Just as global financial markets are beginning to move past the painful macroeconomic disruptions of energy inflation, geopolitical volatility, and stubborn central bank monetary tightening, a new source of systemic instability is building in the Pacific.

The National Oceanic and Atmospheric Administration (NOAA) has officially confirmed the formation of El Niño conditions over the tropical Pacific Ocean. Early meteorological models suggest that this iteration could develop into one of the most powerful climatic events in decades.

While El Niño is fundamentally a meteorological phenomenon, its systemic reach extends far beyond weather patterns. It has the potential to trigger a severe supply-side shock to global agriculture, distorting commodity prices, complicating central bank mandates, and introducing fresh volatility into global equity, fixed-income, and foreign exchange markets.

1. Main Facts: The Mechanics of a Climate-Driven Economic Threat

El Niño is a naturally occurring climate pattern characterized by the periodic warming of sea surface temperatures in the central and eastern equatorial Pacific. Under normal conditions, trade winds blow west across the Pacific, pushing warm surface water toward Asia and Oceania. During an El Niño event, these trade winds weaken or, in severe cases, reverse. This allows the warm surface water to drift backward toward the western coast of the Americas.

NORMAL CONDITIONS:

[Americas] <--- Trade Winds (Push Warm Water) <--- [Asia/Oceania]

Result: Warm water pools in the West; cool, nutrient-rich water rises in the East.

EL NIÑO CONDITIONS:

[Americas] ---> Weakened/Reversed Winds ---> [Asia/Oceania]

Result: Warm water shifts Eastward toward the Americas; rainfall patterns disrupt globally.This eastward displacement of ocean heat dramatically alters global atmospheric circulation and rainfall patterns:

- The Americas: Typically experience significantly heavier precipitation and flooding, particularly along the Pacific coast of South America and the southern United States.

- Asia-Pacific and Southern Africa: Face the opposite extreme—severe droughts, prolonged heatwaves, and delayed monsoons. This directly threatens key agricultural regions in South and Southeast Asia, Australia, and Southern Africa.

By disrupting planting cycles, damaging crop yields, and bottlenecking agricultural logistics, El Niño acts as a direct supply-side shock. Coming on the heels of an inflation cycle dominated by fossil fuels and geopolitical friction, the next major wave of global inflation may find its origins not in oil fields or semiconductor fabs, but in the soil.

2. Chronology: The Lifecycle and Cascading Impact of ENSO

Understanding the timeline of El Niño is critical for market participants, as agricultural commodities trade heavily on forward-looking expectations. The progression of an El Niño shock typically follows a distinct chronological path.

[Phase 1: Spring] [Phase 2: June-September] [Phase 3: Autumn/Winter]

Spring Predictability Barrier Indian Monsoon Catalyst Harvest Disruptions &

Models show low reliability Rainfall deficit shapes crop Physical supply squeezes

before summer signals clear. outlooks in South/SE Asia. manifest in global CPI.The Spring Predictability Barrier

In the initial stages of an El Niño cycle, forecasting models encounter what meteorologists call the "spring predictability barrier." During this period (typically Northern Hemisphere spring), climatic indicators are highly fluid, making it difficult to project the ultimate intensity of the system.

As a result, financial futures markets often experience a lag, remaining tied to near-term physical inventories and spot prices. It is only as summer approaches and the barrier breaks that models gain high-confidence reliability, triggering rapid adjustments in forward curves.

The Critical Catalyst: The Indian Monsoon (June–September)

The first major geographical test of the El Niño cycle occurs during the Indian monsoon season, spanning June through September. The monsoon is the lifeblood of South Asian agriculture, directly determining the yields of water-intensive crops such as rice, cotton, sugar, and oilseeds.

A normal monsoon season can absorb much of the regional El Niño risk. However, a severe rainfall deficit during this window acts as the primary catalyst that transforms a meteorological forecast into a tradable, high-impact market dislocation.

The Historical Precedent: The 2024 Cocoa Crisis

To understand how devastating these compounding weather cycles can be, one only has to look at the recent historical precedent of the cocoa market. West Africa—specifically Ivory Coast and Ghana, which together supply nearly 50% of the world’s cocoa—is highly sensitive to ENSO-driven weather anomalies.

During the last major El Niño cycle, these regions first suffered from unseasonably heavy, uncoordinated rainfall, which fostered widespread black pod disease and rotted crops on the vine. This was immediately followed by intense heatwaves and dry, dusty Harmattan winds.

The resulting structural supply deficit caused cocoa prices to nearly triple over the course of 2024, skyrocketing past $12,000 per metric ton. This extreme pricing pressure forced global chocolate manufacturers to compress margins, adjust product sizes, and pass historic costs down to consumers.

3. Supporting Data: Quantifying the Macroeconomic and Commodity Toll

The macroeconomic consequences of El Niño are well-documented, with central banks and academic institutions providing clear empirical evidence of its inflationary transmission channels.

