In the modern landscape of personal finance, most individuals find themselves trapped in a cycle of "micro-monitoring." They obsess over the daily fluctuations of their checking account, suffer anxiety over the rising cost of a monthly grocery bill, and panic when an unexpected car repair temporarily dips their liquid cash. However, according to financial experts, these daily observations are effectively "noise." They represent snapshots of a single moment in time, offering no meaningful insight into whether an individual is actually building long-term wealth or merely treading water.

The most accurate, comprehensive metric for financial health is not your salary, your savings rate, or your monthly discretionary spend—it is your net worth. By shifting the focus from volatile monthly cash flow to the steady, long-term trajectory of net worth, individuals can finally gain a clear, objective view of their financial life.

The Core Concept: What Is Net Worth?

At its simplest, net worth is a mathematical equation: Assets minus Liabilities.

Assets include everything you own that holds value—your savings accounts, retirement funds (401(k), IRA), brokerage accounts, real estate, and tangible property. Liabilities encompass everything you owe—credit card debt, student loans, car notes, and your mortgage balance.

While the concept is elementary, the implications are profound. When you pay off $500 of credit card debt, it often feels like a loss because your checking account balance drops. In reality, you have improved your net worth by $500, because your liabilities have decreased by that exact amount. By tracking net worth, you stop viewing your finances through the narrow lens of liquidity and start viewing them through the lens of total economic power.

Chronology of Financial Monitoring: Moving from Daily Noise to Quarterly Strategy

To understand why a quarterly review is the "gold standard" of financial health, we must look at the natural evolution of how people track their money.

The Era of Daily Anxiety

For many, financial tracking begins with logging into a banking app daily. While this promotes "awareness," it often leads to cognitive fatigue. Because checking accounts are subject to the "lumpiness" of life—rent payments, pay cycles, and unexpected bills—the data is inherently chaotic. A monthly drop in a checking account does not mean you are becoming poorer; it simply means you are paying your bills.

The Era of Yearly Reflection

Conversely, many people wait until tax season or the end of the year to conduct a "financial audit." While this provides a high-level view, it is often too late to course-correct. If you discover in December that your spending has outpaced your savings for the last 11 months, you have lost a year of potential compounding growth and debt reduction.

The Modern Quarterly Standard

The "Goldilocks" approach—the quarterly review—strikes the perfect balance. Checking your net worth every three months serves three critical functions:

- Smoothing the Noise: A single bad month (due to a market correction or a large one-time expense) is buffered by the other two months in the quarter.

- Actionable Rhythm: It is frequent enough that you can detect a trend before it becomes a crisis, but infrequent enough that it doesn’t consume your mental bandwidth.

- Psychological Stability: By focusing on the long-term trend line, you can detach your emotions from the inevitable volatility of the stock market and your own short-term spending habits.

Supporting Data: The Power of Aggregation

The primary barrier to tracking net worth has historically been the administrative burden. Manually calculating assets and liabilities in a spreadsheet is tedious, prone to error, and quickly becomes outdated.

However, the rise of digital personal finance dashboards has revolutionized this process. Platforms such as Empower and Monarch Money act as "financial aggregators." By securely linking to your various institutions—banks, credit card issuers, mortgage lenders, and investment brokerages—these tools pull real-time data to provide a live, automated net worth calculation.

Why Automation Wins

- Completeness: Manual tracking often misses "hidden" liabilities like accrued interest or small recurring debts. Automated tools capture everything.

- Market Integration: These tools automatically update the value of your brokerage accounts and, in many cases, can pull estimated market values for real estate via Zillow or similar APIs.

