A high-stakes confrontation is brewing between the White House and the Federal Reserve. Financial markets are increasingly pricing in an aggressive, politically sensitive trajectory for monetary policy that directly threatens the economic narrative of the sitting administration.

Despite the long-held "conventional wisdom" that the Federal Reserve avoids making major policy shifts—particularly interest rate hikes—in the immediate run-up to a presidential election, stubborn inflation data has forced a dramatic repricing of market expectations. According to the latest interest rate futures, there is now a net 70.4 percent probability that the Federal Reserve will raise interest rates at least once before voters head to the polls in November.

This hawkish turn comes at a time when President Donald Trump has made his expectations clear: he expects Fed Chair Kevin Warsh to deliver rate cuts, not hikes, to stimulate economic growth. The divergence between executive expectations and macroeconomic reality has set the stage for unprecedented institutional friction.

Main Facts: The Brewing Central Bank Conflict

At the heart of the current financial volatility is a fundamental disconnect between political desires and macroeconomic data. The Federal Reserve, tasked with maintaining price stability and maximum employment, is facing an inflation rate that remains stubbornly double its official 2.0 percent target.

The primary conflict points include:

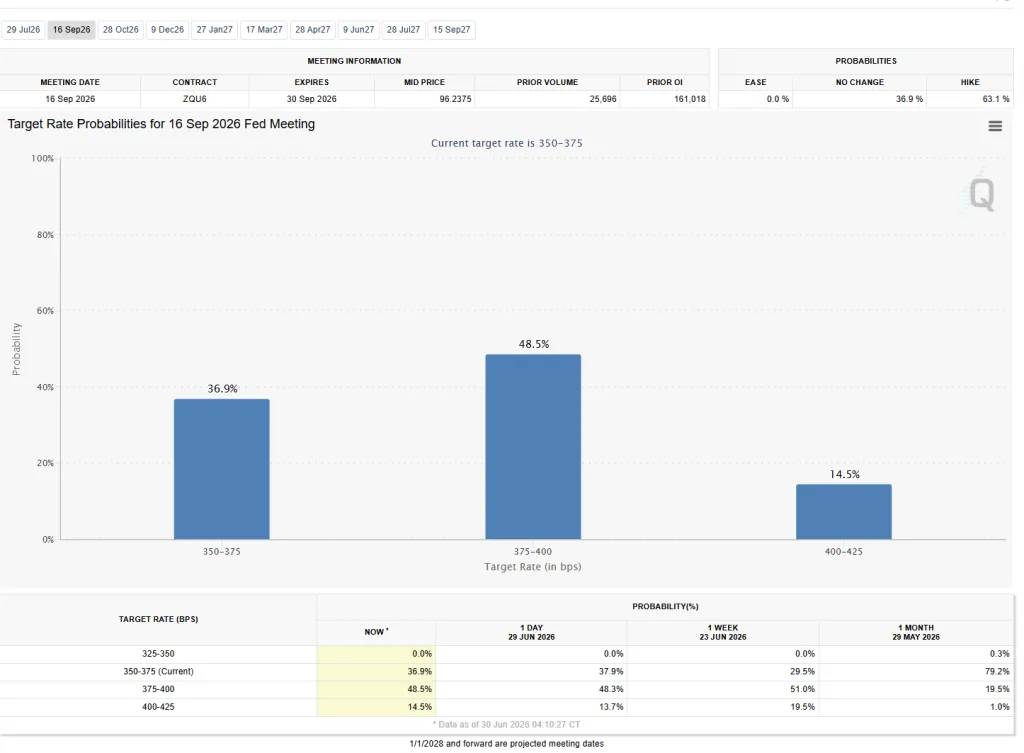

- The Pre-Election Timeline: The Federal Open Market Committee (FOMC) has three critical meetings scheduled before the November presidential election: July 29, September 16, and October 28.

- Market Pricing: Fed funds futures show a rapidly rising probability of tightening. The standalone probability of a rate hike at the July 29 meeting has climbed to 31.5 percent. When compounding the probabilities across the July, September, and October meetings, the market indicates a 70.4 percent chance of at least one rate hike before the election, with a growing probability of two hikes.

