In the modern financial landscape, the difference between prosperity and perpetual struggle often comes down to a single, overlooked variable: the "unassigned dollar." For millions of households, budgeting is a reactive, imprecise science. Expenses are paid, savings are treated as an afterthought, and the remaining balance is left to drift into a murky pool of discretionary spending—a psychological loophole that leads directly to "lifestyle creep" and financial anxiety.

Zero-based budgeting (ZBB) offers a radical, mathematically precise alternative. By forcing every single unit of currency to account for its purpose before the month even begins, ZBB eliminates the ambiguity that drains bank accounts. This guide explores the mechanics, the psychology, and the long-term implications of implementing a zero-based financial strategy.

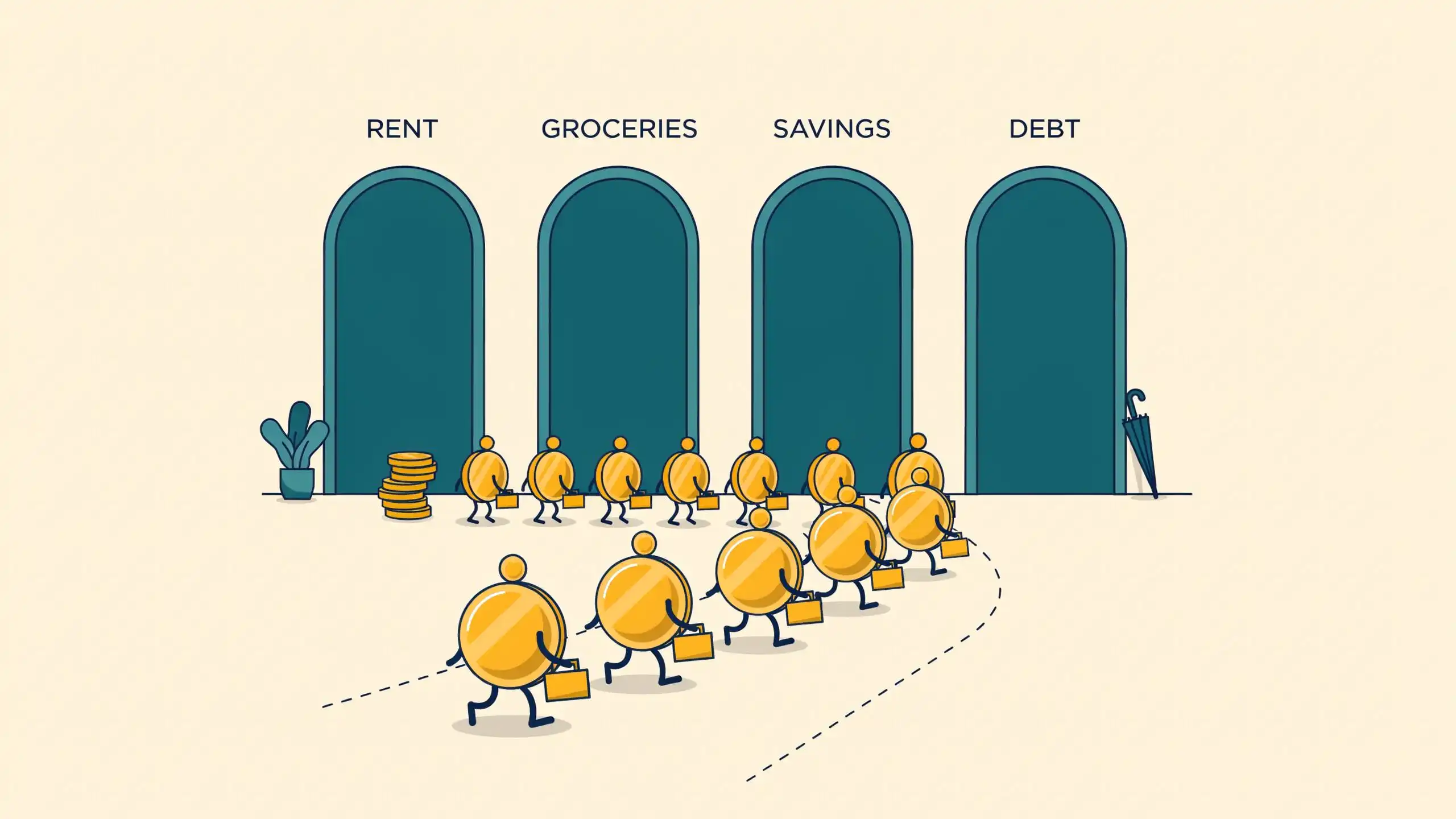

The Philosophy of "Every Dollar Has a Job"

At its core, zero-based budgeting is a simple equation: Income – Expenses = $0.

Unlike traditional budgeting methods that focus on tracking what has already been spent, ZBB is inherently proactive. It dictates that every dollar of your monthly income must be assigned to a specific category—whether that category is rent, retirement contributions, debt repayment, or even a "fun money" buffer.

The term "zero" in this context does not mean you are spending all your money to reach a zero balance in your bank account. Rather, it means that by the time you have finished your planning, you have allocated your entire income toward specific, purposeful destinations. Savings, investments, and aggressive debt payments are treated with the same urgency as fixed expenses like utilities or insurance. By giving every dollar a "job," you prevent money from sitting idle, where it is inevitably tempted by impulse purchases and unplanned consumerism.