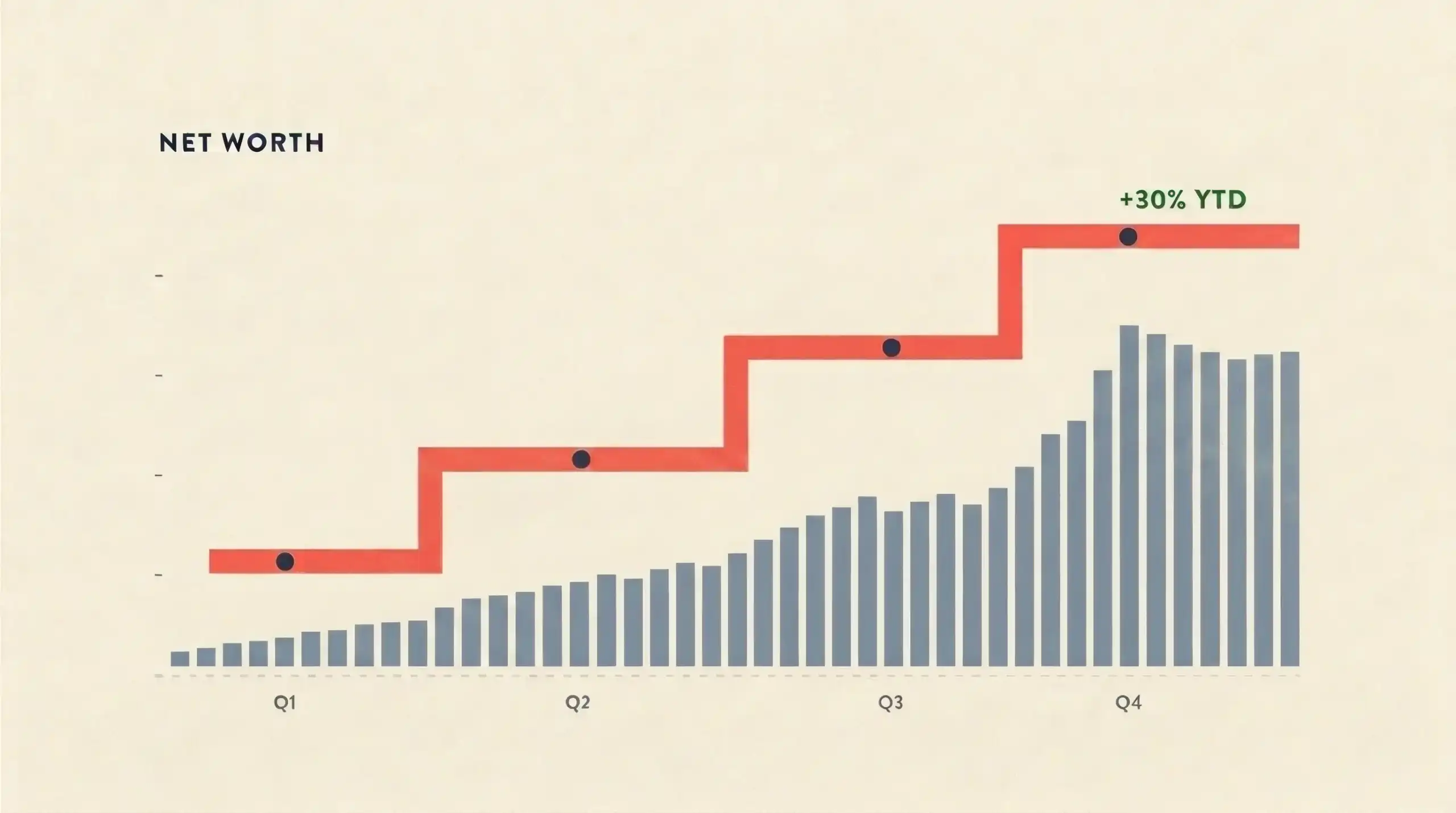

- Trend Visualization: Most modern platforms offer intuitive charts that display your net worth trajectory over years. Seeing a line move upward over a three-year period is a powerful psychological reinforcement that encourages continued saving and investing.

Official Perspectives: The Experts Weigh In

Financial advisors and wealth managers almost universally agree that the "Net Worth First" approach is the most effective way to coach clients.

"Most people focus on the wrong numbers," says a lead analyst at a prominent financial research firm. "They ask, ‘How much can I spend this month?’ instead of ‘How much am I worth today?’ If you focus on the former, you’re always living on the edge of your paycheck. If you focus on the latter, you are constantly incentivized to increase the spread between what you earn and what you owe."

The consensus is that while income is important, it is merely the "fuel." Net worth is the "engine." You can have a high income and a declining net worth if your liabilities (spending) are growing faster than your assets. Conversely, a moderate income can lead to a skyrocketing net worth if the individual is disciplined about their liabilities.

Implications: Building a Sustainable Financial Future

What happens when you adopt the quarterly net worth check-in? The implications for your financial life are transformative.

1. Identifying "Money Leaks"

If your net worth remains flat for two consecutive quarters despite a steady income, it is a definitive sign that you have a "leak." Your money is going somewhere—perhaps into high-interest debt, excessive lifestyle inflation, or underperforming investments. Because you are looking at the aggregate number, you cannot hide from the reality of your progress.

2. Moving from Precision to Direction

There is a common trap in personal finance called "analysis paralysis." Some people spend hours auditing every coffee purchase. This is a losing strategy. The "direction" of your wealth is far more important than the "precision" of your budget. If your net worth is trending upward, you are doing the right things. You don’t need to account for every cent; you need to ensure the total is growing.

3. Creating a Feedback Loop

Financial success is often delayed gratification. By checking your net worth quarterly, you create a feedback loop that rewards your hard work. Seeing that number rise after a quarter of paying down student loans provides the dopamine hit necessary to continue the behavior for the next three months.

4. Market Resilience

When the stock market dips, many investors panic and sell. However, when you view your net worth as a whole, a market dip is just one factor in a larger picture. It keeps you from making emotional decisions during periods of volatility because you can see that your debt reduction and savings rate are still doing the heavy lifting, even when the market is red.

Conclusion: The Two-Minute Habit

The setup process for this financial transformation takes approximately 20 minutes. Select a dashboard, link your accounts, and define your starting point. After that, the maintenance is remarkably simple: set a recurring calendar reminder for the first weekend of every January, April, July, and October.

Spend two minutes reviewing the trend line. Ask yourself: Is the line moving in the right direction? If yes, keep going. If no, investigate the leaks.

In a world where financial products are designed to make you spend, having a personal "North Star" is the only way to ensure you are building security for yourself and your family. Forget the daily checking account balance. Stop worrying about the individual monthly bills. Focus on the only number that dictates your future: your net worth.

Editorial & Advertiser Disclosure: The editorial content on this website is not provided, commissioned, reviewed, approved, or otherwise endorsed by any advertiser. Opinions expressed are ours alone, not those of any advertiser. The offers that appear are from companies from which we may receive compensation. However, this compensation does not impact where and how these companies are mentioned on the site. We do not include all companies or all available offers in the marketplace.