For years, the narrative surrounding silver has been defined by a singular, powerful force: the explosive growth of the solar photovoltaic (PV) industry. As the world pivoted toward renewable energy, silver—a critical component in conductive pastes for solar cells—became the engine of industrial demand. However, a significant shift is currently underway. While the solar sector continues to scale, it is aggressively engineering silver out of its supply chain, leading to a projected decline in silver consumption per panel.

To the casual observer, this may look like a crack in the silver bull case. Yet, a deeper examination reveals that the market is in the midst of a complex structural realignment. Despite a projected 19% drop in solar silver demand for 2026, the global market remains trapped in a persistent supply deficit.

The Macro-Economic Backdrop: Price Volatility vs. Underlying Fundamentals

The silver market has experienced a turbulent 2026. As of mid-June, prices have faced significant pressure, retreating from January highs that surpassed $121 per ounce to settle in the high $60 range. This volatility is a byproduct of a "loud" macro environment. Strong economic data, fluctuating geopolitical tensions—such as the reopening of the Strait of Hormuz—and the Federal Reserve’s hawkish stance on interest rates have all exerted downward pressure on precious metals.

However, beneath the noise of the ticker tape, the demand map for silver is being quietly redrawn. While traders focus on the headlines regarding central bank policy, industrial consumers are focused on the cost of their inputs. With silver prices having surged significantly over the past five years, the metal’s share of a solar cell’s total cost ballooned from 8% to over 20%. This economic imperative has triggered a wave of "thrifting"—the technical process of reducing the silver content per cell without compromising energy conversion efficiency.

Chronology: From Rapid Expansion to Strategic Thrifting

To understand the current tension, one must look at the meteoric rise of solar demand over the last half-decade.

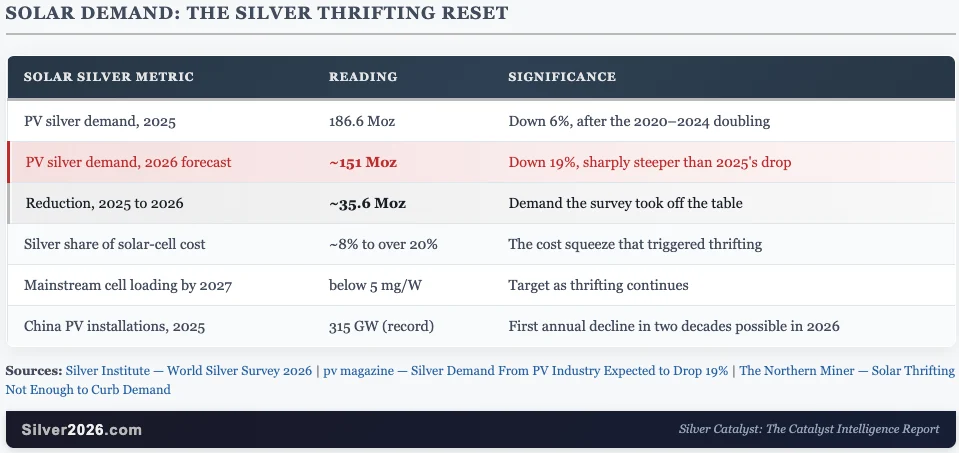

- 2020–2024 (The Expansion Era): Global renewable capacity surged, driving silver use in solar from approximately 82 million ounces to a staggering 197 million ounces. This era established photovoltaics as the single largest industrial consumer of silver, fueling a multi-year market deficit.

- 2025 (The Inflection Point): High silver prices began to bite. Manufacturers, facing compressed margins, accelerated the adoption of ultra-fine printing and zero-busbar designs. Silver use in PV fell by 6%, reaching 186.6 million ounces.

- 2026 (The Efficiency Push): The trend is intensifying. According to the Silver Institute and Metals Focus, solar silver demand is forecast to contract by a further 19%, dropping to roughly 151 million ounces. This decline is driven by both lower silver loadings per cell and a projected cooling of the Chinese solar installation market, which may see its first annual decline in two decades.

