Whether you are a seasoned sommelier curating a high-end cellar or a casual enthusiast picking up a bottle for dinner, the price at the register often conceals a sophisticated web of fiscal policy. Behind every glass of wine lies a complex layer of excise taxes that vary wildly depending on your geography. As of 2025, the wine industry continues to be a vital pillar of the global economy, yet it remains burdened by an arcane, fragmented system of state and federal levies that often defies economic logic.

The Economic Weight of the Grape

The wine market has maintained a remarkable consistency in its share of the alcoholic beverage industry since the turn of the millennium. It is not merely a lifestyle product; it is a significant generator of economic value, supporting agriculture, logistics, retail, and tourism. However, this sector is uniquely burdened by excise taxes that transcend standard corporate and sales levies.

In 2025, the total estimated consumption tax paid on wine in the United States is projected to hit $7.2 billion. This figure represents a substantial transfer of wealth from consumers and producers to state and federal coffers. While these taxes are often marketed as regulatory fees or public health safeguards, their structure is frequently criticized for being outdated, inconsistent, and disconnected from the realities of modern manufacturing and consumption.

Chronology and Evolution of Alcohol Policy

To understand the current tax landscape, one must look at how alcohol regulation has evolved. Following the repeal of Prohibition, states were granted significant latitude in how they govern the sale and taxation of alcohol. This resulted in the "three-tier system" (producer, distributor, retailer) that dominates the U.S. market today.

Since 2021, the landscape has seen subtle but impactful shifts. While many states have maintained static ad quantum (volume-based) taxes, the rise of "Ready-to-Drink" (RTD) wine cocktails has forced legislators to scramble. Many of these products exist in a regulatory gray area, leading to instances of "tax creep" where products are pushed into higher tax brackets intended for distilled spirits, despite having significantly lower alcohol by volume (ABV).

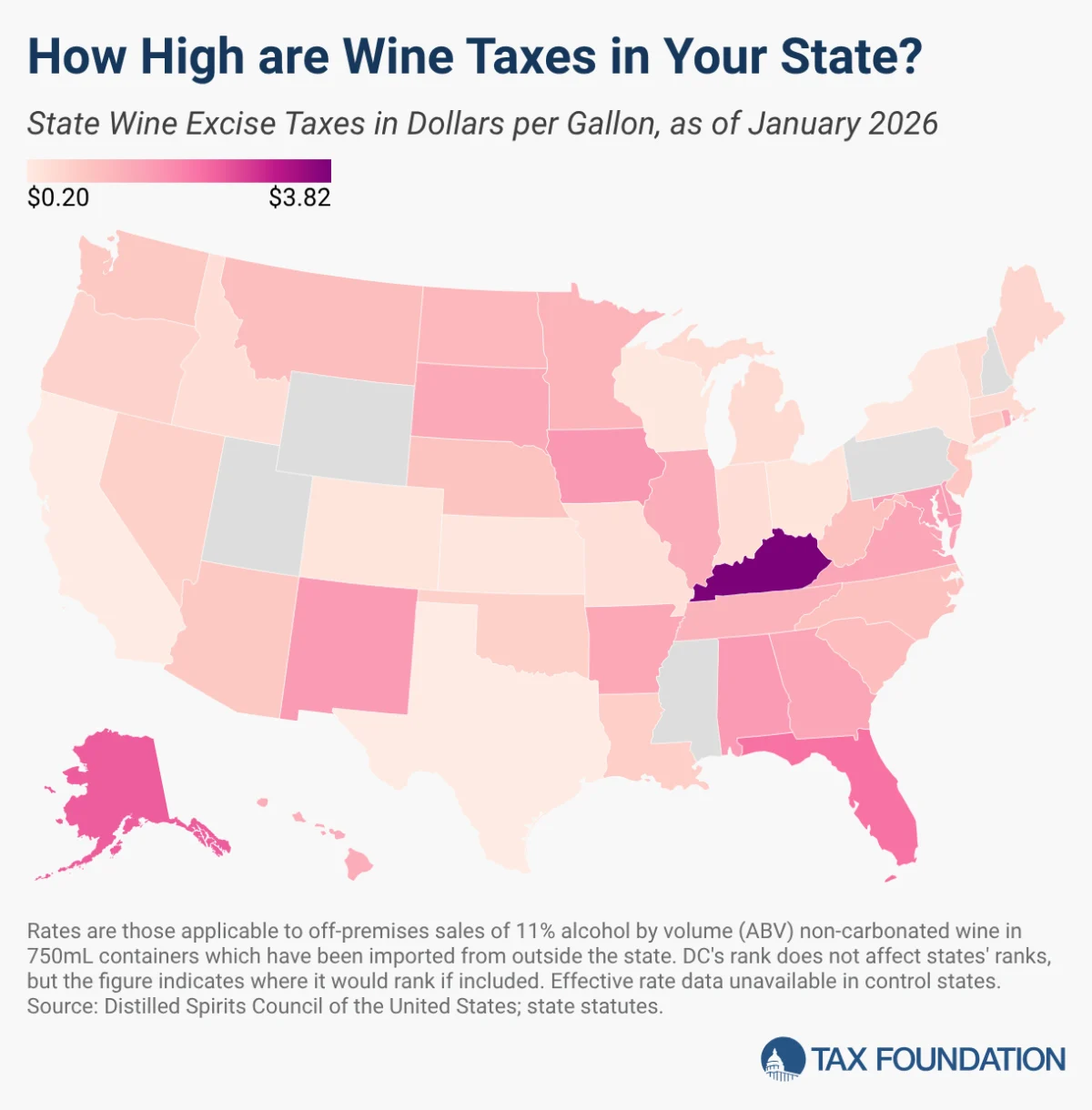

A State-by-State Breakdown: The Tax Disparity

The discrepancy in tax burdens across state lines is stark. Because states generally tax wine at a higher rate than beer but lower than spirits, they often attempt to position wine as a "middle ground" beverage. However, when adjusted for actual alcohol content, the logic often collapses.

