Fixed income markets have undergone a profound transformation over the last few months, driven by the volatile intersection of escalating geopolitical tensions in the Middle East and a recalibration of macroeconomic expectations. As investors grapple with the fallout from the Iran conflict and persistent economic signals, the U.S. Treasury market has absorbed a significant repricing. However, rather than succumbing to panic, the market has demonstrated a remarkable level of efficiency, processing "bad news"—higher-for-longer interest rates, energy-linked inflation, and term premia—with a measured approach that suggests much of the current risk is already priced into the yield curve.

Main Facts: A Shift in the Rate Landscape

The central narrative defining the current fixed income environment is the decisive move toward a "higher-for-longer" reality. Treasury yields have experienced a sharp upward trajectory, fueled by three distinct drivers: an upward revision of growth expectations, an increase in term premia (the extra yield investors demand for holding long-term debt), and a fundamental reassessment of Federal Reserve policy.

Crucially, this adjustment has occurred without a catastrophic collapse in economic data or a decoupling of long-term inflation expectations. This resilience suggests that the market has moved beyond the post-pandemic assumption that the economy would quickly return to a low-neutral-rate environment. Instead, participants are pricing in a structurally higher equilibrium, acknowledging that labor market strength, sticky services inflation, and potential productivity gains from the artificial intelligence (AI) buildout necessitate a higher terminal fed funds rate.

Chronology: The Arc of Recent Market Adjustments

The current repricing can be traced back to the onset of the Iran conflict, which acted as a primary catalyst for market volatility.

- Initial Shock (Pre-Conflict): Earlier in 2026, the prevailing market sentiment was anchored in the expectation of multiple rate cuts throughout the year, as investors bet on a cooling economy and a swift decline in inflation.

- The Conflict Catalyst: Following the escalation of the Iran conflict, the U.S. Treasury curve experienced a "bear flattening." Front-end yields rose dramatically, reflecting immediate concerns over energy price volatility and the potential for a central bank response.

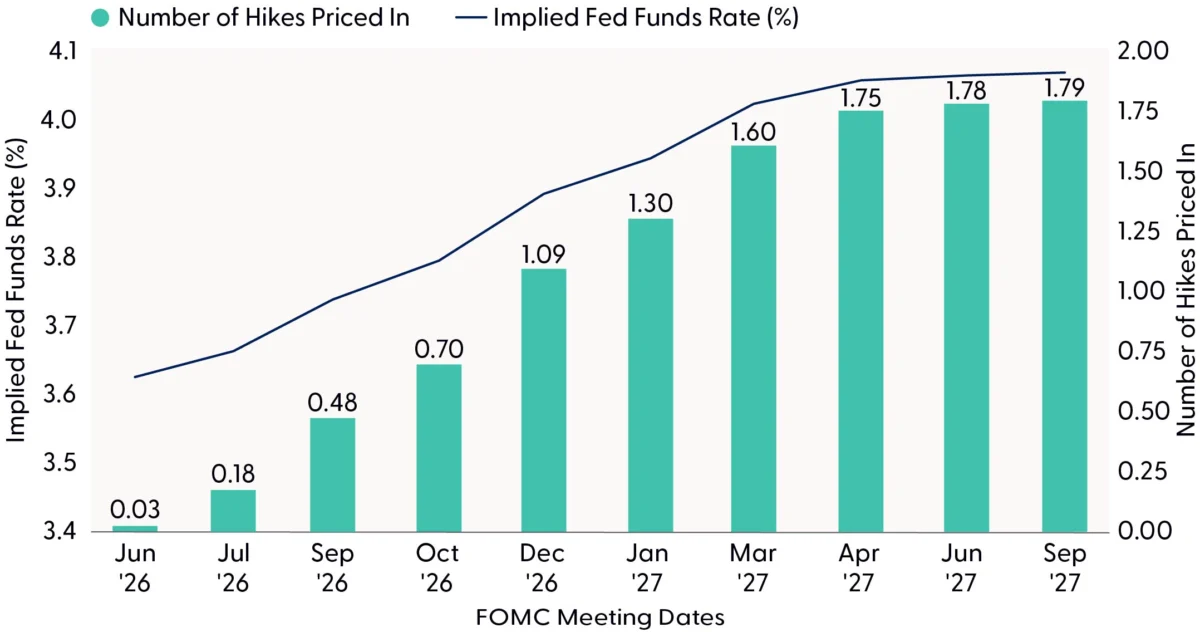

- The Mid-Year Repricing: By the beginning of June 2026, the data began to solidify this new reality. Stronger-than-expected economic indicators forced a total reversal of the rate-cut narrative. Markets shifted from anticipating cuts to pricing in a near 100% probability of a rate hike before the year’s end, with a 67% chance of two additional hikes by mid-2027.