The Chronology of Implementation: A Step-by-Step Approach

Transitioning to a zero-based budget requires a shift in mindset and a structured workflow. The following chronology outlines how to successfully initiate and maintain this system.

Phase 1: Pre-Month Preparation

The most critical work of a zero-based budget happens before the month begins.

- Calculate Income: Tally your expected take-home pay. If you have an irregular income, use the income from the previous month or a conservative average.

- List All Categories: Categorize every expected expenditure. This includes fixed costs (mortgage/rent, utilities, insurance), variable costs (groceries, fuel, entertainment), and financial goals (emergency fund contributions, brokerage investments).

- Assign Values: Allocate specific dollar amounts to each category until your total income is depleted.

- The "Miscellaneous" Safety Valve: Always include a small, dedicated line item for unforeseen expenses. This prevents the entire budget from collapsing when a minor, unexpected cost arises.

Phase 2: Execution and Tracking

As the month progresses, the budget acts as a living document. Tracking is not about restriction; it is about accountability. When you realize that groceries are trending over budget, the zero-based method requires you to reallocate funds from another category—perhaps "entertainment"—to cover the gap. This "robbing Peter to pay Paul" mechanic is not a sign of failure; it is the system working as intended. It forces you to make active trade-offs, ensuring that your spending aligns with your current priorities.

Phase 3: The Mid-Month Adjustment

For those paid bi-weekly, the process is iterative. You build your budget based on the paychecks you expect to receive. When each paycheck hits your account, you assign those specific dollars to the categories that need funding first. By the end of the month, your inflow matches your outflow exactly.

Supporting Data: Why "Save What’s Left" Fails

Behavioral economics consistently demonstrates that the "save what’s left" approach is fundamentally flawed. When individuals wait until the end of the month to save, they are subject to the "Parkinson’s Law of Finance"—expenditures rise to meet income. If there is money sitting in a checking account, the brain perceives it as "disposable," regardless of long-term goals.

Data suggests that individuals who utilize zero-based budgeting or similar "envelope-style" systems report lower levels of financial stress and higher rates of debt reduction. By prioritizing savings and debt repayment at the start of the month, these individuals remove the competition between immediate gratification and long-term security. The money is gone before it has a chance to be spent on non-essentials.

Expert Perspectives: The Psychology of Constraints

Financial experts argue that the primary benefit of ZBB is not just the math, but the cognitive load reduction. "When you make decisions in advance, you eliminate the need for willpower in the moment," says one prominent financial advisor.

The "official" stance among personal finance advocates is that most people overspend because they lack a clear roadmap. Without a destination for every dollar, money defaults to the path of least resistance: consumption. ZBB forces a moment of reflection. When you have to choose between a new streaming service and an extra contribution to your emergency fund, you are forced to reconcile your spending with your values.

Implications for Financial Health

The implications of adopting a zero-based budget are profound, particularly for those looking to accelerate their journey toward financial independence.

1. Elimination of Financial "Leaks"

Most households have "leaks"—unnoticed subscriptions, recurring fees, or daily habits that aggregate into hundreds of dollars of lost potential. ZBB plugs these holes by requiring a review of every category every month.

2. Accelerated Debt Payoff

By assigning a specific amount of money to debt reduction every month, the repayment process becomes a fixed expense. This creates momentum, turning the psychological burden of debt into a scheduled, manageable line item.

3. Increased Intentionality

The most significant long-term impact is the shift in how one views money. When every dollar is assigned a job, you become more conscious of the cost-benefit analysis of every purchase. You aren’t just "spending"; you are deciding whether a purchase is worth the opportunity cost of the money you would have otherwise invested or saved.

Tools and Technology: Choosing Your Medium

While the method is ancient, the execution has been modernized.

- The Traditionalists: Many still prefer the pen-and-paper or spreadsheet method. The manual entry process provides a tactile connection to the numbers, which can increase the psychological impact of the spending.

- The Modern Automators: A variety of budgeting applications are designed specifically for zero-based budgeting. These apps sync with bank accounts, categorize transactions, and alert users when a category is reaching its limit, effectively automating the "math" part of the process while leaving the decision-making to the user.

Conclusion: The Power of Purpose

Zero-based budgeting is not a "quick fix" for poverty, nor is it a magic wand for instant wealth. It is a discipline. It requires the effort to plan, the honesty to track, and the humility to adjust. However, for those who commit to the process, it offers a level of control that few other financial strategies can match.

By ensuring that every dollar has a job, you move from being a passenger in your financial life to the driver. You stop wondering where your money went and start directing where it goes. In a world of infinite spending temptations, that clarity is the ultimate competitive advantage. Whether you are aiming to pay off student loans, build a six-month emergency fund, or save for a home, the path forward is clear: define your categories, assign your dollars, and start the month with a plan.

As the old adage in the financial community goes: "A dollar without a job finds one on its own, and it rarely picks the one you would have chosen." Choose the jobs for your dollars today, and watch your financial future transform from a series of accidents into a calculated, successful reality.