Value Added Tax (VAT) is the lifeblood of European fiscal policy, providing a stable and substantial stream of revenue for governments across the continent. Yet, for small and medium-sized enterprises (SMEs), the administrative burden of VAT compliance can be a formidable barrier to entry. To mitigate this, many nations implement "VAT registration thresholds"—a revenue ceiling below which a business is exempt from the bureaucratic rigors of the VAT system.

However, recent data reveals a complex, often counterintuitive landscape. While these thresholds are intended to protect small businesses, they frequently trigger unintended economic consequences, including the "bunching" of firms below revenue limits, the stifling of productivity, and significant distortions in market competition. As several European nations move to raise these thresholds, the debate over their efficiency has never been more relevant.

The Landscape of VAT Exemptions: Nominal vs. Real Value

Across 32 major European economies, the approach to VAT exemptions varies wildly. When looking at the nominal, or absolute, value of these thresholds, Switzerland leads the pack. Businesses in the Alpine nation can generate up to CHF 100,000 (€106,724) before they are required to register for VAT. The United Kingdom and France follow, with thresholds set at £90,000 (€105,043) and €87,000, respectively.

At the other end of the spectrum, some nations have eschewed the threshold model entirely. Spain and Turkey, for instance, maintain a zero-threshold policy. In these jurisdictions, every business—regardless of its size or annual turnover—is enrolled in the VAT system from its inception.

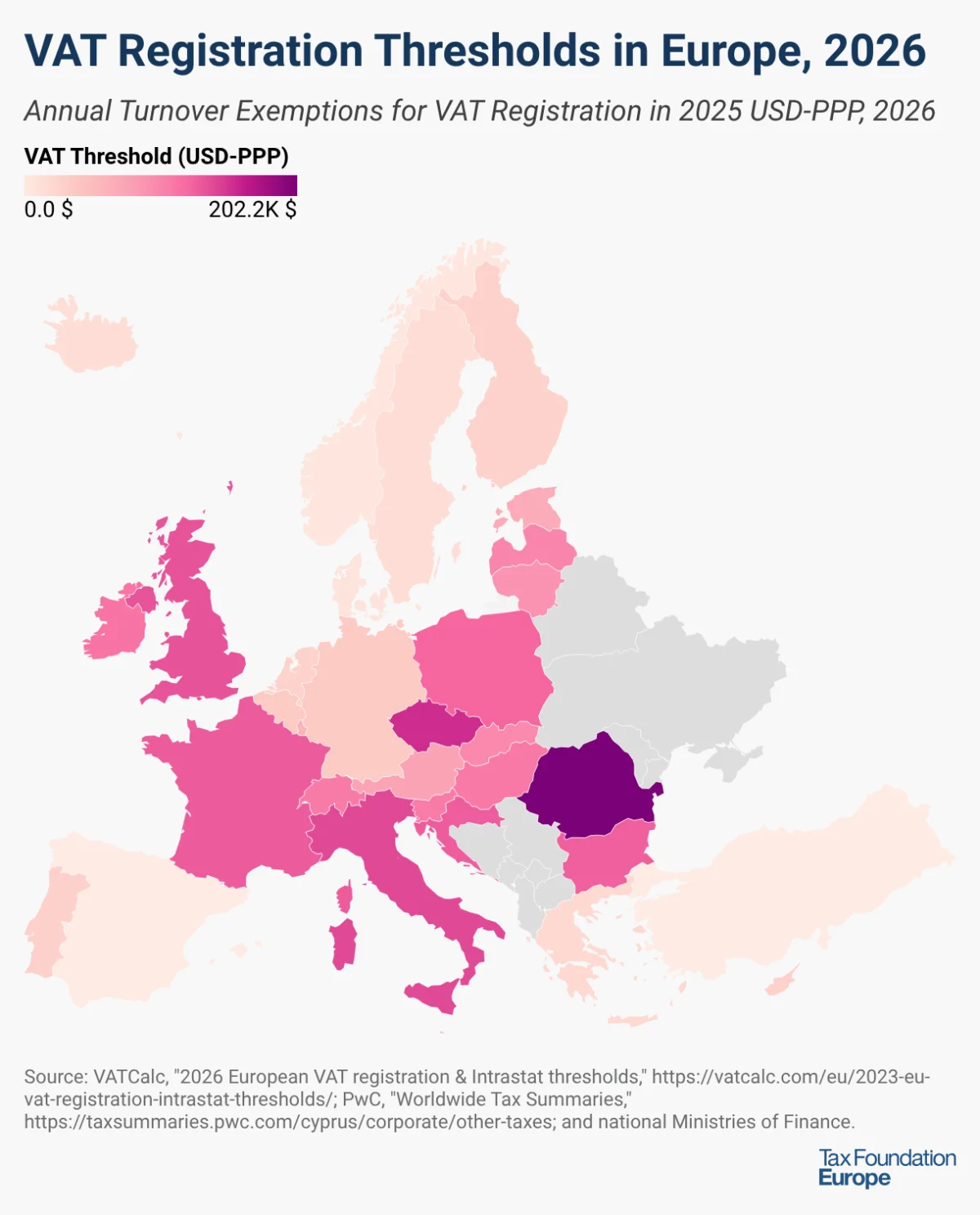

Adjusting for Purchasing Power Parity (PPP)

A simple comparison of nominal figures can be misleading due to the varying costs of living and doing business across the continent. When analysts adjust for Purchasing Power Parity (PPP)—a measure that reflects the true "buying power" of currency in a specific market—the picture changes significantly.

