In the modern financial landscape, the difference between building lasting wealth and living paycheck-to-paycheck often comes down to a single, overlooked factor: the sequence of your financial decisions. Many individuals approach their personal finances with a haphazard "shotgun" strategy—investing small amounts here, paying off a credit card there, and saving whatever happens to remain at the end of the month.

However, financial experts argue that true wealth accumulation is not just about how much you earn, but how strategically you deploy every dollar. By following a rigid, prioritized "Order of Operations," you can ensure that your capital is always working at maximum efficiency.

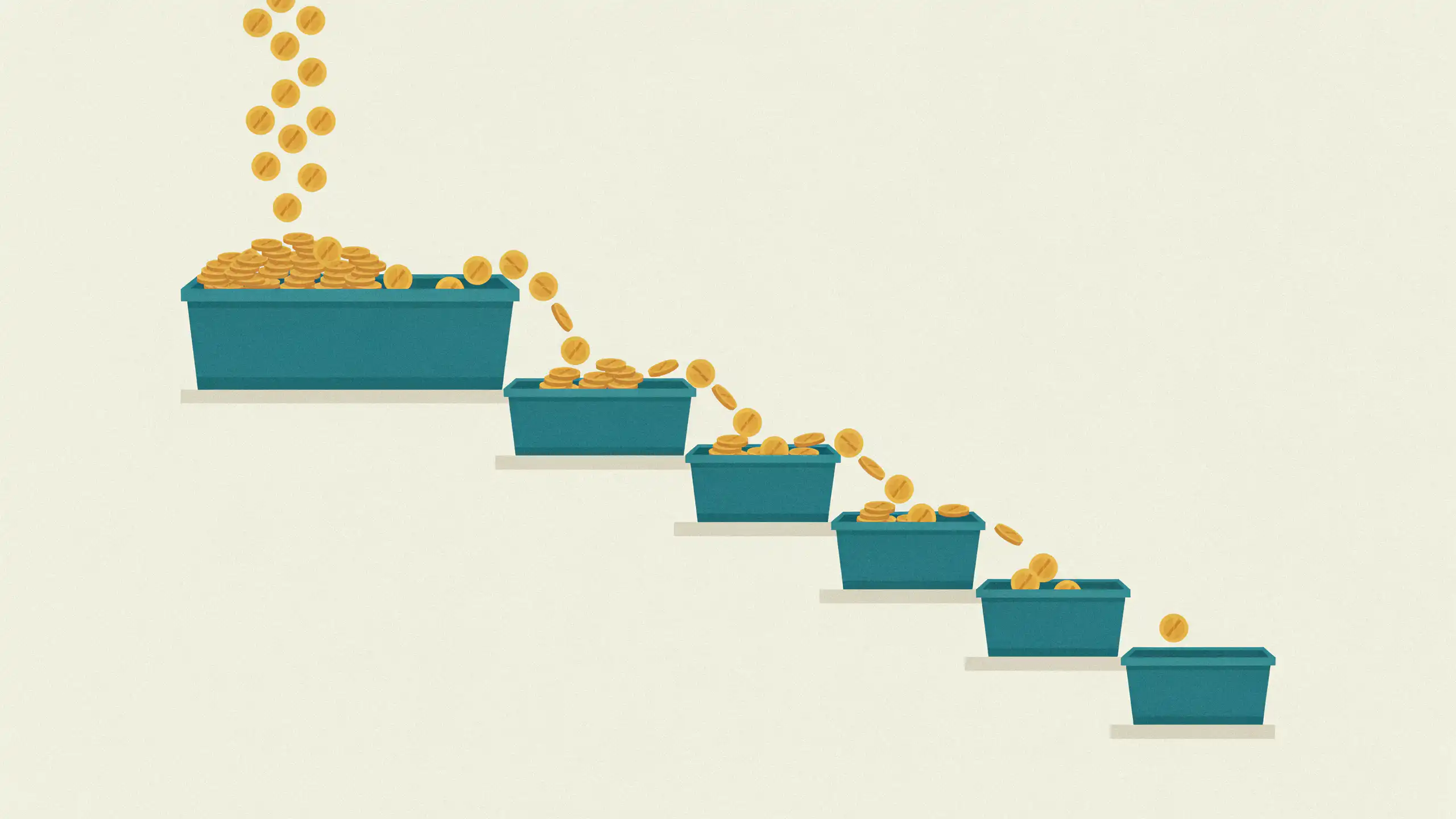

The Financial Hierarchy: Establishing the Priority Framework

The concept of a "financial sequence" suggests that not all dollars are created equal. A dollar used to pay off a 22% APR credit card balance is fundamentally more powerful than a dollar placed in a high-yield savings account earning 4%. When you ignore this hierarchy, you effectively "leak" wealth through interest payments and missed opportunities.

The golden rule of personal finance is simple: Sequence matters more than scale. Two individuals earning identical salaries can diverge by hundreds of thousands of dollars in net worth over a decade, simply because one followed a deliberate path while the other acted on impulse.

The Six-Step Roadmap to Fiscal Optimization

- The Starter Emergency Buffer: A small, accessible cash reserve designed to prevent you from using credit cards when minor life emergencies arise.

- The Employer 401(k) Match: Capturing the "free money" offered by your employer, which provides an immediate, risk-free return on investment.