- The Current State: As of early June, the market has stabilized at these higher levels. While Treasury yields remain elevated, the absence of acute stress in funding markets or forced selling indicates that the initial shock phase has passed, and the market is now operating under a new, higher baseline.

Supporting Data: Dissecting the Yield Curve

To understand the current state of the market, one must look at the specific components driving yield movements. Since the escalation in the Middle East, the 2-year Treasury yield has risen by approximately 60 basis points (bps), while the 10-year Treasury yield has climbed by 77 bps.

A critical component of this movement is the decomposition of the 10-year yield. Analysis reveals that roughly 35 bps of the increase is directly attributable to rising real growth expectations. This is a vital distinction: it indicates that investors are not merely pricing in "inflation fear," but rather a "soft landing plus" scenario—a resilient economy that is potentially outperforming previous forecasts. Only a small fraction of the yield increase (about 14 bps) is tied to higher inflation compensation.

Furthermore, the "anchoring" of long-term inflation expectations remains a cornerstone of current market stability. Unlike the 2022 inflationary spike, where expectations drifted dangerously upward alongside actual prices, current breakeven rates suggest that the market views current inflationary pressures as transitory, linked primarily to energy volatility rather than systemic price instability. This confidence is bolstered by the Fed’s established credibility, which provides a buffer against extreme scenarios.

Official Responses and Policy Optionality

The Federal Reserve now finds itself in a position of "optionality." The shift in the implied neutral fed funds rate to approximately 4% has brought market pricing closer to the hawkish projections of the Federal Open Market Committee (FOMC).

Fed officials, including Governor Chris Waller, have acknowledged that if the data continues to show resilience and inflation remains sticky, a rate hike is a viable policy tool. However, the Fed is not currently compelled to act. Because long-run inflation expectations remain well-anchored, the central bank has the flexibility to wait for further evidence before tightening policy further.

This environment suggests that the "bar" for a rate hike is significantly higher than the bar for maintaining the status quo. Policymakers are essentially using their hawkish rhetoric as a form of tightening—attempting to manage financial conditions through communication rather than immediate action. By signaling a willingness to hike, the Fed is successfully keeping long-term expectations in check without needing to disrupt economic momentum.

Implications: Strategic Asset Allocation

The implications for investors are clear: the era of "easy" returns from duration is likely paused, but the outlook is not inherently bearish. The substantial repricing that has already occurred means that a significant portion of potential "bad news" is already reflected in asset prices.

The View from the STAAC

LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) has adopted a neutral stance on duration. The committee’s proprietary models suggest that while yields have reached a point where they are attractive, the current economic climate warrants caution.

- Fixed Income Positioning: The committee maintains an underweight position in investment-grade corporate bonds and mortgage-backed securities (MBS). Given that credit spreads remain tight relative to historical norms, the risk-reward profile for these sectors is currently unfavorable.

- Equity Strategy: A tactical equity overweight remains recommended. This view is based on the expectation that geopolitical supply concerns will eventually ease, allowing the underlying resilience of the corporate sector—driven by productivity gains—to drive performance.

- The "Trigger" Points: The STAAC is monitoring the 10-year Treasury yield closely. Should it rise into the 4.75%–5.00% range, the committee would view this as a compelling entry point to add duration, as such levels would likely overcompensate for the current risks to the economy.

Conclusion: A Balanced Risk-Reward Profile

The fixed income landscape has been tested by geopolitical upheaval and a pivot in monetary policy, yet it has responded with maturity and efficiency. The Treasury market’s ability to digest the shift toward a higher neutral rate while maintaining anchored inflation expectations is a testament to the underlying health of the financial system.

While the prospect of a rate hike remains a headline risk, the reality is that the Fed is no longer "behind the curve" as it was in 2022. The market has already priced in the most likely adverse outcomes. Absent a dramatic resurgence in oil prices or an unpredicted acceleration in inflation, the rapid surge in yields is likely behind us.

For investors, the current environment is less about predicting the "next crash" and more about recognizing that the "bad news" is already in the price. The path forward will be dictated by the Fed’s ability to maintain its credibility while navigating a growth-oriented, high-rate economy. In this context, a disciplined, neutral approach to duration, combined with a focus on high-quality assets and defensive equity factors, represents the most prudent strategy for navigating the remainder of the 2026 cycle.