In the urgent global endeavor to mitigate climate change, European nations have emerged as the primary laboratory for environmental fiscal policy. Through a complex interplay of carbon taxes, emissions trading systems (ETS), and regulatory frameworks, the continent is attempting to decouple economic growth from greenhouse gas emissions. While the objective—decarbonization—is unified, the methods employed across Europe reveal a stark divergence in strategy, pricing, and effectiveness.

Main Facts: The Evolution of European Carbon Pricing

The concept of "pricing carbon" is rooted in the economic principle of internalization: by assigning a financial cost to the negative externalities of greenhouse gas emissions, governments aim to incentivize businesses and consumers to shift toward cleaner energy sources.

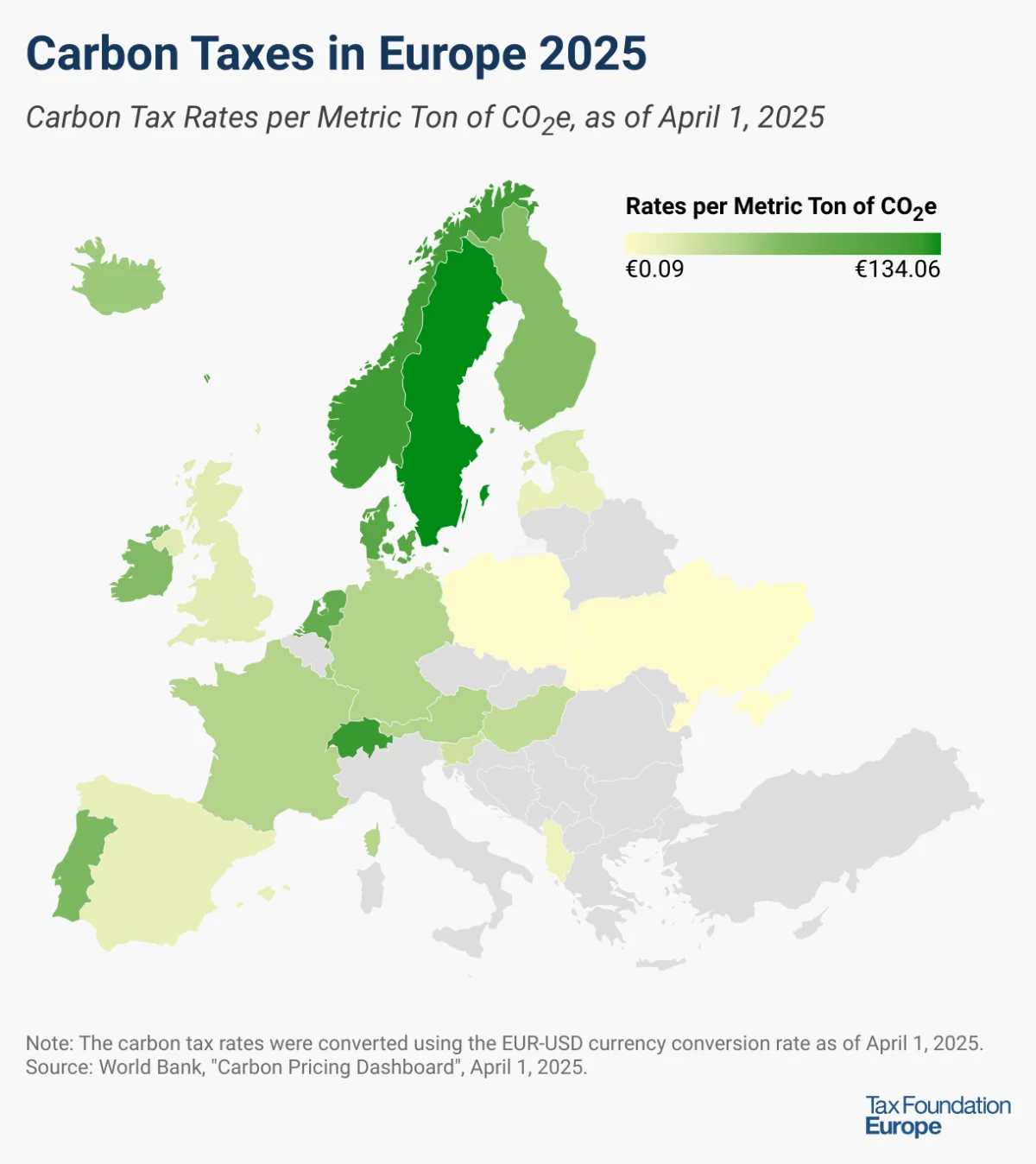

Finland pioneered this approach in 1990, becoming the first country globally to implement a carbon tax. Since that inaugural move, the practice has proliferated across the continent. Today, 24 European countries have institutionalized carbon taxes, though the definition and implementation of these taxes vary wildly.

A carbon tax is fundamentally a levy on the carbon content of fossil fuels, though it may extend to other greenhouse gases like methane. By placing a price on these emissions, governments hope to force a behavioral shift. However, the efficacy of these taxes depends heavily on their scope. For instance, while some nations cover the majority of their greenhouse gas emissions, others—like Spain—maintain narrow tax bases that target specific sectors, such as fluorinated gases, effectively covering only a fraction of their total national output.