Supporting Data: The Physics of Substitution

The solar industry’s move to "thrift" silver is not a sudden pivot but a highly engineered transition. By 2027, the industry expects mainstream solar cells to require less than 5 milligrams of silver per watt.

The Thrifting Toolkit

- Ultra-fine printing: This allows manufacturers to lay down thinner, more precise conductive lines on the silicon wafer.

- Zero-busbar designs: By removing the traditional busbars (the larger conductive strips on a cell), manufacturers can reduce the total volume of silver paste required.

- Advanced Cell Architectures: Technologies like TOPCon (Tunnel Oxide Passivated Contact) have become the industry standard. While these cells are highly efficient, they have forced engineers to refine the chemistry of silver pastes to maximize conductivity with less material.

The Limits of Substitution

Despite the success of thrifting, the "death of silver in solar" remains a premature prediction. The industry is currently hitting a "reliability floor." While research into copper electroplating and pure-copper pastes is ongoing, these alternatives face significant hurdles. Copper is prone to oxidation and reliability issues in high-heat environments—problems that silver, with its superior conductivity and stability, does not face. Consequently, for the high-end, long-lifecycle solar projects that define modern energy infrastructure, silver remains an irreplaceable component.

Official Responses and Industry Outlook

Market analysts at the Silver Institute remain measured in their assessment. The prevailing sentiment is that while the "easy savings" from thrifting are being captured now, the transition to alternative metals is years away from mass-market adoption.

"Solar is not being designed out of existence," noted one analyst from the World Silver Survey. "It is being economized. When a raw material becomes expensive, the industry reacts. That is not a sign of failure; it is a sign of a mature, price-responsive market."

Furthermore, the "energy-security" argument provides a durable floor for demand. Solar deployment is no longer purely a climate policy goal; it is a strategic imperative for nations looking to decouple their power grids from volatile fossil fuel markets. Even with a projected 19% drop in silver-per-panel usage, the sheer volume of global solar build-outs ensures that the industry will remain a dominant, if slightly smaller, consumer of the metal for years to come.

Implications for Investors: The Structural Shortage

For the silver investor, the current environment presents a paradox: demand from the largest growth engine is cooling, yet the total market deficit is widening.

Why the Deficit Persists

According to the 2026 World Silver Survey, even with the projected 36-million-ounce reduction in solar demand, the market is on track for a sixth consecutive annual shortfall of approximately 46.3 million ounces. This reveals a critical truth: the underlying balance of the silver market is far tighter than the solar headlines suggest.

The industrial demand for silver is diversifying. Beyond photovoltaics, silver is essential in the build-out of modernized power grids, the rapid growth of the electric vehicle (EV) sector, and the massive cooling and power requirements of AI-driven data centers. While solar consumption per cell is declining, the total number of industrial applications requiring silver is rising.

The Investment Case

The risk for long-term investors is twofold:

- Technological Acceleration: If copper substitution succeeds faster than anticipated, the demand floor could drop further.

- Macro-Economic Headwinds: If interest rates remain elevated for a prolonged period, the "monetary" demand for silver (as a store of value) may continue to struggle.

However, the offset is equally compelling. The "thrifting" process has physical limits. Once the silver content per cell is optimized to the minimum viable level, the industry cannot reduce usage further without sacrificing performance. When that point is reached, solar silver demand will become tethered once again to the total gigawatt-hours of capacity installed.

Conclusion: A Market Realigned, Not Broken

The news that solar silver demand is falling should not be interpreted as the end of the silver bull case. Rather, it is evidence of a market functioning exactly as it should. High prices triggered innovation, and innovation reduced waste.

The fact that the market remains in a structural deficit despite this massive efficiency gain is the most important data point for long-term investors. It confirms that silver is a scarce resource with inelastic demand across a variety of critical modern industries. While the "solar engine" may be downshifting from its record-breaking pace, the structural shortage of the metal—compounded by years of under-investment in mining and the emergence of new, high-growth industrial sectors—remains the primary driver of the long-term price outlook. Investors who look past the headlines of "solar thrifting" will find a metal that is becoming increasingly essential to a world that, despite its best efforts to economize, simply cannot get enough of it.