- The Political Flashpoint: An interest rate hike on September 16 would severely disrupt the conventional campaign season. A subsequent hike on October 28—just days before the election—would be an unprecedented monetary shock in modern political history.

- Executive Discontent: President Trump’s public and private expectations have focused on monetary easing. The appointment and support of Kevin Warsh as Fed Chair was widely viewed as a move to secure a more accommodative monetary environment. A series of rate hikes would represent a major institutional defiance of executive branch preferences.

Chronology of the 2026 Inflation Resurgence

The market’s sudden shift from expecting rate cuts to pricing in imminent rate hikes is the result of a multi-month acceleration in consumer prices. The timeline of recent economic releases highlights how quickly the inflation narrative recaptured Wall Street:

June 10, 2026: The Initial Warning Shot

The Bureau of Labor Statistics (BLS) released the Consumer Price Index (CPI) data for May, revealing that over the previous 12 months, the CPI had increased by 4.2 percent. This marked the fastest pace of inflation since April 2023. The print shocked economists who had predicted that supply-chain normalization and previous tightening cycles would keep inflation on a downward trajectory toward the 2.0 percent target.

June 15, 2026: The Service Sector Problem Revealed

A deeper analysis of the inflation components exposed structural imbalances in the domestic economy. Economists noted that while core goods inflation had moderated, services inflation remained highly elevated. Because services constitute a massive 63.4 percent of the total CPI basket, the persistent wage growth and consumer demand in this sector effectively neutralized any deflationary progress in manufacturing and retail goods.

June 25, 2026: Consolidation of the Hawkish Case

The latest inflation data confirmed that actual CPI inflation settled at 4.1 percent, representing a month-over-month increase of 0.4 percent. With the monthly run-rate annualizing to nearly 5.0 percent, market analysts realized the Federal Reserve had no choice but to keep its policy rate elevated, or actively tighten, to prevent inflation expectations from becoming unanchored. Consequently, bond yields surged, and Fed funds futures began aggressively pricing in pre-election rate hikes.

[May 2026 CPI: 4.2% YoY] ──> [June 15: Services identified as 63.4% of CPI] ──> [June 25: CPI at 4.1%, +0.4% MoM] ──> [Market prices 70.4% chance of pre-election hike]Supporting Data: Deconstructing the Market Probabilities

To understand the scale of the market’s hawkish shift, one must analyze the implied probabilities derived from the Chicago Mercantile Exchange (CME) FedWatch tool and Fed funds futures pricing.

The July 29 FOMC Meeting

In isolation, the market currently prices the probability of a 25-basis-point rate hike at 31.5 percent. While a pause remains the baseline scenario for July, a one-in-three chance of a hike reveals that investors believe the Fed is highly alarmed by the June inflation data.

The September 16 FOMC Meeting

If the Fed pauses in July to gather more data, September becomes the primary target for a policy adjustment. A rate hike at this meeting would occur at the height of the presidential campaign season, directly impacting consumer borrowing costs, mortgage rates, and stock market valuations just as voters are solidifying their choices.

The October 28 FOMC Meeting

The October meeting is highly unusual. Occurring a mere week before the presidential election, central banks traditionally use this period to signal stability and avoid any actions that could be interpreted as politically motivated. However, the futures market is pricing in a highly volatile scenario:

- A cumulative 70.4 percent chance of at least one rate hike by the end of this meeting.

- A reasonable and growing probability of two rate hikes (e.g., July/September or September/October) if the summer inflation prints do not rapidly cool.

| FOMC Meeting Date | Standalone Hike Probability | Cumulative Probability of At Least One Hike by This Date |

|---|---|---|

| July 29, 2026 | 31.5% | 31.5% |

| September 16, 2026 | High (Primary Target) | ~55.0% |

| October 28, 2026 | Moderate-High | 70.4% |

The Core Inflation Dilemma

The Federal Reserve’s reluctance to cut rates—and its inclination to raise them—is driven by the composition of the Consumer Price Index:

- The Target: 2.0%

- Current Actual CPI: 4.1% (up 0.4% month-over-month)

- The Services Component: Services represent 63.4 percent of the CPI. Because services are highly labor-intensive, sticky wage inflation directly translates into sticky consumer prices, making it incredibly difficult for the Fed to bring headline inflation down without inducing broader economic cooling.

