, not added at the register.

- Geographic Arbitrage: Where you buy your beer matters significantly. A cross-border trip can result in drastically different tax obligations for the retailer, which is eventually passed down to the consumer.

- The Innovation Gap: Because current laws are rigid, new product categories—such as hard seltzers or functional botanical beverages—often fall into gray areas, leading to inconsistent enforcement and taxation.

Conclusion

The American beer industry is one of the most highly regulated and heavily taxed sectors of the retail economy. As of 2026, the system remains a patchwork of historical compromises and local municipal interests. While the call for a more modernized, ABV-based taxation system is growing louder, the political inertia of state legislatures suggests that change will be incremental.

For the consumer, the takeaway is clear: the price of a pint is more than just a reflection of supply and demand. It is a reflection of a complex, often opaque legislative landscape that is struggling to balance the needs of state budgets with the realities of a modern, changing beverage market. Understanding this framework is not just an academic exercise—it is essential for anyone who wishes to understand the true cost of their favorite beverage in an increasingly complex fiscal environment.