The Federal Reserve’s strategy of patient vigilance is facing its most severe test yet. For months, monetary policymakers have maintained a steady hand on interest rates, operating on the assumption that the recent resurgence in inflation would prove temporary. However, that assumption has become significantly harder to defend.

The release of the May Personal Consumption Expenditures (PCE) price index—the Federal Reserve’s preferred inflation metric—reveals that pricing pressures are expanding far beyond the volatile energy costs associated with the ongoing conflict in the Middle East. With core inflation metrics creeping upward and services-sector inflation accelerating, the central bank’s room for maneuver is rapidly shrinking.

The developing macroeconomic picture presents an immediate challenge for the newly appointed Federal Reserve Chairman, Kevin Warsh. As Warsh seeks to establish his policy credentials, the bond market is flashing warning signs, signaling that investors may soon lose patience if the central bank fails to address these persistent underlying price pressures.

Main Facts: Broadening Price Pressures and the Fed’s Dilemma

The latest PCE inflation data has disrupted the narrative that current inflationary pressures are merely a temporary byproduct of geopolitical instability. While the spike in energy prices driven by the Iran conflict initially shielded the Fed from criticism, the May data demonstrates that price increases have integrated into the broader domestic economy.

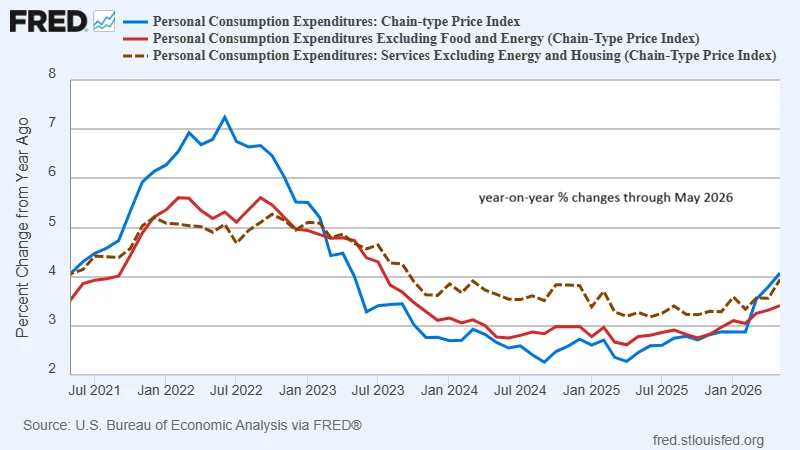

Headline Inflation Hits Three-Year High

According to the Commerce Department’s latest update, the headline PCE price index rose to a 4.1% year-over-year increase in May. This represents the fastest pace of annual inflation recorded in three years. While some supply-side economists argue that energy costs have peaked and will soon drag the headline figure down, the underlying components of the report tell a much more concerning story.

Core and Services Inflation Accelerate

The core PCE price index, which strips out volatile food and energy components to provide a clearer view of long-term inflation trends, rose to an annual rate of 3.4% last month.

Even more troubling for policymakers is the "supercore" inflation metric—specifically, PCE services prices excluding both energy and housing. This metric, which is highly sensitive to domestic labor market conditions and wage growth, accelerated to 3.9% year-over-year. The steady climb in supercore inflation suggests that price pressures are now driven by domestic demand rather than imported supply shocks.

The Bond Market’s Reaction

The financial markets are closely monitoring these developments. The policy-sensitive U.S. 2-year Treasury yield closed yesterday at 4.14%. Although this represents a minor decline over the last three sessions, the yield remains locked in a clear upward trend.

Crucially, the 2-year yield sits well above the Federal Reserve’s current target range of 3.50% to 3.75%. This discrepancy indicates that fixed-income investors are pricing in the necessity of further monetary tightening, regardless of the Fed’s current pause.

