The global financial landscape is currently navigating a period of heightened volatility, driven by a convergence of geopolitical instability and persistent macroeconomic uncertainty. At the center of this turbulence is the U.S. 10-Year Treasury yield, a benchmark that serves as the bedrock for global asset pricing. Recent market data indicates that the 10-year yield is trading at a significant premium to its “fair-value” estimate, a divergence that underscores a profound shift in investor sentiment.

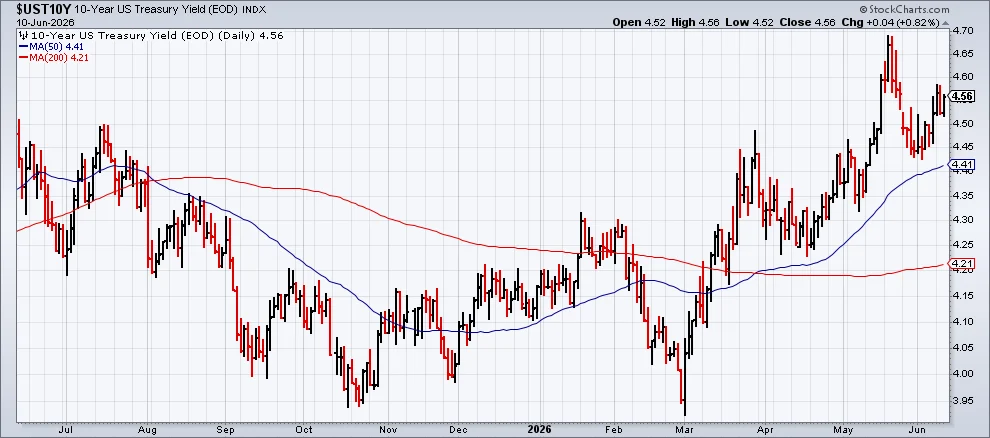

As of June 10, the 10-year yield closed at 4.56%, hovering near a 12-month high. This upward trajectory is not merely a reflection of domestic interest rate policy, but rather a manifestation of an intensifying “risk premium”—the additional yield investors demand to hold government debt in an environment where inflation expectations and geopolitical tensions remain elevated.

Main Facts: The Widening Disconnect

The core of the current market narrative lies in the widening gap between the market-determined yield of the 10-year Treasury note and its theoretical fair-value estimate. According to the ensemble model utilized by The Capital Spectator, the market premium—the spread between the actual yield and the model’s estimate—has ballooned to 48 basis points.

This figure represents the highest premium observed since July 2025. In financial terms, this indicates that the market is currently pricing in a significantly higher risk profile than what is justified by conventional macroeconomic fundamentals alone. Investors are effectively demanding more compensation for the uncertainty surrounding future inflation trajectories and the potential for spillover effects from the ongoing conflict in the Middle East.

Chronology of the Shift: From Normalization to Reversal

To understand the significance of this move, one must examine the timeline of Treasury yields over the past few years.

The Pandemic Surge and Subsequent Normalization

During the height of the COVID-19 pandemic, Treasury yields experienced a violent decoupling from historical norms. Supply chain disruptions, unprecedented fiscal stimulus, and an abrupt spike in inflation pushed yields higher, creating a massive risk premium. However, as the global economy began to stabilize and central banks signaled a pivot toward tightening monetary policy, the market entered a "normalization phase." Throughout this period, the risk premium began to contract, suggesting that the market was successfully pricing in a return to a more predictable economic environment.

The Geopolitical Inflection Point

The trajectory of this normalization was abruptly halted by the outbreak of conflict in the Middle East. The initial market reaction was characterized by a "flight to safety," which often suppresses yields. However, as the conflict persisted and the potential for long-term regional instability grew, the focus shifted toward the inflationary implications of energy supply disruptions and supply chain bottlenecks.

By early May, the data began to clearly reflect this reversal. The steady decline in the risk premium that had characterized the post-pandemic recovery period gave way to a new upward trend, marking a decisive shift in market psychology.

Supporting Data and Quantitative Analysis

The ensemble model employed by The Capital Spectator synthesizes multiple fair-value estimates to provide a smoothed outlook on where Treasury yields "should" be, based on historical correlations with inflation, economic growth, and monetary policy stances.

