In a fundamental shift that is reshaping the landscape of global finance, new Federal Reserve Chair Kevin Warsh is signaling a departure from the "Fed-first" guidance model that defined the previous decade. Under Warsh’s stewardship, the central bank appears to be moving toward a strategy of decentralization, effectively delegating the heavy lifting of interest rate discovery to the bond market.

This transition is not merely theoretical. As inflation remains stubbornly elevated, investors are responding with a decisive repricing of real (inflation-adjusted) yields. The recent surge in Treasury Inflation-Protected Securities (TIPS) serves as the primary battleground for this new paradigm, with real yields breaking through psychological thresholds that haven’t been tested in over a year.

The Mechanics of the Shift: Letting the Market Lead

For years, the Federal Reserve acted as the "market-maker of last resort," utilizing forward guidance to minimize volatility and steer investor expectations. Chair Warsh, however, has signaled a preference for a more hands-off approach, emphasizing that the central bank should function as a reactive body rather than an architect of market sentiment.

In his inaugural press conference, Warsh articulated a vision where the bond market acts as the primary transmission mechanism for monetary policy. "I think financial markets perform best when they react to incoming data," Warsh remarked. By encouraging the market to process real-time economic signals—such as employment reports, consumer price indices, and geopolitical energy shocks—the Fed aims to foster a more resilient financial system.

This strategy places the burden of proof on the "bond ghouls"—the collective of traders, hedge funds, and institutional investors who must now interpret the Fed’s intent through the prism of economic reality rather than waiting for explicit, pre-scripted guidance.

Chronology of the Yield Surge

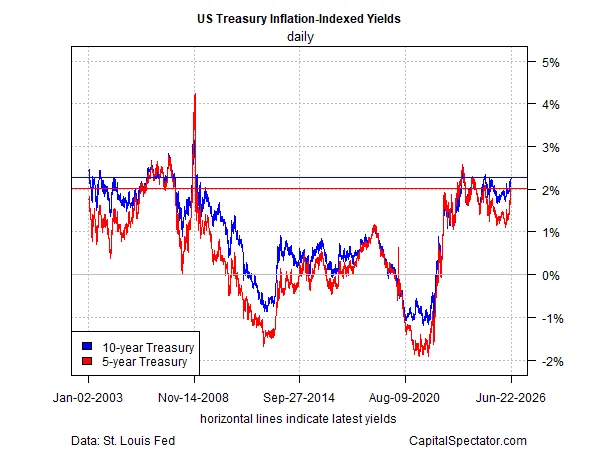

The recent trajectory of TIPS yields offers a clear timeline of this market recalibration. As recently as February 27, the 5-year real yield sat at a modest 1.11%. The subsequent months have been defined by a rapid, volatility-driven ascent.

- Q1 2026: Markets began pricing in higher geopolitical risk premiums as tensions between the United States and Iran intensified, threatening global energy supply chains.

- Late Q2 2026: The persistence of headline inflation, driven primarily by energy costs, forced a re-evaluation of long-term real interest rates.

- June 17, 2026: Chair Warsh’s first press conference solidified the hawkish tone, acknowledging that the Fed had failed to hit its 2% inflation mandate for over five years.

- Current Standing: Yesterday’s market close marked a significant milestone: the 5-year TIPS rate climbed to 2.01%, crossing the 2.0% threshold for the first time in over a year.

This upward pressure has cascaded across the yield curve. The 10-year TIPS now trades at 2.13%, while the 30-year maturity has hit 2.75%, reflecting a market that is increasingly demanding higher compensation for the risk of sustained inflationary pressure.

Supporting Data: Dissecting the TIPS Landscape

The data suggests that the market is not just reacting to inflation, but also to a fundamental change in the cost of capital. The rise in real yields is a direct reflection of the market’s belief that tighter policy is not only necessary but inevitable.

Yield Maturity Breakdown

- 5-Year TIPS (2.01%): Represents the short-to-medium-term expectations of policy path and inflation control. Its breach of the 2% level is a strong signal that investors no longer view the current rate environment as "accommodative."

- 10-Year TIPS (2.13%): Serves as the benchmark for long-term real growth and inflation expectations. The narrowing gap between the 5-year and 10-year yields indicates a flattening curve, often a precursor to restricted liquidity.

- 30-Year TIPS (2.75%): Captures the "term premium"—the extra yield required for holding long-term debt in an uncertain inflationary environment.

The rapid move from 1.11% in February to over 2% today demonstrates a massive rotation in capital. Investors who were previously parked in cash or equity risk-on assets are finding the "risk-free" real return of TIPS increasingly attractive, creating a self-reinforcing cycle of higher yields.

Official Responses and the "Hawkish" Pivot

Chair Warsh’s rhetoric has been scrutinized by analysts for its stark departure from his predecessors. During his June 17 briefing, he didn’t mince words: "Inflation has been running well ahead of the Fed’s long-stated goal of 2%—that’s been going on for more than five years. Persistently high prices are a burden for the American people."

This admission represents a significant shift in Fed accountability. By framing inflation as a "burden" rather than a transitory phenomenon, Warsh is signaling a potential return to traditional monetary conservatism. His philosophy, as explained to reporters, is that "the more that markets are paying attention to what’s happening in the real economy—deciding what’s good data and what’s less good data—the more financial markets can price what they believe is the most likely and what the tail risks are."

Implications: A New Era for Investors

The implications for the broader economy are profound. If the Fed continues to outsource rate-setting to the market, investors should expect:

- Increased Volatility: Without the "Fed Put" to act as a floor for markets, investors will be forced to respond more aggressively to economic data prints.

- Higher Cost of Capital: Businesses will need to adjust to a world where real rates are not suppressed by central bank intervention. This may dampen corporate investment and force a return to fundamental earnings-based valuations.

- The "Endgame" Uncertainty: The current inflationary spike is heavily influenced by the war with Iran. As Vice President Vance reports "great progress" in diplomatic negotiations and energy prices begin to retreat, the primary catalyst for the current rise in yields may be waning.

The central question remains: If energy prices collapse and headline inflation cools, will the market-driven yields follow suit, or have we entered a structural shift where the market demands a higher "real" return regardless of temporary inflationary spikes?

Conclusion: The Bond Market’s Test

The Federal Reserve is currently engaged in a high-stakes experiment. By relinquishing the steering wheel to the bond market, Kevin Warsh is betting that the collective wisdom of thousands of global participants will lead to a more stable economy than the discretionary decisions of a single committee.

For now, the market is playing its part. It is pricing in a tougher, higher-for-longer environment, effectively doing the Fed’s job by tightening financial conditions without the need for a formal hike at every meeting. However, the path forward is fraught with uncertainty. As geopolitical tensions subside and the "war-driven" inflation fades, the bond market will face its true test: distinguishing between a temporary anomaly and a permanent shift in the economic landscape.

For the average investor, the message is clear: the era of easy money is receding, and the era of market-led reality has arrived. Whether this leads to a soft landing or a period of prolonged volatility remains the primary concern for the fiscal and monetary authorities alike. For now, the 2% yield on the 5-year TIPS stands as the new North Star in a shifting financial galaxy.