Official Responses and Political Friction

The prospect of pre-election rate hikes has created a highly charged political atmosphere, pitting the executive branch’s economic goals against the central bank’s statutory independence.

The White House Perspective

President Trump has repeatedly and publicly expressed his desire for lower interest rates. Throughout his term, he has argued that high rates unnecessarily restrict domestic manufacturing, raise the cost of servicing the national debt, and penalize American consumers.

According to administration insiders, Trump’s expectation was that Fed Chair Kevin Warsh—whom he supported under the assumption that Warsh would favor a pro-growth, accommodative monetary policy—would initiate a series of rate cuts. The realization that the Warsh-led Fed may instead raise rates before the election has reportedly caused immense frustration within the West Wing. A rate hike in September or October would be viewed by the administration as an unnecessary drag on economic momentum and a direct challenge to the president’s economic policy record.

The Federal Reserve’s Institutional Stance

Publicly, Fed Chair Kevin Warsh and other members of the FOMC have maintained a strictly data-dependent, non-political narrative. In recent press conferences, Fed officials have reiterated that the central bank does not consider political calendars or election cycles when making interest rate decisions.

The Fed’s official position is that failing to act against 4.1 percent inflation would damage its long-term credibility and risk a repeat of the 1970s stagflationary spiral. Central bank defenders argue that if the Fed avoids necessary rate hikes simply because an election is near, it would prove that the institution is politically compromised, which could lead to even greater long-term market instability.

Strategic and Economic Implications

The divergence between market expectations and political desires carries profound implications for the financial system, the upcoming election, and the future of central bank independence.

1. Financial Market Volatility and the Bond Market

If the Federal Reserve proceeds with a rate hike in September or October, the bond market is likely to experience significant disruption. Short-term yields would spike, further inverting the yield curve and raising borrowing costs across the economy.

- Equities: High interest rates reduce the present value of future corporate earnings, which could trigger a pre-election correction in the stock market—an outcome the White House is desperate to avoid.

- Consumer Credit: Average Americans would immediately feel the impact through higher credit card APRs, auto loans, and mortgage rates, which are already hovering near multi-decade highs.

2. Electoral Fallout

Monetary policy tightening just weeks before an election is historically rare for a reason: it dampens consumer sentiment.

- The Incumbent Dilemma: A rate hike would allow political opponents to argue that the administration’s fiscal policies have fueled inflation so severely that the Fed was forced to step in and slow the economy.

- Consumer Sentiment: Even if the job market remains stable, the psychological impact of the Fed declaring that the economy is "overheating" and raising borrowing costs could sway undecided voters who are already highly sensitive to the cost of living.

3. The Future of Federal Reserve Independence

Perhaps the most lasting implication of this conflict is the potential threat to the Federal Reserve’s autonomy. If the Fed defies the White House and raises rates, it could trigger a coordinated political backlash.

Some policy analysts warn that a second Trump administration, frustrated by a hawkish Fed, could seek legislative changes to curb the central bank’s authority. Proposals could include restructuring the FOMC, giving the executive branch more direct oversight of interest rate decisions, or challenging the Fed’s dual mandate in Congress.

Ultimately, the stage is set for an extraordinary autumn. As inflation remains sticky at 4.1 percent and the service sector continues to prop up prices, Kevin Warsh and the FOMC are caught between a rock and a hard place: enforce their inflation target and face the wrath of the White House, or hold off on rate hikes to avoid political controversy and risk letting inflation run out of control. Whichever path the Fed chooses, the decision will reverberate far beyond Wall Street.