- High-Interest Debt Elimination: Eradicating debts that carry interest rates higher than what you could reasonably expect to earn in the stock market.

- The Full Emergency Fund: Transitioning from a "buffer" to a 3-to-6-month cushion, providing a robust safety net against major life disruptions.

- Tax-Advantaged Retirement Accounts (IRA): Utilizing individual retirement accounts to maximize tax-deferred or tax-free growth.

- General Investing: Allocating surplus funds into brokerage accounts, real estate, or other wealth-building vehicles.

Chronology of Wealth: Why the Sequence Cannot Be Bypassed

Financial experts often compare this sequence to building a house. You cannot build the roof (general investing) before you have poured the foundation (emergency funds) or installed the framing (employer matches). If you attempt to skip steps, you introduce structural risks that can bring your entire financial plan crashing down during an economic downturn.

Step 1: The Starter Buffer

The journey begins not with growth, but with defense. Without a "starter" buffer—typically $1,000 to $2,000—any unforeseen expense, such as a car repair or a minor medical bill, forces you to reach for a credit card. Once you rely on high-interest debt to bridge these gaps, you are immediately forced to pay a "poverty tax" in the form of 20% to 30% interest rates.

Step 2: Capturing the Employer Match

Once the buffer is established, the focus shifts to the most lucrative move in personal finance: the employer 401(k) match. If your company offers a 100% match on contributions up to 5% of your salary, you are effectively securing an immediate 100% return on your money. No investment vehicle in the history of the stock market consistently generates a 100% return in a single day. Skipping this is akin to turning down a pay raise.

Step 3: Eliminating High-Interest Debt

Credit card debt acts as a reverse investment. If you are paying 22% interest on a balance, you are effectively losing 22% of your net worth annually to the lender. Because the long-term historical average of the S&P 500 is roughly 8% to 10% per year, it is mathematically irrational to invest in the market while holding high-interest debt. You should prioritize paying off these balances over almost any other financial goal.

Step 4: The Full Emergency Fund

Once high-interest debt is cleared, you move to the full emergency fund. This isn’t just about savings; it is about "optionality." With six months of expenses in a liquid account, you gain the freedom to change jobs, handle a period of unemployment, or pivot during a recession without liquidating your long-term investments.

Supporting Data: The Math of Efficiency

To understand the urgency of this sequence, one must look at the "cost of delay." If an individual has $5,000 in surplus cash, they face a choice: pay off a 20% credit card or invest in a brokerage account.

If they choose the credit card, they save $1,000 in interest over the year. If they invest that $5,000 in the stock market with an 8% return, they earn $400. By choosing the wrong sequence, the individual has effectively lost $600. When multiplied over years and compounded, these "lost opportunities" account for the massive disparity in wealth between different demographics.

Financial advisors emphasize that this is not a one-time process. It is a recurring cycle. Whenever a bonus, tax refund, or raise occurs, the "Order of Operations" provides an objective, emotion-free destination for those funds. By removing the need for deliberation, you remove the temptation to spend the money on lifestyle inflation.

Professional Perspectives and Industry Standards

Financial professionals consistently advocate for this structured approach because it addresses both behavioral and mathematical realities.

"The biggest mistake we see is ‘optimism bias,’" says one financial planner. "People assume they won’t have a car repair or a medical emergency, so they jump straight to investing. Then, when the emergency happens, they liquidate their investments during a market dip, triggering taxes and penalties. The sequence is designed to protect you from your own optimism."

Critics of rigid sequences sometimes argue that "debt is just a tool," but for the vast majority of households, the risk-adjusted return of paying off high-interest debt is superior to any volatile market asset. The consensus among wealth managers is that until your balance sheet is stabilized, leverage should be minimized, not maximized.

Implications for Future Financial Security

The implications of adopting this hierarchy are profound. By automating your financial decisions according to these priorities, you create a "self-healing" financial system.

- Reduced Cognitive Load: You no longer need to decide what to do with a $500 bonus; the system dictates that it goes to the next incomplete step in your sequence.

- Accelerated Net Worth: By avoiding high-interest debt and maximizing employer matches, you are essentially increasing your "savings rate" without necessarily earning more income.

- Crisis Resilience: When the economy experiences a contraction, those who followed the sequence—holding a full emergency fund and zero high-interest debt—are the most resilient. They are not forced to sell assets at a loss.

Navigating the Nuances

It is important to note that these steps are not strictly linear in a way that prevents overlap. For instance, most people will contribute to their 401(k) via payroll deduction while simultaneously paying down a credit card balance. The "priority" aspect of the sequence simply dictates where excess or discretionary funds should be directed.

The goal is to stop treating money as a pile of cash to be used for the next shiny object and start treating it as a resource to be deployed into the highest-yielding bucket available.

Final Summary: The Discipline of Execution

The path to financial independence is rarely paved with complex, high-risk investment strategies. Instead, it is paved with the boring, consistent, and disciplined execution of a foundational plan. By prioritizing your liquidity, capturing free money, and systematically eliminating high-interest liabilities, you shift from a reactive financial state to a proactive one.

As you look toward the next year, take a moment to audit your current position. Are you skipping steps? Are you funding a brokerage account while carrying a balance? If so, the solution is simple: pause, re-evaluate, and align your next dollar with the hierarchy of wealth. Your future net worth depends not on the next "hot" stock tip, but on the order in which you choose to pay your past, your present, and your future self.