As the summer sun begins to warm the landscape, millions of Americans will seek the refreshing relief of a cold beer after a long day’s work. Yet, for many, the price tag at the checkout counter—or the cost of a round at the local tavern—is significantly higher than the raw cost of production suggests. While the average consumer may be aware of the federal excise tax, they are likely oblivious to the intricate, multi-layered "hidden" tax structure that makes beer one of the most heavily taxed consumer products in the United States.

The Invisible Ingredient: Why Your Beer Costs More

In the complex alchemy of brewing, the most expensive ingredient is not hops, barley, or water—it is the tax. The tax burden embedded within the final price of a beer often exceeds the combined costs of labor, raw materials, and distribution. Across the nation, various levies, fees, and surcharges can aggregate to account for as much as 40.8 percent of the retail price of a beverage.

This financial reality is largely obscured from the consumer. Unlike a standard retail sales tax, which is explicitly broken out as a line item on a receipt, beer taxes are typically levied at the manufacturer or wholesaler level. These costs are then "baked into" the retail price, meaning the average drinker remains largely unaware that they are paying a significant premium for the privilege of enjoying their beverage of choice.

A Chronology of Fiscal Complexity

The American alcohol tax landscape is a legacy system, built upon decades of shifting legislative priorities, post-Prohibition regulatory frameworks, and regional economic needs.

- The Post-Prohibition Era: Following the repeal of the 18th Amendment, the federal government established the current excise tax structure to both regulate the industry and generate reliable, albeit volatile, revenue.

- The Rise of Tiered Taxation: Over the decades, states began introducing their own excise taxes, leading to a patchwork of regulations. By the late 20th century, states began differentiating between domestic and imported products, and eventually between different alcohol-by-volume (ABV) levels.

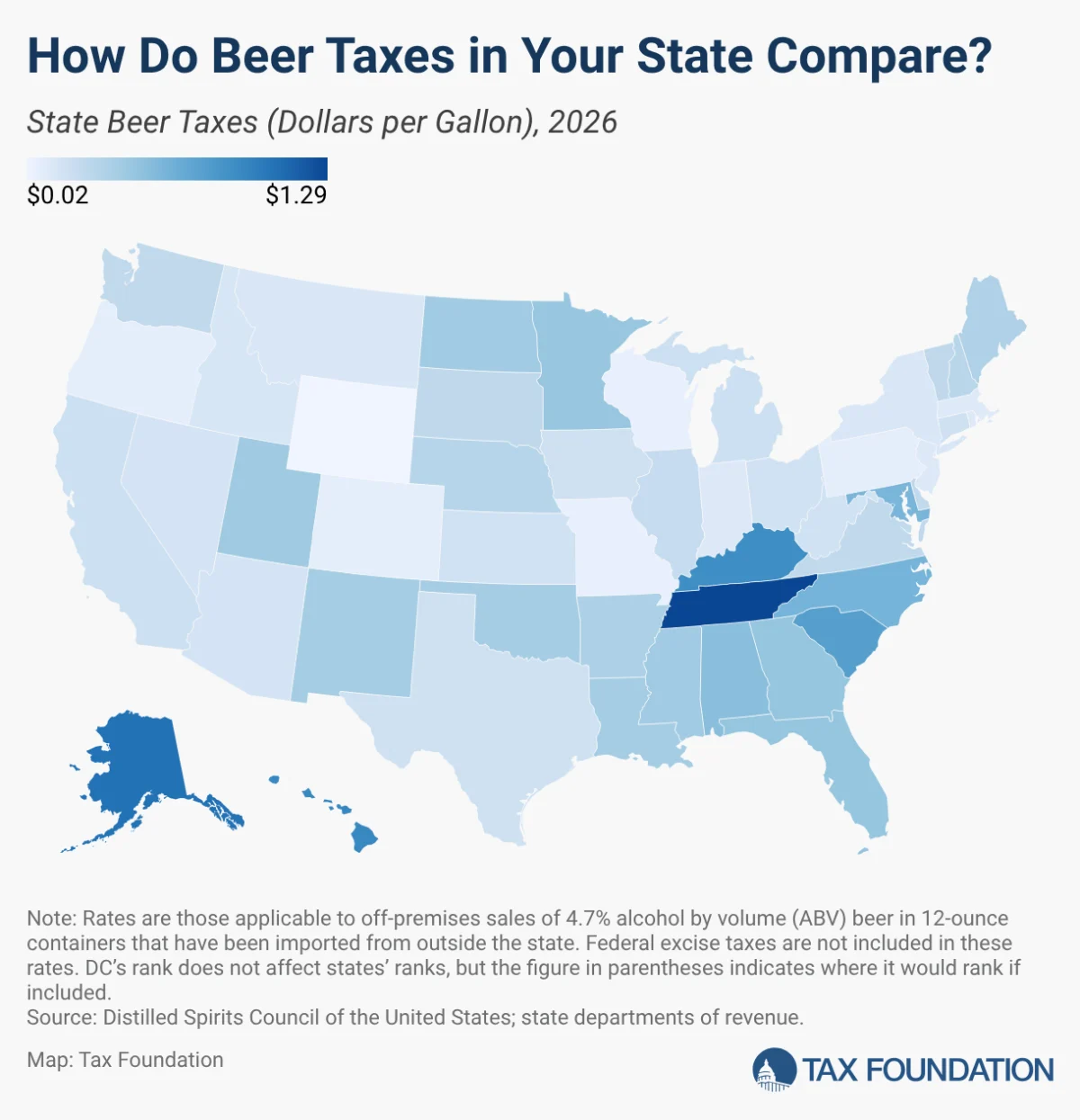

- Modern Regulatory Shifts: In recent years, several states have moved to modernize these codes. For example, Missouri’s recent legislative efforts to cut taxes on beer manufactured within state borders to just $0.02 per gallon highlight a modern trend of using tax policy as a tool for economic development and local industry protection.

