In the modern financial landscape, the primary adversary of long-term prosperity is not a lack of income or poor investment choices—it is human fallibility. Financial planners and behavioral economists have long observed a recurring pattern: even the most well-intentioned individuals often see their wealth-building efforts derailed by the mundane frictions of daily life. A busy schedule, a momentary lapse in memory, or the psychological tax of making recurring decisions can dismantle months of careful budgeting.

The solution, increasingly championed by financial experts, is the "Automated Financial Architecture." By shifting the burden of fiscal management from human willpower to algorithmic precision, individuals can effectively turn good intentions into guaranteed, measurable outcomes.

The Psychology of Financial Fatigue

Most financial plans do not collapse due to complex mathematical errors; they fail on a random Tuesday when a transfer is forgotten or a bill goes unpaid. This phenomenon is rooted in what psychologists call "decision fatigue." Every manual transfer—moving money from a checking account to a high-yield savings account or allocating funds to an IRA—is a cognitive event. Each decision requires a deliberate expenditure of mental energy.

When you rely on discipline to manage your finances, you are setting yourself up for a test that you must retake every single time you are paid. Willpower is a finite resource; when you are exhausted, stressed, or distracted, your ability to make prudent financial choices diminishes. Conversely, automation removes the decision entirely. When a transfer is automated, it happens whether you are motivated, exhausted, or simply busy. By removing the "choice" to save, you effectively make saving your default behavior, while spending becomes the secondary, conscious action.