The Inflation Transmission Channel

Research from the Federal Reserve reveals a stark correlation between climate anomalies and global inflation, finding that approximately 20% of historical commodity price movements can be directly linked to the El Niño-Southern Oscillation (ENSO) cycle.

A standard El Niño event typically lifts real global commodity price inflation by roughly 3 percentage points over a 6-to-12-month horizon. Crucially, agricultural and food commodities bear almost the entirety of this upward pressure.

[El Niño Event]

│

▼

[~20% of Commodity Price

Movements Linked]

│

┌─────────┴─────────┐

▼ ▼

[Fed Estimate] [IMF Research]

+3% Real Commodity +5% Non-Energy Prices

Price Inflation lasting 6-16 months

(over 6-12 months)This finding is reinforced by International Monetary Fund (IMF) researchers (Cashin, Mohaddes, and Raissi), who estimate that a strong El Niño episode can drive an increase of approximately 5% in global non-energy commodity prices, with the inflationary impulse persisting for 6 to 16 months.

Divergent Global Impacts

The economic fallout of El Niño is highly asymmetric, creating stark regional divides:

- High-Exposure Nations: Countries like Australia, India, Indonesia, South Africa, Chile, and the Andean nations face significant domestic output losses due to damaged harvests, water scarcity, and disrupted mining operations.

- Insulated Nations: The United States and parts of Europe often experience a neutral or even mildly positive impact. Wetter weather in the U.S. plains can boost domestic crop yields, while the European Union benefits from structural agricultural protections. According to the Banco de España, El Niño has historically reduced Eurozone inflation by approximately 0.3 percentage points after 12 months, primarily due to the insulating effects of the Common Agricultural Policy (CAP), which buffers European consumers from global price volatility.

Commodity-Specific Vulnerabilities

| Commodity | Primary Producing Regions Exposed | El Niño Impact & Price Risk Profile |

|---|---|---|

| Cocoa | Ivory Coast, Ghana | Extremely High. Vulnerable to crop diseases from erratic rain, followed by intense heat. |

| Palm Oil | Indonesia, Malaysia | High. Severe dryness impairs fruit-bearing cycles, tightening global vegetable oil supplies. |

| Cotton | India, United States | Moderate-High. Heavily dependent on the Indian monsoon; dry spells reduce staple lengths and yields. |

| Coffee | Vietnam, Indonesia (Robusta); Brazil (Arabica) | High (Robusta). Vietnam and Indonesia face intense heat. Arabica is more nuanced; Brazil may see lower initial frost risk but faces late-season heat. |

| Sugar | India, Thailand, Brazil | Moderate. Monsoon shortfalls in Asia threaten yields, though India often mitigates this by diverting sugar away from ethanol production. |

| Rice | India, Southeast Asia | Extremely High. Directly tied to monsoon volumes. Shortages trigger export bans and severe food security risks. |

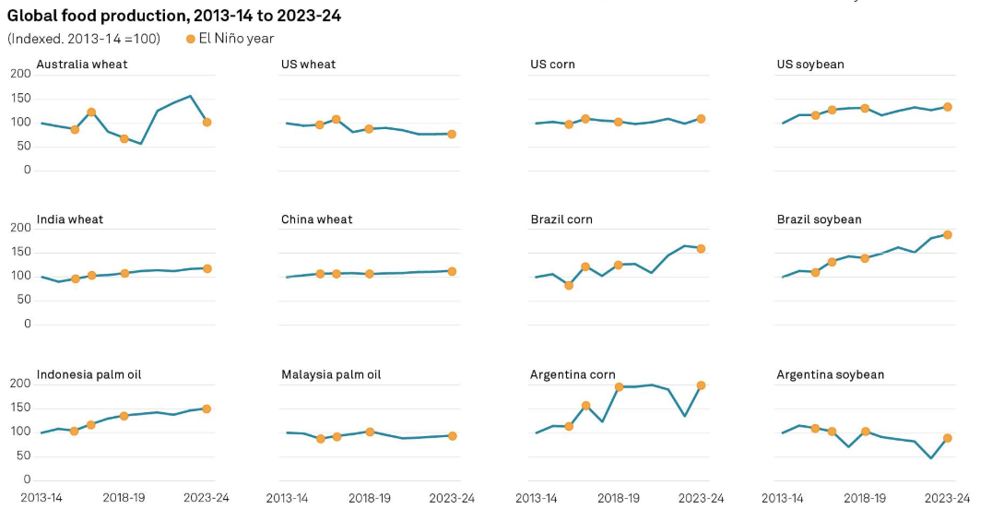

| Soybeans | Brazil, Argentina, United States | Low-Mixed. Often benefits from increased rainfall in South America, offsetting losses elsewhere. |

| Natural Gas | Northern Hemisphere | Neutral-Bearish. Typically leads to milder Northern winters, reducing heating demand, though geopolitical bottlenecks (e.g., Strait of Hormuz) can distort this. |

4. Official Responses: Policy Maneuvers and Central Bank Constraints

When El Niño disrupts supply chains, governments and central banks are forced to pivot quickly to protect domestic economies, often resulting in protectionist trade measures and tighter monetary policy.

