In the complex architecture of European tax systems, Value Added Tax (VAT) remains the primary engine of government revenue. Yet, beneath the surface of these multi-billion-euro systems lies a quiet but consequential battleground: the VAT registration threshold. These thresholds—the turnover limits below which businesses are exempt from charging and remitting VAT—are intended to shield small enterprises from onerous administrative burdens. However, as recent data from the Tax Foundation reveals, these policies are increasingly fueling economic distortions that ripple across the continent.

The Landscape of VAT Exemptions: Nominal vs. Real Value

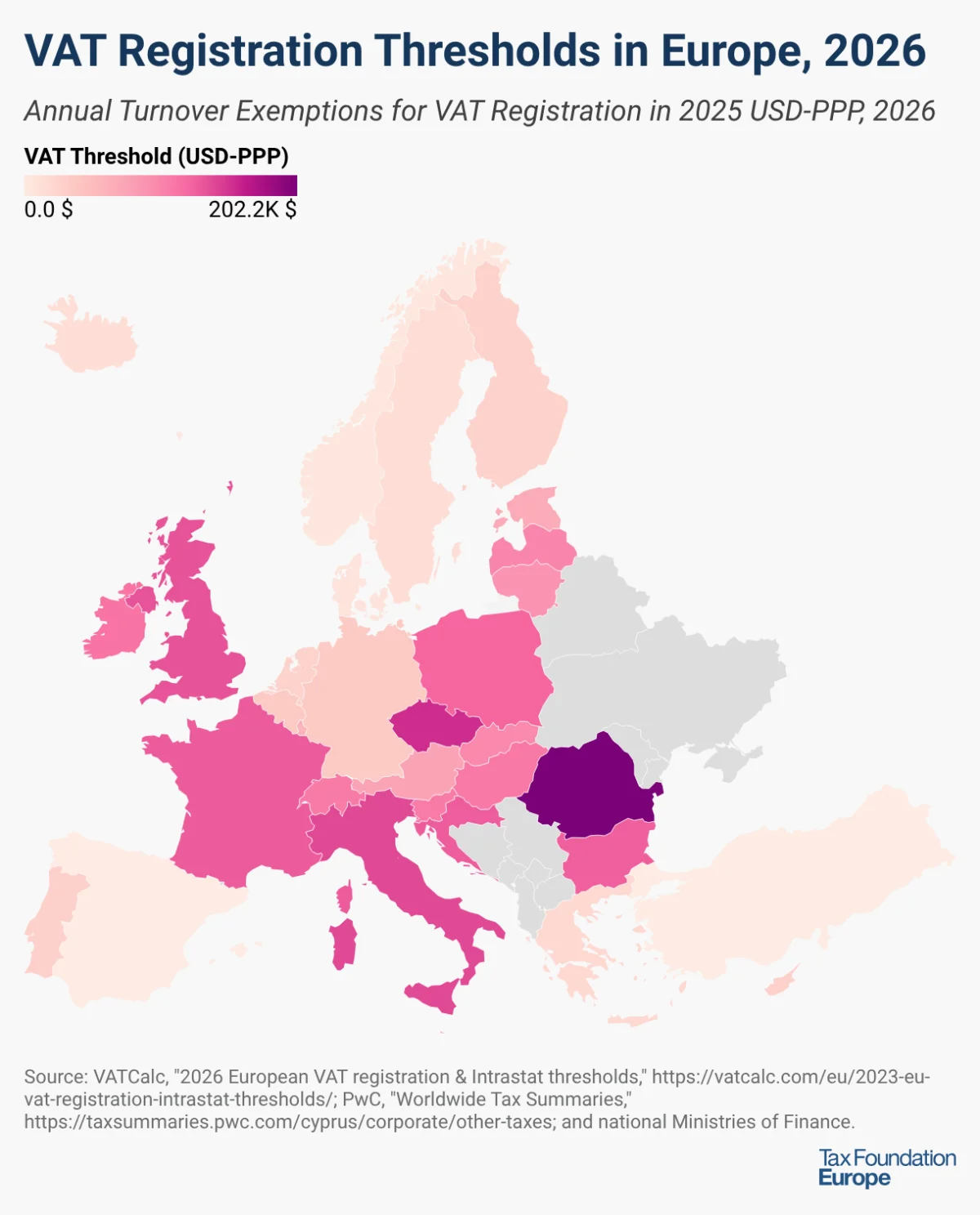

Across 32 major European nations, the approach to VAT thresholds varies wildly, reflecting a tension between ease of doing business and the need for a broad tax base. When measured in absolute nominal terms, Switzerland leads the pack, offering an exemption threshold of CHF 100,000 (€106,724). Following close behind are the United Kingdom at £90,000 (€105,043) and France at €87,000.

At the other end of the spectrum lie the “total inclusion” jurisdictions. Spain and Turkey stand as the only nations in the cohort that maintain a zero-threshold policy. In these countries, every business, regardless of size or revenue, is legally required to enroll in the VAT system. This approach eliminates the administrative "cliff" that plagues other nations but places a significant compliance burden on the smallest micro-enterprises and freelancers.