Chronology: From Pandemic Shocks to the 2026 Inflation Resurgence

To understand the gravity of the Federal Reserve’s current position, it is necessary to examine the policy decisions and economic events that have shaped the current rate cycle over the last several years.

[2021–2022] Pandemic-Era Inflation Surge -> Fed delays response due to "transitory" policy narrative

│

[2023–2024] Aggressive Monetary Tightening -> Rates raised; inflation cools toward target

│

[2025] Policy Stabilization -> Fed lowers target range to 3.50%–3.75%

│

[Early 2026] Geopolitical Shocks -> Iran conflict triggers energy price spike; headline inflation rises

│

[May 2026] Underlying Inflation Broadens -> May PCE data reveals core and services inflation accelerating

│

[Present] The Credibility Test -> Fed Chair Kevin Warsh faces pressure to abandon patience for hawkish pivot1. The Legacy of the 2021–2022 Policy Error

During the immediate post-pandemic recovery, the Federal Reserve under previous leadership maintained highly accommodative monetary policy, famously classifying rising prices as "transitory." This delayed response allowed headline inflation to peak at multi-decade highs, forcing the central bank into an aggressive, retroactive tightening cycle that strained global financial systems. This period remains a stark warning of the dangers of central bank hesitation.

2. Stabilization and the Transition to Easing (2023–2025)

Following aggressive interest rate hikes, inflation began to cool toward the Fed’s 2.0% target. By late 2025, the central bank felt comfortable lowering its benchmark policy rate to the current target range of 3.50% to 3.75%, aiming for a "soft landing" that would preserve labor market gains while maintaining price stability.

3. The 2026 Geopolitical Energy Shock

In early 2026, escalations in the Middle East—specifically involving Iran—triggered a sudden spike in global crude oil and energy prices. Headline inflation measures began to drift upward. Fed officials initially preached patience, arguing that these supply-side shocks would subside once energy markets normalized.

4. The May 2026 PCE Revelation

The release of the May PCE data has challenged the supply-shock narrative. The data shows that while energy prices may indeed be stabilizing, core inflation and services-sector prices are climbing independently. This shift has forced the Federal Open Market Committee (FOMC) to confront the reality that domestic inflation pressures are rebuilding.

Supporting Data: A Comparative Analysis of Inflation Metrics

To evaluate the strength of the inflationary trend, analysts look at several different measures of price changes. Each metric offers a different perspective on how deeply inflation has penetrated the economy.

| Inflation Metric | May Annual Rate | Target Rate | Policy Implication |

|---|---|---|---|

| Headline PCE | 4.1% | 2.0% | Reflects immediate consumer pain; heavily influenced by energy and food. |

| Core PCE (Excl. Food & Energy) | 3.4% | 2.0% (Implicit) | Indicates persistent underlying demand; suggests inflation is structural. |

| Supercore PCE (Services Excl. Housing/Energy) | 3.9% | N/A | Highly tied to wage growth; signals a tight domestic labor market. |

| Dallas Fed Trimmed Mean PCE | 2.4% | 2.0% | Filtered metric used by the Fed to dismiss short-term volatility. |

The Core vs. Headline Divergence

The headline PCE of 4.1% is a clear warning sign, but the core rate of 3.4% is arguably more concerning for long-term planning. Because core PCE strips out the direct effects of the Iran conflict on fuel prices, its steady climb indicates that businesses across the economy are raising prices to offset broader operational costs, including wages and logistics.

The Supercore Acceleration

At 3.9%, the supercore services metric shows that inflation is firmly entrenched in service-oriented industries. Unlike manufactured goods, which are subject to global supply chain dynamics, service pricing is driven almost entirely by domestic factors. This suggests that the current monetary policy setting of 3.50% to 3.75% may not be restrictive enough to cool domestic demand.

The Trimmed Mean Counter-Argument

The primary defense for maintaining steady rates rests on the Dallas Fed’s "Trimmed Mean" PCE. This calculation removes the most extreme price increases and decreases in any given month to establish a stable baseline.