[El Niño Shock]

│

┌──────────┴──────────┐

▼ ▼

[EM Central Banks] [Sovereign Governments]

• High CPI food weight • Export bans (e.g., Rice)

• FX depreciation • Strategic reserves release

• Higher-for-longer • Ethanol-to-food diversionCentral Bank Dilemmas in Emerging Markets

For central banks in developed nations, food inflation is often a temporary "noise" that can be looked through. However, in emerging markets (EMs), food accounts for a massive portion of the consumer price index (CPI) basket—often exceeding 30% to 40%.

When food prices surge, it quickly de-anchors local inflation expectations, weakens domestic currencies, and triggers imported inflation. Consequently, EM central banks in Latin America, Sub-Saharan Africa, and Southeast Asia are frequently forced to maintain a "higher-for-longer" interest rate stance, limiting their ability to ease monetary policy to support growth.

Government Interventions and Trade Protectionism

To shield domestic populations from rising food costs, governments frequently resort to interventionist policies that can exacerbate global supply squeezes:

- Export Restrictions: During previous El Niño events, major agricultural exporters like India have implemented sudden bans on non-basmati rice exports to secure domestic supply, triggering price spikes across global grain markets.

- Policy Flexibility (The Ethanol Buffer): Some nations use regulatory levers to absorb supply shocks. For example, India has the capacity to redirect 3 to 4 million metric tons of sugar sugarcane feedstock away from ethanol biofuel production and back into food-grade sugar manufacturing. While this stabilizes domestic food prices, it can tighten regional biofuel markets.

- International Agency Warnings: Organizations such as the World Bank, the World Meteorological Organization (WMO), and the FAO continuously monitor these developments. The World Bank’s baseline projections suggest a 16% rise in headline commodity prices in 2026—primarily driven by energy and fertilizer inputs. A severe El Niño acts as a major upside risk to this baseline, threatening to turn a projected decline in agricultural prices into a prolonged inflationary squeeze.

5. Implications: Financial Markets and Asset Allocation

For institutional investors and asset allocators, a powerful El Niño requires active portfolio adjustments to hedge against inflation and exploit sectoral disparities.

[FINANCIAL MARKET IMPLICATIONS]

│

┌──────────────────────────┼──────────────────────────┐

▼ ▼ ▼

[Equities] [Fixed Income & FX] [Commodities]

• Long: Fertilizer, Agri-Tech • Long: Commodity Exporters • Long: Softs (Cocoa,

• Short: Food Processors, (BRL, AUD) Robusta Coffee, Rice)

Beverages, Insurers • Short: Food Importers • Timing: Watch Spring

(TRY, INR, EMs) Predictability BarrierEquity Market Winners and Losers

- The Winners (Upstream Agricultural Inputs): Companies specializing in fertilizers (such as potash, phosphates, and nitrogen), crop protection chemicals, advanced seed technologies, and agricultural machinery typically experience robust demand. Farmers facing difficult weather conditions must invest more heavily in inputs to maximize yields on viable acreage.

- The Losers (Downstream Food & Beverage): Food processors, packaged food conglomerates, and beverage manufacturers face severe margin compression. These companies are highly sensitive to raw ingredient costs (sugar, cocoa, coffee, vegetable oils). If they attempt to pass these costs entirely to consumers, they risk demand destruction; if they absorb them, profitability declines.

- The Vulnerable (Insurance and Reinsurance): The insurance sector faces heightened catastrophe risk. Increased frequencies of wildfires in Australia, severe droughts in Africa, and heavy flooding along the Americas’ Pacific coast lead to elevated agricultural and property insurance claims, denting underwriting margins.

Foreign Exchange and Emerging Markets Debt

In the FX space, El Niño redraws the terms of trade.

- Resilient Currencies: Major commodity-exporting countries with agricultural or mineral surpluses—such as Brazil (BRL), Australia (AUD), and Canada (CAD)—often see their currencies supported by stronger export pricing.

- Vulnerable Currencies: Nations that are net food and energy importers with low foreign exchange reserves are highly exposed. Elevated food import bills strain current account balances, putting downward pressure on local currencies and driving up sovereign bond yields.

Strategic Portfolios and the Geopolitical Overlay

Ultimately, while El Niño is a powerful macroeconomic catalyst, it does not exist in a vacuum. Its primary significance for asset allocators is its role as a compounding tail risk.

Currently, global commodity markets are heavily focused on geopolitical risks, particularly potential energy supply disruptions surrounding the Strait of Hormuz. A severe El Niño occurring simultaneously with an energy shock would create a compounding inflationary effect, as high diesel and fertilizer costs would merge with weather-driven crop failures.

For global macro investors, the single most actionable playbook over the coming months is to closely monitor the cumulative rainfall metrics of the Indian monsoon and the crop progress reports from Southeast Asia. This data will determine whether the current El Niño remains a manageable market disruption or transforms into a historic, tradeable dislocation across the global soft commodities complex.