However, nominal figures often deceive. A threshold of €50,000 provides far more purchasing power in a low-cost economy than it does in a high-cost capital like Paris or London. When adjusting for Purchasing Power Parity (PPP)—which levels the playing field to reflect the actual economic weight of the currency—the leaderboard shifts dramatically. Romania emerges as the continental leader with a PPP-adjusted threshold of RON 395,000 ($202,206), followed by the Czech Republic (CZK 2,000,000 / $155,039) and Italy (€85,000 / $140,246).

The Economic Implications: Efficiency vs. Distortion

While the primary justification for VAT thresholds is the reduction of compliance costs for small businesses, the policy comes with a significant trade-off: tax revenue erosion. Beyond the immediate loss of income for the state, these thresholds introduce a structural distortion that favors micro-enterprises at the expense of productivity.

The "Notch" and the Tax Cliff

The most severe economic consequence of these thresholds is the "notch" effect. In many jurisdictions, a firm that crosses the threshold by a single euro suddenly incurs a liability for its entire value-added, rather than just the marginal amount exceeding the limit. This creates a psychological and financial "tax cliff."

Empirical studies, including recent analysis by the International Monetary Fund (IMF), suggest that this structure incentivizes "bunching." Businesses often artificially cap their growth, underreport turnover, or scale back operations specifically to avoid crossing the threshold. By artificially keeping firms small, these thresholds prevent businesses from achieving the economies of scale necessary to compete in a global market. When tax-advantaged micro-enterprises are protected from the competitive pressures of the broader market, they effectively crowd out more productive, efficient firms, stifling overall economic growth.

The Czech Case Study

The Czech Republic serves as a cautionary tale of the distortionary impact of high thresholds. Because the country maintains one of Europe’s highest PPP-adjusted limits, researchers have observed a distinct spike in the distribution of corporate turnover immediately below the cutoff. As the government has periodically raised the threshold, the "bunching point" has tracked upward in lockstep. This phenomenon proves that firms are not organically small; rather, they are being shaped by the tax code to remain small, illustrating a massive misallocation of resources across the national economy.

A Chronology of Recent Policy Shifts

Despite the economic warnings regarding "bunching" and productivity loss, the trend across Europe in 2025 and 2026 has been a consistent expansion of these thresholds. Governments are under significant pressure from small-business lobbies to provide relief amidst inflationary environments, leading to a wave of legislative updates.

- September 2025: Romania took a major step, increasing its VAT registration threshold from RON 300,000 to RON 395,000, signaling a move to further reduce the tax compliance burden on its burgeoning small-business sector.

- January 2026: Poland implemented an increase from PLN 200,000 to 240,000, effectively raising the threshold in euro terms to approximately €56,610.

- Early 2026: Hungary executed a phased increase. The threshold rose from HUF 18 million to 20 million (€50,280) in early 2026, with a further scheduled increase to HUF 22 million (€55,310) set for 2027.

- April 2026: The Belgian parliament signaled a shift toward liberalization by approving an increase in the VAT exemption threshold from €25,000 to €30,000. While the measure is pending final implementation, it reflects the broader European sentiment toward expanding relief for micro-entities.

Official Perspectives and the Debate on Reform

The debate between tax administrators and economic policy experts remains polarized. For politicians, the VAT threshold is a popular tool for political capital. It is perceived as a "pro-growth" measure for the self-employed, who are often viewed as the backbone of the economy. Raising the threshold is an easy way to provide immediate, tangible relief without the need for complex, long-term structural reforms.

Conversely, tax economists and international institutions are increasingly calling for the elimination or significant reduction of these thresholds. The argument is that modern technology—such as digital invoicing and real-time reporting—has drastically lowered the cost of tax compliance.

"The traditional justification for high VAT thresholds—that small businesses lack the capacity to manage complex tax filings—is becoming obsolete," notes one policy expert. "With automated software, the cost of being ‘in the system’ is negligible compared to the economic damage caused by distorting business behavior."

The Path Forward: Minimizing Economic Costs

To mitigate the negative externalities of the VAT threshold, policymakers face a difficult path. The goal is to move away from the "all-or-nothing" cliff that triggers such extreme behavioral responses.

- Phased Transitions: Some economists propose a "tapered" system where a business that exceeds the threshold is not immediately fully liable, but rather faces a gradual phase-in of VAT obligations. This would remove the cliff, eliminating the incentive to suppress growth.

- Harmonization: A major point of contention is the lack of alignment across the European Union. As the Single Market deepens, the disparate thresholds create "tax havens" for micro-entities that can impact cross-border competition.

- Digital Integration: By mandating digital tax reporting, governments can reduce the "administrative burden" argument, thereby justifying a lower threshold that captures more revenue without disproportionately punishing small business owners.

Conclusion

The VAT registration threshold represents a fundamental dilemma in fiscal policy. While it offers a reprieve to the smallest actors in the economy, it does so at the cost of long-term productivity and tax neutrality. As nations like Hungary, Poland, and Romania continue to push their thresholds higher, they are arguably exacerbating the "bunching" effect that keeps their local economies fragmented.

For European policymakers, the challenge is to move beyond the short-term political appeal of tax exemptions. To foster a truly competitive, high-productivity environment, the focus must shift from protecting businesses from the tax system to integrating them into a modernized, digital-first framework that minimizes distortion and ensures that every firm, regardless of size, contributes its fair share to the public coffers. Until then, the "VAT cliff" will remain a silent architect of European corporate strategy, holding back the very growth that governments are so eager to encourage.