In the world of personal finance, the difference between long-term prosperity and perpetual struggle rarely comes down to raw income. Two individuals may earn the exact same six-figure salary, live in the same neighborhood, and possess identical savings habits, yet one may retire a millionaire while the other finds themselves perpetually catching up. The missing variable is not "how much," but "where first."

Financial success is not a random act of saving; it is an exercise in strategic priority. When individuals treat their capital as a fungible resource—shuffling money into savings, investments, and debt repayments without a logical hierarchy—they suffer from "optimization leakage." By failing to place every dollar in the highest-leverage position, they lose years of compounding potential and incur unnecessary interest costs.

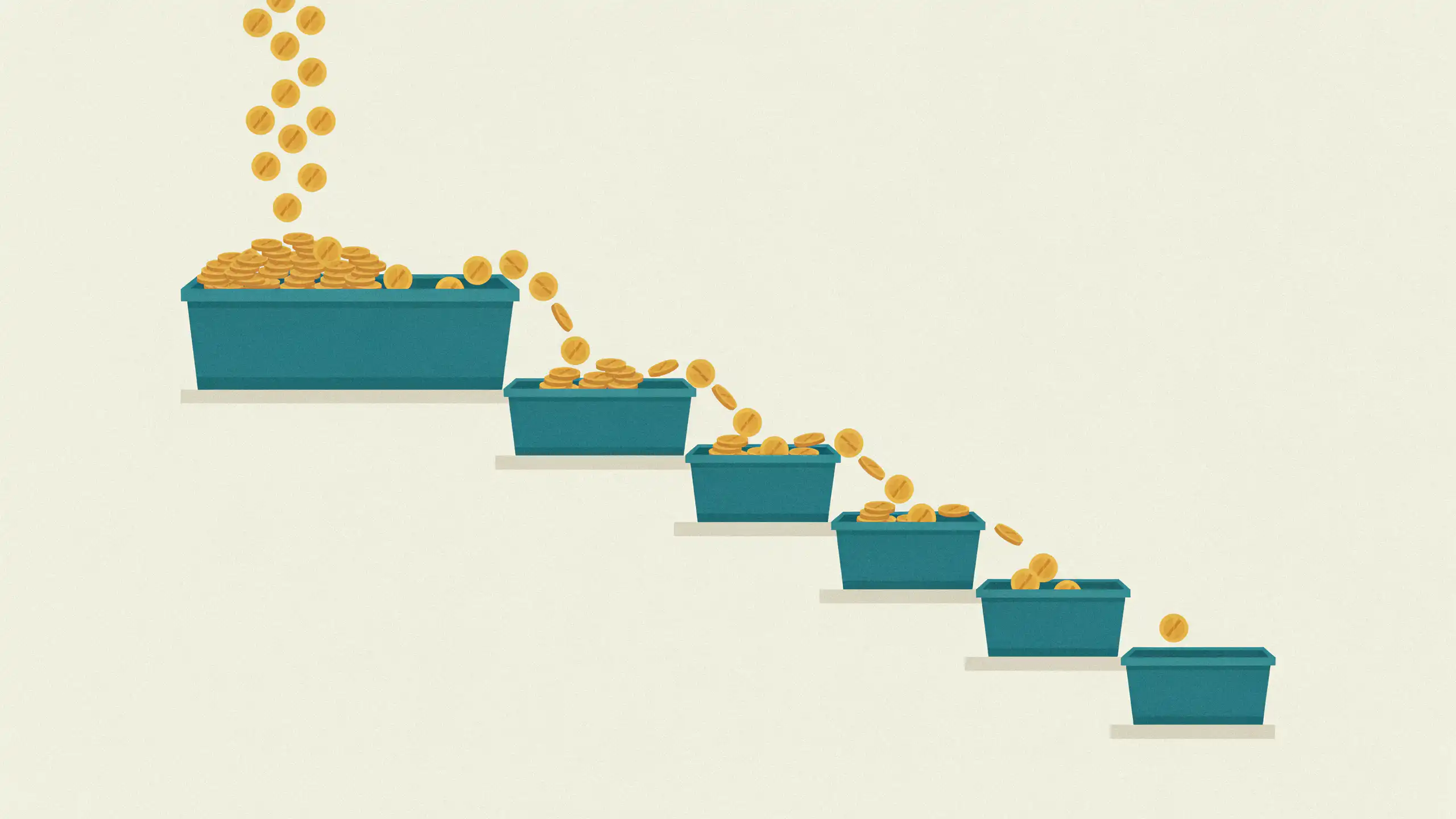

To master your financial destiny, you must adopt a rigid "Financial Order of Operations." By funneling your resources through a specific sequence of buckets, you ensure that every dollar works at maximum efficiency before moving on to the next task.

The Strategic Sequence: A Six-Step Blueprint

The logic behind a prioritized sequence is rooted in the mathematical reality of returns and risk mitigation. Each step serves as a prerequisite for the next, ensuring that you are not building a skyscraper on a foundation of sand.

1. The Starter Emergency Buffer

Before you invest a single penny, you must establish a "starter" emergency fund—typically $1,000 to $2,000. This is not for long-term security; it is a tactical defensive measure. Without this cash buffer, any minor life event—a flat tire, a broken appliance, or a surprise medical bill—forces you to utilize credit cards. By having cash on hand, you prevent the cycle of high-interest debt before it can start.