The Heavy Hitters

Kentucky currently holds the title for the most expensive wine tax environment in the nation, levying a burden of $3.82 per gallon. This is largely driven by a 10 percent wholesale tax that compounds the base excise rate. Following Kentucky, the most expensive states for wine drinkers include:

- Alaska: $2.50 per gallon

- Florida: $2.25 per gallon

- Iowa: $1.75 per gallon

The Favorable Climates

On the opposite end of the spectrum, California—the heart of the U.S. wine industry—offers the lowest tax burden in the country at just $0.20 per gallon. This low-tax environment is often credited with fostering the massive economic growth of the Napa and Sonoma wine regions. Other states with relatively low tax burdens include:

- Texas: $0.204 per gallon

- Wisconsin: $0.25 per gallon

- Kansas & New York: $0.30 per gallon

The "Control State" Dilemma

While most states operate under a licensing system, five states—Mississippi, New Hampshire, Pennsylvania, Utah, and Wyoming—maintain government monopolies over the sale of alcohol. In these jurisdictions, "tax" is a misleading metric because the state effectively sets the price.

- Utah: Mandates a minimum markup of 88.5 percent, acting as a massive, non-transparent tax on the consumer.

- Pennsylvania: The Liquor Control Board has broad authority to manipulate prices, with net margins reported around 5.3 percent, alongside an additional 18 percent tax on spirits that often bleeds into the broader regulatory perception of alcohol pricing.

- New Hampshire: Interestingly, the state’s liquor commission prides itself on lower effective taxes (averaging $0.046 per gallon) to encourage cross-border shopping, effectively using low alcohol prices as an economic development tool.

Supporting Data: The Hidden Fees and Commissions

Beyond standard excise taxes, seven states (Colorado, Idaho, Iowa, Missouri, Oregon, Ohio, and Washington) impose specific levies to fund "Wine Commissions" or "Agricultural Development Funds." In these states, the average consumer is unknowingly subsidizing the marketing and lobbying efforts of local viticultural associations.

Furthermore, at the federal level, the tax structure is equally complex. The federal excise tax for 11 percent ABV still wine is $1.07 per gallon. While there are tiered tax credits available for smaller domestic producers (covering the first 30,000 to 750,000 gallons), these credits are often difficult to navigate, creating a barrier to entry for boutique wineries that lack the administrative resources to manage complex tax filings.

Implications: The Case for Modernization

The current categorical structure of alcohol taxation is increasingly viewed as an artifact of the 20th century. As the market pivots toward low-alcohol wines, canned wine spritzers, and complex hybrids, the rigid definitions of "wine" versus "spirits" lead to frequent misclassifications.

The Argument for ABV-Based Taxation

The most prominent recommendation from tax policy experts—such as those at the Tax Foundation—is to transition toward a neutral, ABV-based taxation model. By taxing the product according to the actual alcohol content rather than the container size or the categorical label, the system would achieve three goals:

- Neutrality: It eliminates the bias toward specific types of alcohol, allowing the market to dictate winners based on quality rather than tax-avoidance strategies.

- Simplicity: It removes the need for arcane definitions and constant legislative updates to accommodate new product types like RTD cocktails.

- Inflation Resistance: Unlike ad quantum taxes, which lose value as the currency debases over time, an ABV-based percentage system can be structured to maintain a more consistent real-value revenue stream for the state.

The Risk of Revenue Volatility

Policymakers must be wary of relying on alcohol taxes as a primary revenue stream. Ad valorem taxes (taxes based on the assessed value) are notoriously volatile. During economic downturns, consumers tend to trade down to cheaper, lower-margin products, causing tax revenues to crater. Conversely, tariffs and trade wars, such as those seen in recent years, can cause sudden spikes in costs that suppress the industry, making it an unreliable foundation for general government funding.

Conclusion: A Call for Transparency

For the casual consumer, the price of a bottle of wine is a combination of production costs, logistics, marketing, and the "invisible" layer of government revenue collection. As the industry continues to evolve, the disconnect between modern consumption habits and Prohibition-era tax structures will only grow.

If the goal of state and federal policy is to provide a fair, simple, and efficient tax system, the current approach of disparate, categorical, and often punitive excise taxes falls short. Modernizing the system to tax based on alcohol content would not only simplify compliance for businesses but would also bring transparency to the consumer. Until then, the taxman remains the silent partner at every dinner table, taking his cut long before the first cork is pulled.

Whether the political will exists to dismantle these entrenched, state-specific revenue silos remains to be seen. However, as the wine industry faces new challenges from global competition and shifting consumer demographics, the need for a tax system that reflects the 21st-century reality is more pressing than ever.