- The Future Outlook (2026 and Beyond): As we move toward 2026, the industry faces mounting pressure from inflation and changing consumption habits. Policymakers are increasingly tasked with balancing the need for revenue against the desire to support local craft breweries, which often struggle under the weight of the same regulations designed for massive industrial producers.

Supporting Data: The Great Divide

The variance in beer taxation across the 50 states is staggering, creating a landscape of "tax havens" and "tax traps" for the brewing industry.

According to data analyzed by the Tax Foundation, the disparities are stark. At the high end of the spectrum, Tennessee leads the nation with a tax burden of $1.287 per gallon. Alaska follows closely at $1.07, and Hawaii rounds out the top three at $0.93. These figures often reflect the high costs of logistics and local government funding needs in those jurisdictions.

Conversely, the lowest tax burdens are found in states with robust, historic brewing cultures. Wyoming leads the nation in affordability at $0.019 per gallon, followed by Missouri and Wisconsin at $0.06 and $0.065, respectively. These states often view their beer industries as vital cultural and economic pillars, opting for lower tax rates to encourage volume and competitive pricing.

The Impact of Localized Levies

It is important to note that state-level data often masks additional local burdens. In the Municipality of Anchorage, for instance, a local sales tax on alcohol adds an extra 5 percent to the cost of a purchase. Similarly, states like Alabama and Georgia utilize statewide uniform local taxes that add roughly 50 cents per gallon to the cost of beer. When these local, municipal, and county-level taxes are combined with federal and state excise duties, the true fiscal burden becomes a moving target that varies from one street corner to the next.

Regulatory Nuance: ABV and Product Classification

The administrative burden of beer taxation is further complicated by the way states classify alcoholic beverages. In 16 states, the tax rate is not a flat fee but is instead contingent on a variety of factors, including:

- Alcohol by Volume (ABV): Idaho, for example, treats beer with more than 5 percent ABV as wine, effectively tripling the tax rate from $0.15 to $0.45 per gallon.

- Container Size: Virginia utilizes a complex sliding scale, applying different tax rates to containers smaller than 7 ounces, those up to 12 ounces, and those exceeding 12 ounces.

- Place of Production: Taxes often favor local manufacturing, creating an uneven playing field for imported or out-of-state brands.

This rigid categorical system—which separates beer, wine, and spirits into distinct legal buckets—is increasingly viewed by economists as obsolete. Modern brewing, which often involves cross-category innovation (such as hard seltzers or spirit-infused ales), frequently runs into roadblocks where the product is taxed in a way that is disconnected from its actual alcohol content.

Implications for the Industry and Consumers

The current system of beer taxation carries significant risks for both the public and private sectors. For the brewing industry, the challenges are mounting. Beyond the "hidden" taxes, the sector is grappling with the rising costs of tariffs on imported raw materials and a broader shift in consumer behavior. Younger demographics are increasingly pivoting toward low- or no-alcohol alternatives, a trend that threatens the tax base for states that have come to rely on beer excise taxes to fund general government services.

The Danger of Fiscal Over-Reliance

For policymakers, relying on alcohol taxes to fill budget gaps is a precarious strategy. Unlike property or income taxes, which are relatively stable, excise taxes on consumer goods are subject to significant volatility. When consumer trends shift away from a specific product, or when economic downturns lead to reduced discretionary spending, the revenue streams tied to beer sales can evaporate, leaving states with unforeseen budget deficits.

The Case for Modernization

The consensus among tax policy experts is that the current arcane system requires a fundamental overhaul. A shift toward a neutral, ABV-based taxation model would offer several benefits:

- Simplicity: A uniform tax based on alcohol content would remove the administrative complexity of managing disparate categories for beer, wine, and spirits.

- Neutrality: It would eliminate the current market distortions where products are taxed based on their label rather than their actual composition.

- Adaptability: A system based on alcohol content would naturally accommodate industry innovation, ensuring that new products are taxed fairly without requiring constant legislative intervention.

Conclusion: A Toast to Transparency

As the industry and consumer preferences continue to evolve, the necessity for a clearer, more rational tax framework becomes undeniable. For the American consumer, the next time they enjoy a pint, they are participating in a complex economic transaction that has been shaped by over a century of legislative negotiation.

Whether the goal is to protect local craft brewers, ensure state budget stability, or simply lower the cost of a summer luxury, the path forward requires a transition away from the "hidden" tax model. By modernizing these outdated categorical systems and moving toward a more transparent, ABV-focused approach, policymakers can create a more predictable and equitable environment for one of America’s most cherished cultural pastimes. Until then, the hidden cost of the pint remains an invisible companion to every drink raised in celebration.