Whether you are a seasoned sommelier curating a private cellar or a casual consumer picking up a bottle for dinner, there is a silent partner at your table: the government. While the price on the shelf is what most shoppers focus on, the true cost of that bottle of wine is heavily influenced by a labyrinthine system of state and federal excise taxes, markups, and regulatory fees. As we move through 2025, the total economic burden of these consumption taxes is estimated to reach a staggering $7.2 billion, highlighting a tax structure that is as antiquated as it is costly.

The State of Play: Understanding the Burden

Wine has maintained a remarkably steady market share among alcoholic beverages since the turn of the millennium. Despite shifting consumer preferences toward craft spirits and ready-to-drink (RTD) cocktails, wine remains a cornerstone of the hospitality industry and a significant contributor to the broader economy. However, beyond the standard sales and corporate income taxes paid by businesses, the industry faces specific "sin taxes"—excise levies that are often misunderstood by the public and applied inconsistently by state legislatures.

Currently, the average wine drinker may not realize that their purchase is being taxed based on a patchwork of legacy policies. States generally categorize alcohol into three tiers: beer, wine, and distilled spirits. Typically, wine is taxed at a rate higher than beer but lower than spirits, reflecting its mid-range alcohol-by-volume (ABV) content. However, this logic frequently breaks down upon closer inspection. After adjusting for actual alcohol content, many states still levy a disproportionately higher tax on wine, while others skew the playing field by taxing beer at double the rate of wine. This "arcane categorical system," as described by tax policy experts, creates an environment of economic distortion that complicates supply chains and confuses consumer pricing.

A Chronology of Categorical Inefficiency

The history of alcohol taxation in the United States is rooted in post-Prohibition regulation, which sought to control distribution through a "three-tier system" (producers, distributors, and retailers). Over the last several decades, these systems have evolved into a complex, state-by-state regulatory nightmare.

Since 2021, the landscape has seen increased pressure as states look for ways to bolster general revenues. However, unlike broad-based income or sales taxes, excise taxes are notoriously inefficient. Because they are often "ad quantum" (volume-based, such as a fixed dollar amount per gallon), they lose their real-world value over time due to inflation—a phenomenon known as currency debasement. Conversely, when states move toward "ad valorem" (value-based) taxes, revenues become highly volatile, fluctuating wildly based on consumer behavior, market trends, and the impact of international trade tariffs on imported wines.

In recent years, the rapid rise of RTD wine-based cocktails has exposed the fragility of these old laws. Because many statutes define wine by strict, narrow parameters, these innovative products often fall into a "regulatory gap," leading to situations where new, popular beverages are either over-taxed or barred from entry due to outdated definitions.