In May, the Trimmed Mean PCE ticked up slightly to an annual rate of 2.4%. While this figure is much closer to the Fed’s 2.0% target, critics point out that the Trimmed Mean is historically slow to react to broad economic shifts. During the 2021–2022 inflation wave, this metric failed to signal danger until inflation was already well established.

Official Responses and Policy Perspectives

The broadening of inflation pressures has sparked an intense debate within policy circles, focusing heavily on the strategy of the newly appointed Federal Reserve Chairman, Kevin Warsh.

"The bond market is currently giving Chairman Warsh the benefit of the doubt, but that patience is not infinite. If core PCE does not cool soon, the market will force his hand."

— Fixed Income Strategy Note, June 2026Chairman Warsh’s Price Stability Pledge

In his public statements, Chairman Warsh has emphasized his commitment to restoring price stability, recognizing that his institutional credibility is on the line. Having taken leadership of the central bank during a period of economic transition, Warsh must balance the need to curb inflation with the risk of triggering an unnecessary economic slowdown.

During his Senate confirmation hearings and in policy statements last week, Warsh repeatedly pointed to the Trimmed Mean PCE as a reliable guide for monetary policy, suggesting he remains reluctant to rush into rate hikes based on volatile headline data.

The Hawkish Response

A growing coalition of regional Fed presidents and independent economists argue that relying on the Trimmed Mean is a dangerous strategy. They contend that the May PCE report proves the Fed is falling "behind the curve" once again.

These hawks warn that if the Fed does not signal a willingness to raise rates soon, inflation expectations could become unanchored, making eventual control much more painful and economically disruptive.

Market Expectations and the FedWatch Tool

According to the CME FedWatch Tool, futures markets continue to project that the FOMC will leave the federal funds rate unchanged at its upcoming meeting. However, the probability of a rate hike at the September meeting has risen significantly. Investors are increasingly viewing a autumn rate hike as a highly probable outcome if core PCE readings do not show a clear reversal in the summer months.

Implications: Credibility, Policy Pivots, and Market Stability

The Federal Reserve’s handling of the May PCE data will have significant consequences for financial markets and the broader global economy.

The Credibility Risk for Chairman Warsh

For any new central bank leader, establishing credibility is a primary objective. If financial markets lose confidence in Warsh’s commitment to price stability, long-term inflation expectations could rise, pushing bond yields higher and complicating the Fed’s policy objectives.

If Warsh relies too heavily on the slower-moving Trimmed Mean PCE while core and services inflation continue to rise, he risks repeating the policy mistakes of 2021–2022. This would damage his standing with both financial markets and public observers.

Potential for a Hawkish Policy Pivot

Should upcoming inflation reports fail to show a clear deceleration in core prices, the Fed may be forced to abandon its patient stance. A hawkish pivot—potentially involving a 25-basis-point rate hike in September—would signal that the central bank is willing to accept slower economic growth to bring inflation back to its 2.0% target.

Such a move would catch many equity market participants off guard, as they have spent the last several quarters pricing in steady or declining borrowing costs.

Market Volatility and Financial Conditions

The divergence between the Fed’s policy rate (3.50%–3.75%) and the 2-year Treasury yield (4.14%) indicates that financial conditions are already tightening through market mechanisms. If the Fed continues to hold rates steady while inflation rises, the bond market may continue to push yields higher, effectively raising borrowing costs for corporations and consumers without the Fed’s explicit action. This scenario could lead to increased volatility in both equity and fixed-income markets.

Ultimately, the Federal Reserve’s window for patience is closing. While geopolitical factors like the Iran conflict provided a temporary explanation for rising prices, the broad-based nature of May’s PCE data shows that domestic inflation remains a persistent challenge. How Chairman Warsh navigates this challenge in the coming months will determine not only the path of the U.S. economy but also the institutional credibility of the Federal Reserve for years to come.