Analyzing the Spread

The spread—calculated as the current 10-year yield minus the fair-value estimate—serves as the primary indicator of investor anxiety. For several quarters, this spread had been trending downward, reflecting a market that was increasingly confident in the Federal Reserve’s ability to anchor inflation expectations.

The reversal seen in May and June is statistically significant. When the 10-year yield trades 48 basis points above its model-driven fair value, it suggests that the market is pricing in "tail risk." This risk is not necessarily captured in standard economic models; it includes the risk of "higher-for-longer" interest rates, the fiscal implications of a ballooning U.S. national debt, and the geopolitical premium associated with the Iran-led conflict.

Yield Trends

The climb to 4.56% on June 10 is not an isolated event but part of a sustained push against the upper bounds of the recent range. Technical analysts point to this level as a critical threshold. Should the yield break through this resistance, it could trigger a further repricing of risk assets across the board, from corporate credit to equity valuations, which are historically sensitive to the "risk-free" rate benchmark.

Official Responses and Macroeconomic Context

While the Federal Reserve has maintained a stance of data dependency, market participants are increasingly skeptical that current models capture the full extent of the risks involved.

The Federal Reserve’s Dilemma

Federal Reserve officials have consistently highlighted that their primary mandate is the restoration of price stability. However, the persistence of the 10-year yield premium suggests that the bond market is "fighting" the Fed. If the market demands a higher premium for Treasury debt, the effective cost of borrowing for the U.S. government increases, complicating fiscal policy.

Furthermore, the "inflation risk" mentioned by market analysts is often linked to the potential for energy price volatility caused by the Iran conflict. While the Fed cannot influence geopolitical outcomes, the consequences of those outcomes—such as higher oil prices—force the central bank to maintain higher interest rates for longer than previously anticipated.

Global Central Banking Perspectives

International central banks are watching the U.S. Treasury market with trepidation. As the U.S. 10-year yield rises, it exerts upward pressure on sovereign bond yields globally. This creates a "tightening effect" in other jurisdictions, even if those nations face domestic economic slowdowns. The rise in the U.S. risk premium, therefore, acts as a global economic headwind.

Implications: What This Means for Investors

The widening of the risk premium has profound implications for every asset class.

1. The Equity Risk Premium

As the risk-free rate (the 10-year yield) climbs, the hurdle rate for corporate investment rises. Equity markets, particularly high-growth technology stocks, are vulnerable to this shift. When the risk-free rate is high, the present value of future earnings is discounted more aggressively, leading to lower valuation multiples.

2. Credit Markets

Corporate bond spreads, which represent the additional yield investors require to hold company debt over Treasuries, are also feeling the heat. If the "base rate" (the Treasury yield) continues to climb due to an elevated risk premium, corporations with high debt loads may find refinancing significantly more expensive, potentially leading to a spike in credit defaults.

3. The Geopolitical "Fear Factor"

The most significant takeaway is that the market is no longer treating the geopolitical conflict in the Middle East as a temporary disruption. By baking in a 48-basis-point premium, investors are signaling that they expect the inflationary pressures linked to this conflict to persist for the foreseeable future. This is a departure from the "transitory" narrative that governed market thinking in the early stages of the conflict.

4. Long-term Asset Allocation

For institutional investors, the current environment necessitates a re-evaluation of the "60/40" portfolio. If Treasury bonds no longer provide the expected protection during equity market drawdowns—because the bond market itself is suffering from a rising risk premium—investors may need to look toward alternative hedges, such as commodities or inflation-protected securities (TIPS).

Conclusion: A Market in Search of Equilibrium

The recent evolution of the 10-year Treasury yield is a clear signal that the financial world is entering a new phase of risk assessment. The normalization process that defined the post-pandemic era has been decisively interrupted.

The convergence of the Iran conflict and persistent inflation concerns has created a structural shift in how investors view the safety and value of U.S. government debt. With the 10-year yield trading near its 12-month high and the risk premium at its widest point in nearly a year, the message from the bond market is unambiguous: uncertainty is the new baseline.

As we look toward the remainder of the year, the stability of this premium will depend on two critical factors: the containment of geopolitical escalation and the trajectory of domestic inflation data. If the premium continues to widen, it will force a repricing of risk across all asset classes, signaling that the "fair value" of the global economy is in a state of flux. Investors, therefore, should remain cautious, as the current yield environment reflects not just the math of interest rates, but the raw, unpredictable reality of global risk.