Chronology: A Multi-Decadal Transformation

The trajectory of carbon pricing in Europe has moved from experimental policy to a cornerstone of economic strategy.

- 1990: Finland sets the global standard by introducing the first national carbon tax.

- 2005: The European Union launches the EU Emissions Trading System (EU ETS), a "cap-and-trade" market that limits the total volume of greenhouse gases companies can emit.

- 2020: Switzerland successfully links its national ETS to the EU ETS, signaling a trend toward cross-border market integration.

- 2021: The United Kingdom establishes the UK ETS following its withdrawal from the European Union, demonstrating a desire to maintain rigorous carbon pricing standards despite political decoupling.

- 2021–2022: Germany and Austria enter the fray, implementing national carbon taxes to bridge the gap toward broader European climate goals.

- 2026: As of April 1, 2026, the average carbon tax rate among the 24 European countries stood at €53.63 per metric ton. This year also saw Serbia introduce a new national carbon tax, further expanding the reach of climate-conscious fiscal policy.

Supporting Data: The Price Gap and Coverage Disparity

The economic burden of carbon emissions in Europe is far from uniform. The disparity between the highest and lowest tax rates highlights the lack of a singular "European" approach.

The Pricing Spectrum

As of 2026, Norway maintains the most aggressive stance, levying a carbon tax of €146.23 ($169.71) per metric ton. Sweden follows closely at €133.17 ($154.55), while Switzerland and Liechtenstein maintain rates of €129.09 ($149.81). At the other end of the spectrum, the tax environments in Poland and Ukraine are largely symbolic, with rates of €0.09 and €0.59 per ton, respectively.

This variance suggests that while the "intent" to tax carbon is widespread, the political appetite to impose high costs on industry and consumers remains localized and sensitive to domestic economic conditions.

The Challenge of Coverage

The "collection efficiency" of these taxes is often compromised by exemptions and narrow definitions. While countries like Albania, Andorra, and Luxembourg theoretically cover over 70% of their greenhouse gas emissions, the reality of tax administration—riddled with rebates and sector-specific exclusions—often leaves the actual coverage significantly lower. Spain serves as a cautionary tale; by focusing its tax primarily on fluorinated gases, the system influences only 2% of the country’s total emissions profile.

Implications: The Risks of Double Taxation and Market Shifts

The integration of national carbon taxes with the supranational EU ETS has created a complex regulatory environment that often leads to unintended consequences.

The Problem of Double Taxation

Several nations, including France, Ireland, the Netherlands, and Portugal, have allowed their national carbon tax bases to overlap with the sectors already regulated under the EU ETS. This results in "double taxation"—a scenario where the same unit of carbon is effectively taxed twice. Economists argue that this is not only administratively inefficient but can also distort market signals.

The "Leakage" Effect

Perhaps more concerning is the tendency for national carbon taxes to shift emissions rather than eliminate them. When a domestic tax makes production expensive within a specific country, firms may shift their operations or source their energy from outside the tax base. Because the EU ETS caps the total number of allowances across the bloc, these domestic-level taxes often fail to reduce total net emissions. Instead, they simply redistribute where those emissions occur, often leading to industrial flight or "carbon leakage" to jurisdictions with lower regulatory hurdles.

Official Responses and Future Outlook

The European Commission is acutely aware of the limitations of the current fragmented system. The proposed EU ETS-2 represents the next phase of European climate policy, intended to cover sectors like buildings and road transport that were previously excluded or inconsistently taxed.

Germany’s decision to phase its national carbon tax into a national ETS—with a view to eventually sunsetting these in favor of the broader EU ETS-2—serves as a blueprint for the future. By aligning national policies with a pan-European mechanism, the EU hopes to create a unified price for carbon that prevents double taxation and ensures a more efficient, transparent market.

Meanwhile, other nations continue to experiment. Turkey is currently exploring the implementation of a national ETS, signaling that the European model of carbon pricing is increasingly influential beyond the formal borders of the European Union.

The Ideal Model

The ideal, as advocated by many tax policy experts, is a broad-based, uniform tax applied to all sectors. A narrow tax base is inherently non-neutral and inefficient, increasing the costs of administration while failing to capture the full scope of economic activity. By moving toward a "single price" system, policymakers hope to minimize the administrative burden on businesses and provide a consistent signal that makes green investment the most rational economic choice.

Conclusion: The Long Road to Decarbonization

The European experience with carbon taxation proves that while fiscal policy is a potent tool for environmental management, it is not a silver bullet. The success of these initiatives rests not on the sheer number of taxes implemented, but on the design, administration, and integration of these systems.

As Europe moves toward 2030, the focus will likely shift from the introduction of new taxes to the harmonization of existing ones. The goal is to evolve from a patchwork of national levies into a coherent, continent-wide market that treats carbon as a quantifiable, tradable, and—ultimately—avoidable cost of business. For the rest of the world, the European laboratory continues to offer critical lessons in the delicate balance between environmental ambition and economic stability.

Stay informed on the tax policies impacting you. Subscribe to receive expert insights and policy analysis delivered straight to your inbox. Subscribe here.