2. The Employer 401(k) Match

Once the starter buffer is in place, your immediate priority should be securing your employer’s 401(k) match. This is the closest thing to "free money" in the financial world. If your employer offers a 50% or 100% match on your contributions, you are receiving an immediate, guaranteed return on investment that no stock market index or real estate deal can match. Prioritizing anything else over this match is, quite literally, leaving a raise on the table.

3. High-Interest Debt Liquidation

Credit card debt, which often carries interest rates exceeding 20%, is a financial anchor. Because the interest on this debt consistently outpaces the long-term average return of the stock market (typically 7–10%), every dollar used to pay down a credit card balance is effectively a guaranteed return equal to the interest rate of the card. You cannot out-invest a 20% interest rate; you must eliminate it first.

4. The Full Emergency Fund

With high-interest debt gone and the employer match secured, it is time to build a robust emergency fund—usually three to six months of essential living expenses. This fund serves as your insurance policy against job loss or major medical events. It provides the psychological safety net necessary to remain invested in the market during downturns, preventing the panic-selling that destroys wealth.

5. Individual Retirement Accounts (IRAs)

Once your basic financial defenses are shored up, you move toward tax-advantaged growth. Contributing to a Roth or Traditional IRA allows your money to grow either tax-free or tax-deferred. These accounts offer more investment flexibility than most employer-sponsored 401(k) plans, allowing you to curate a portfolio that aligns with your specific risk tolerance and long-term goals.

6. Taxable Brokerage and Wealth Expansion

Only after the previous five steps are optimized should you direct surplus capital into standard brokerage accounts. At this stage, your foundation is secure, your "free" money is captured, your high-interest liabilities are extinguished, and your tax-advantaged accounts are being utilized. Now, your remaining dollars can be deployed for general wealth creation.

The Mathematics of Prioritization: Why Order Matters

The core principle at play here is opportunity cost. Every dollar has a "best and worst" place to be at any given moment.

Consider the individual who ignores their employer match to pay off a low-interest student loan, or the person who funds a brokerage account while carrying a 22% APR credit card balance. They are sacrificing guaranteed returns for the sake of psychological comfort or perceived progress.

In the financial sector, experts often refer to this as the "leakage of compounding." If you contribute $5,000 to a brokerage account but pay $2,000 in credit card interest over the same year, you are essentially losing money in the transaction. By reordering these activities, you stop the outflow of interest and capture the inflow of employer contributions, effectively accelerating your net worth growth without having to earn a single extra dollar in salary.

Supporting Data and Economic Context

Financial research consistently supports the "waterfall" approach to capital allocation. According to historical market data, the long-run annual return of the S&P 500 hovers around 10%. Conversely, consumer debt interest rates have remained consistently higher, often ranging between 18% and 25%.

When an individual chooses to invest in the market while holding 20% interest debt, they are effectively betting that their investments will outperform a 20% hurdle rate. Statistically, this is a losing bet. By prioritizing the debt payoff, you are securing a "risk-free" return of 20%—a performance level that even the world’s most elite hedge fund managers would struggle to maintain.

Furthermore, the behavioral aspect of this sequence cannot be ignored. Following a structured, objective sequence removes the "decision fatigue" that leads to erratic financial behavior. When a bonus or tax refund arrives, the "Financial Order of Operations" provides an immediate directive: find the first unfinished bucket and fill it.

Official Perspectives: The Professional Consensus

Financial planners and fiduciary advisors widely endorse this hierarchy. While specific nuances may change based on individual tax brackets or unique debt structures, the foundational principle remains the same.

"The most common mistake we see is the pursuit of complexity over priority," says a lead analyst in personal finance. "Investors are often obsessed with picking the right stock or the next big ETF, but they are ignoring the fact that they are losing thousands annually by not maximizing their employer match or by carrying high-interest debt. The sequence is the strategy."

Furthermore, regulators emphasize the importance of liquidity. By building a starter buffer before committing funds to long-term retirement accounts, individuals protect themselves from the penalties and taxes associated with early withdrawals from 401(k) or IRA accounts. A proper sequence respects the liquidity requirements of real life, ensuring that you don’t have to raid your retirement to pay for a mundane emergency.

Implications for Your Financial Future

Adopting this systematic approach requires a shift in mindset. You must stop viewing your money as a single pool of funds and start viewing it as a series of specialized tools.

The "Concurrent" Misconception

A common critique of this model is that it is too slow—that one should be "doing everything at once." While it is true that you can (and should) run some steps concurrently (for example, paying down debt while contributing to a 401k), the priority must remain clear. If you have to choose between an extra $500 toward a debt and an extra $500 toward a brokerage account, the sequence provides the absolute answer: the debt.

The Long-Term Compounding Effect

The implications of this strategy are magnified over decades. An extra $5,000 invested early due to a higher-priority sequence can grow into significantly more over 30 years compared to the same amount invested late. By consistently funneling dollars into the highest-impact buckets, you shorten the time required to reach financial independence.

Final Thoughts: The Path Forward

The next time a windfall arrives—be it a tax refund, a bonus, or a raise—avoid the temptation to "reward" yourself immediately or guess where the money should go. Consult the sequence. If your 401(k) match isn’t capped, send it there. If your credit cards aren’t at zero, pay them down.

Wealth is not built by luck; it is built by the boring, consistent, and logical allocation of every available dollar. By following the Financial Order of Operations, you transform your financial life from a series of reactive decisions into a proactive, wealth-generating machine. The sequence is simple, but in its simplicity lies its power. Follow the steps, maintain the discipline, and let the mathematics of compounding do the heavy lifting for you.