The Geography of Taxation: Winners and Losers

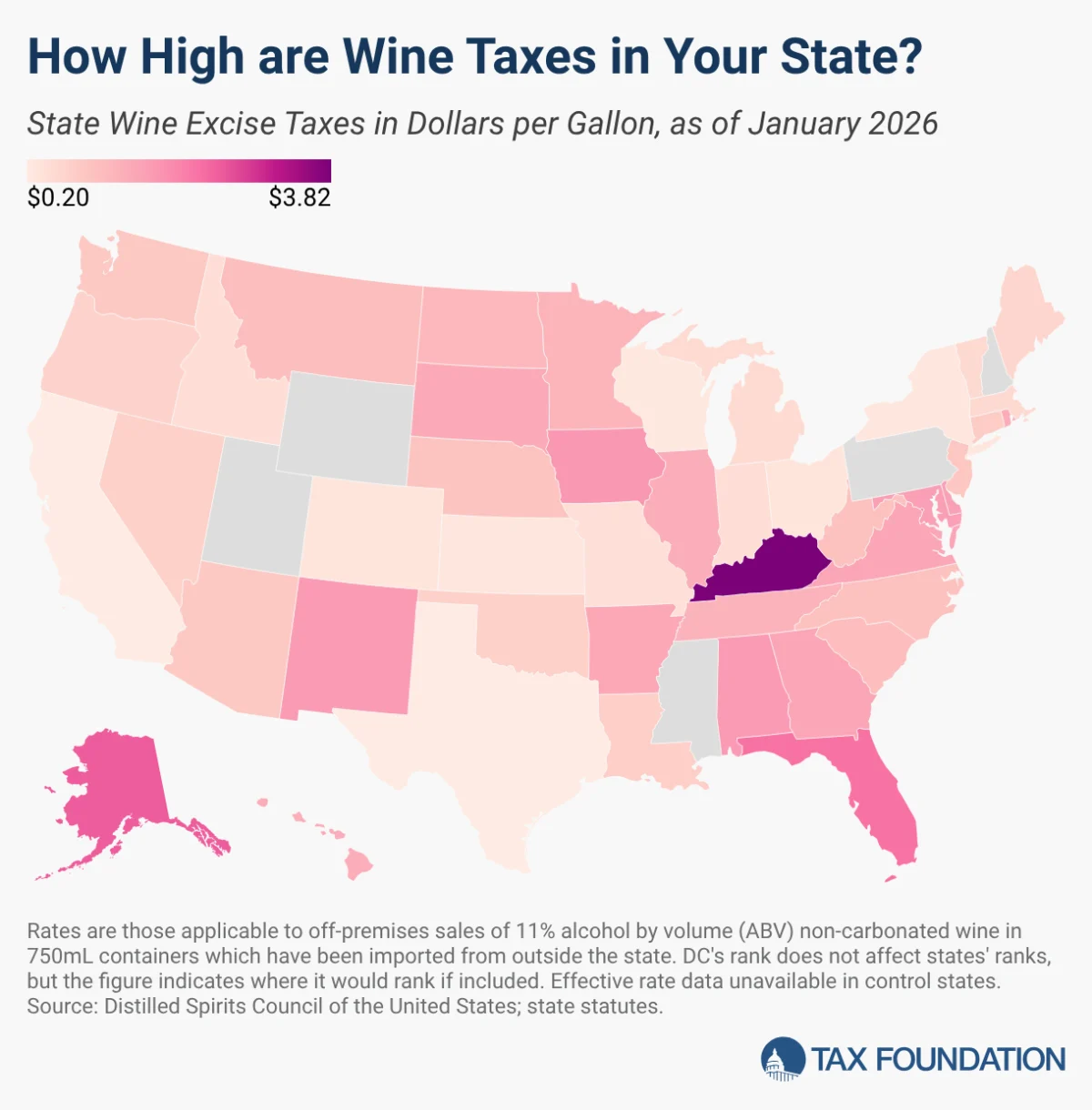

The tax burden on a bottle of wine is not distributed equally across the American map. A consumer in Kentucky faces a significantly different reality than a consumer in California.

The High-Cost Jurisdictions

Kentucky currently holds the title for the highest tax burden on wine in the nation, with an effective rate of $3.82 per gallon. This is largely driven by a 10 percent wholesale tax that compounds the underlying excise costs. Following Kentucky are Alaska ($2.50 per gallon), Florida ($2.25 per gallon), and Iowa ($1.75 per gallon). These states often argue that high taxes fund public health initiatives or alcohol treatment programs, though critics point out that these taxes are frequently diverted to general fund spending rather than their stated public health purposes.

The Low-Cost Jurisdictions

At the other end of the spectrum, California—the heart of American viticulture—maintains the lowest tax burden in the country at just $0.20 per gallon. This low-tax environment is often cited as a key factor in the state’s ability to foster a massive, competitive wine industry that dominates both domestic and international markets. Following California are Texas ($0.204), Wisconsin ($0.25), and New York ($0.30).

The "Control State" Anomalies

The situation becomes even more opaque in the five states that maintain a government monopoly on alcohol sales: Mississippi, New Hampshire, Pennsylvania, Utah, and Wyoming. In these "control states," pricing is not just a function of excise tax, but of artificial price markups mandated by the state.

- Utah: The state enforces a minimum markup of 88.5 percent on wine, essentially functioning as a massive hidden tax.

- Pennsylvania: The Liquor Control Board has the authority to manipulate prices, resulting in net margins that significantly inflate the final price to the consumer.

- New Hampshire: Interestingly, the state leverages its monopoly to offer lower effective taxes, reporting an average wine tax of just $0.046 per gallon, effectively using the state store model to drive volume.

Supporting Data: Federal vs. State Layers

It is important to note that state taxes are merely one layer of the onion. Every bottle sold in the United States is also subject to federal excise taxes. For a standard 11 percent ABV still wine, the federal rate is $1.07 per wine gallon.

However, the federal government provides a tiered system of tax credits for domestic producers. These credits significantly reduce the rate for the first 30,000, 130,000, and 750,000 wine gallons produced. This creates a "tiered advantage" for smaller, boutique wineries, which is often viewed as a mechanism to preserve the diversity of the industry. Nevertheless, when these federal credits are added to the disparate state-level excise taxes and the additional fees in states like Colorado, Idaho, and Washington—where a portion of the tax is specifically earmarked for "Wine Commissions" or "Agricultural Development Funds"—the consumer is left paying a premium that goes far beyond the cost of production.

Implications for the Future: A Call for Modernization

The current system of taxing wine is a relic of an era that did not account for globalized supply chains, the complexity of modern alcohol production, or the need for tax neutrality.

Economic Distortions

The primary implication of the current system is economic distortion. When taxes are high, they suppress demand, hurt small businesses, and incentivize consumers to purchase cheaper, lower-quality products to mitigate the cost. Furthermore, the practice of taxing the "broad market" to subsidize specific state-sponsored agricultural initiatives is a form of industrial policy that picks winners and losers at the expense of the average citizen.

The Case for ABV-Based Taxation

Policy experts, including those at the Tax Foundation, have long advocated for a shift toward an alcohol-by-volume (ABV) tax system. By taxing products directly according to their actual alcohol content, the system would become:

- Neutral: It would treat all alcoholic beverages equally, regardless of whether they are marketed as wine, beer, or spirits.

- Simple: It would eliminate the need for arbitrary categorical definitions that fail to keep pace with new beverage technologies.

- Predictable: It would provide a consistent revenue stream for states without relying on the manipulation of prices or the creation of government monopolies.

Conclusion

As the $7.2 billion estimated tax haul for 2025 demonstrates, the wine industry is a massive engine for state and federal revenue. However, the reliance on an arcane, disjointed, and often punitive tax structure is unsustainable. For the sake of both the consumer and the economic health of the wine industry, policymakers must look toward modernizing the tax code. Moving away from rigid, volume-based excise taxes and toward a neutral, ABV-based system would not only simplify the process but would also ensure that the price of a bottle of wine reflects its market value, not just its tax status.

Until such reform occurs, the next time you uncork a bottle, remember that you are paying for more than just the grapes; you are subsidizing a complex and often inefficient web of government fiscal policy.