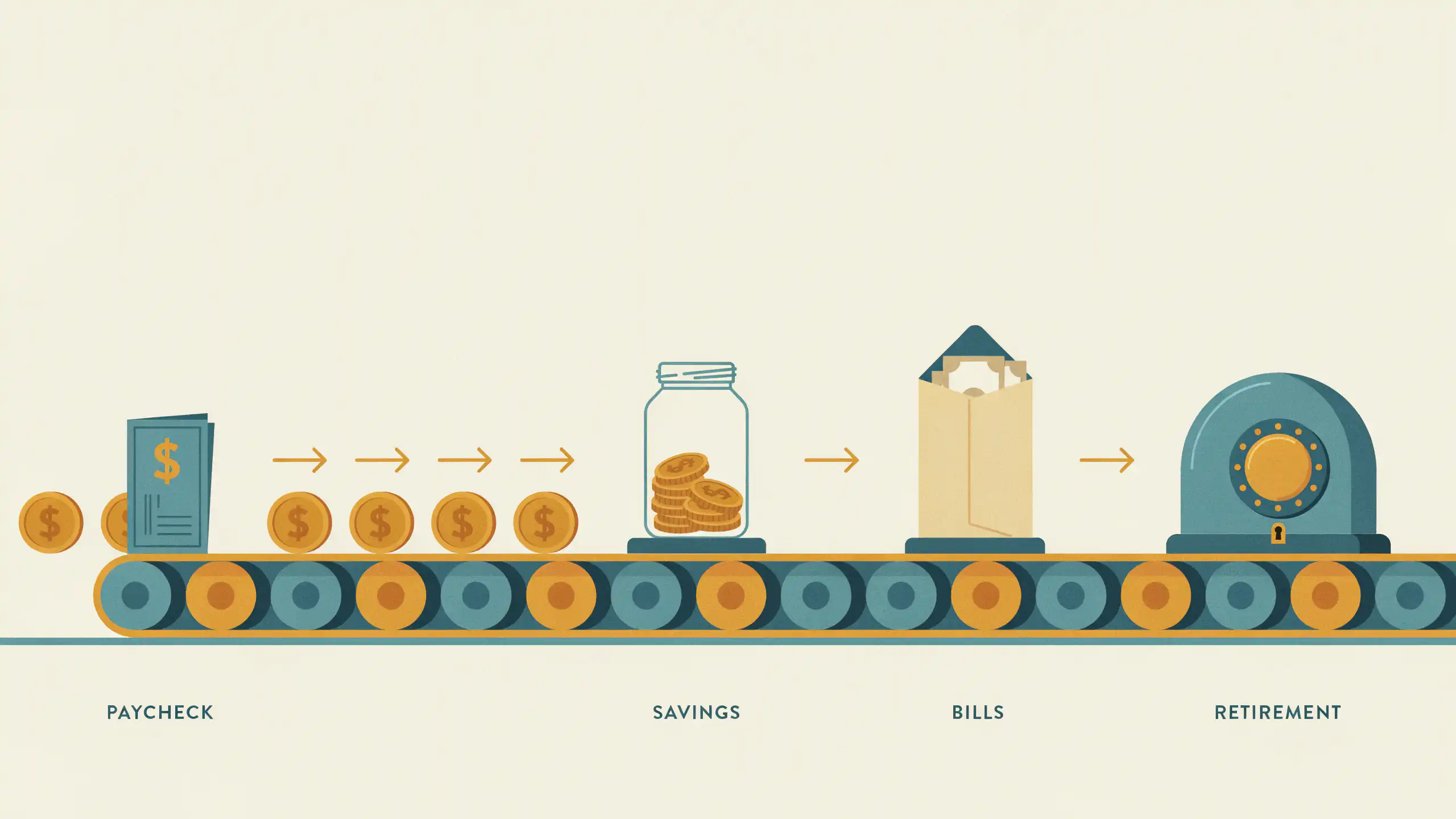

The Chronology of Automation: A Step-by-Step Implementation

Transitioning to a fully automated financial system requires an initial investment of time—perhaps ten minutes in your banking portal—but it pays dividends in the form of time saved and wealth accumulated. To build an effective system, one must follow a strategic sequence of operations:

Phase 1: The Foundation (Current Accounts)

The first step is auditing your current cash flow. Identify your primary income date and your recurring fixed expenses. Automation works best when it is synchronized with your paycheck. By scheduling transfers to occur within 24 to 48 hours of your salary deposit, you ensure that money is moved before it feels "available" for discretionary spending. This mimics the psychological success of payroll deductions, where retirement contributions are removed before they ever reach your checking account.

Phase 2: The Infrastructure (The Three Pillars)

Most experts agree that three core automations cover 90% of your financial life:

- Savings Contributions: Set up recurring transfers to a dedicated emergency fund.

- Debt Repayment: Schedule automatic payments for all fixed-rate debt, such as mortgages or student loans, to ensure you never miss a payment and avoid unnecessary interest penalties.

- Retirement Contributions: Utilize automated investment plans (such as 401(k) contributions or automated IRA deposits) to ensure your long-term growth remains consistent regardless of market volatility.

Phase 3: The Maintenance (Quarterly Reviews)

Automation is not abandonment. It is a system that requires periodic calibration. Every three months, schedule a brief review to ensure that your automatic transfers still align with your current income and long-term goals. If your salary increases, your automated contribution amounts should be scaled upward accordingly.

Supporting Data: Why "Set It and Forget It" Wins

Behavioral studies consistently demonstrate that individuals who automate their savings are significantly more likely to reach their retirement goals than those who rely on manual transfers. According to data from various retirement research institutes, employees who are auto-enrolled in retirement plans—meaning they must "opt-out" rather than "opt-in"—have participation rates upwards of 90%.

The math is simple: compound interest is the greatest wealth-building tool available, but it requires consistency. By automating, you prevent the "gaps" in savings that occur when a person forgets to make a transfer for a month or two. Over a thirty-year career, these missed months can result in tens of thousands of dollars in lost potential earnings due to the loss of compounding time.

Implications for Personal Finance

The broader implication of this shift is the democratization of wealth management. In the past, managing complex finances was the domain of those who had the time to obsess over spreadsheets or the money to hire a dedicated professional. Today, banking applications and digital finance tools have lowered the barrier to entry, allowing anyone with a smartphone to build an institutional-grade financial system.

However, there is a caveat: the "buffer" strategy. When automating, it is crucial to maintain a modest cushion in your primary checking account. This buffer accounts for timing discrepancies between automated withdrawals and income deposits, preventing accidental overdrafts. Without this safety net, the system can become a source of stress rather than a source of stability.

Expert Consensus and Professional Perspectives

Financial planners often emphasize that the goal of automation is to lower the "friction" of financial growth. In an interview regarding modern wealth management, several industry experts noted that the most successful clients are those who are "bored" with their finances.

"If you are checking your accounts daily and agonizing over every transaction, you are likely doing it wrong," says one veteran financial advisor. "The most effective investors are those who build a robust, automated system and only look at their accounts during their quarterly check-ins. When the system works, the need for constant vigilance disappears."

Overcoming the "Default Bias"

The human brain is wired to prefer the path of least resistance. This is known as "default bias." By making savings the default, you leverage this human tendency for your own benefit. When the money leaves your account before you have the chance to perceive it as spendable income, your lifestyle naturally adjusts to the remaining balance. This is often referred to as "paying yourself first."

Conversely, if you wait until the end of the month to "save what is left," you are relying on the assumption that there will be a surplus. In reality, modern consumer culture is designed to fill any available surplus with expenses. Automation flips this dynamic, forcing you to prioritize your future self over your present impulses.

Conclusion: Take Control Tonight

The transition from a manual, willpower-based financial life to an automated, system-based one is the single most effective move you can make for your long-term economic health. It requires no specialized education, no massive initial capital, and no daily effort.

Spend ten minutes in your banking app tonight. Set your automatic transfers, align them with your payday, and set a calendar alert for a quarterly review. By removing the need for constant, disciplined decision-making, you are not just saving money—you are purchasing peace of mind. In the end, the most sophisticated financial plan is the one that works while you sleep, ensuring that your wealth continues to grow, regardless of whether you remember to check the balance.