Under the PPP lens, Romania boasts the highest threshold in Europe, sitting at RON 395,000, which carries an economic weight equivalent to approximately $202,206. The Czech Republic and Italy also maintain high real-value thresholds, at $155,039 (CZK 2,000,000) and $140,246 (€85,000) respectively. This data suggests that while nominal thresholds provide a snapshot of regulatory policy, PPP-adjusted figures are a more accurate barometer of the actual competitive advantage (or disadvantage) afforded to small firms in different European markets.

Chronology of Recent Legislative Shifts

The trend across Europe in the 2025–2027 period has been a consistent upward adjustment of these thresholds, often framed by governments as a move to support small-scale entrepreneurship during inflationary periods.

- September 2025: Romania took proactive steps to shield its small business sector by raising its threshold from RON 300,000 to RON 395,000.

- January 2026: Hungary initiated the first phase of a multi-year plan to increase its threshold, moving from HUF 18 million to 20 million.

- January 2026: Poland implemented a significant hike, raising its registration limit from PLN 200,000 to 240,000.

- April 2026: The Belgian parliament signaled a shift in policy, approving a move to raise the exemption threshold from €25,000 to €30,000. While the measure has been approved, the formal implementation remains in the final stages of the legislative process.

- 2027 Outlook: Hungary is scheduled to further increase its threshold to HUF 22 million, continuing a trend of aggressive upward adjustments for small enterprises.

The Economic Implications: Efficiency vs. Distortion

The core justification for VAT thresholds is the reduction of administrative and compliance costs. For a micro-enterprise, the cost of filing, auditing, and maintaining VAT-compliant accounting can represent a disproportionate share of their overhead. By removing this requirement, governments aim to foster a vibrant ecosystem of small, flexible firms.

However, this policy creates a "distortionary tax" environment. By shielding smaller firms from the tax burden that their larger competitors must bear, governments are essentially picking winners and losers. This creates a market where smaller, tax-advantaged firms can outcompete larger, more productive, and potentially more efficient rivals.

The "Notch" and the Tax Cliff

Perhaps the most damaging effect of the threshold is the creation of a "tax cliff" or "notch." Because the exemption is typically binary—meaning you are either in the system or you are out—a firm that earns exactly one euro above the threshold suddenly faces a substantial tax burden on its entire value-added, rather than just the marginal amount earned over the limit.

This creates a perverse incentive for business owners. Empirical evidence, including extensive studies by the IMF and various fiscal policy think tanks, shows that firms often engage in "bunching" behavior. They purposefully cap their growth, underreport their turnover, or scale back their operations to stay just below the VAT threshold.

The Czech Republic serves as a primary case study for this phenomenon. Data shows a distinct spike in the distribution of corporations just below the national VAT threshold. As the government increases the threshold, the "bunching point" of these firms shifts in lockstep, proving that businesses are actively adjusting their economic activity to avoid the tax rather than focusing on growth and scale.

Official Perspectives and Policy Recommendations

The consensus among tax economists is shifting away from high thresholds. While they provide immediate relief for the smallest businesses, the long-term cost to the economy is high.

The Productivity Trap

When businesses are incentivized to remain small to avoid the VAT, they fail to realize the benefits of economies of scale. In a competitive global market, this leads to a stagnation of productivity. If a firm is afraid to grow because it will trigger a tax liability that wipes out its margins, that firm will remain a "micro-enterprise" indefinitely, preventing it from investing in new technologies, hiring more staff, or expanding into new markets.

Toward a Streamlined System

Policy experts suggest that instead of raising thresholds, governments should focus on:

- Simplifying VAT Compliance: Rather than exempting firms, governments should reduce the complexity of the VAT system so that compliance is less of a burden for all businesses, regardless of size.

- Phased Implementation: Implementing a "tapered" system—where tax liability increases gradually as a firm grows, rather than hitting a cliff—would remove the incentive to stay small.

- Digitalization: Leveraging e-invoicing and automated tax reporting can lower the administrative cost of VAT for small businesses, effectively providing the same benefit as an exemption without the negative market distortions.

Conclusion

The evolution of VAT thresholds in Europe reflects a tug-of-war between the desire to support local, small-scale commerce and the need for a neutral, efficient tax system. While the recent hikes in countries like Hungary, Poland, and Romania are intended to provide temporary relief, they risk entrenching a culture of "bunching" and limiting the potential for European firms to achieve the scale necessary to compete on the global stage.

As policymakers continue to navigate the complexities of fiscal sustainability, they must recognize that thresholds are not merely administrative tools—they are powerful signals that shape how businesses grow. For the European economy to thrive, the focus must shift from protecting the small at the expense of the productive to creating a tax environment where growth is rewarded, not penalized. By reducing or eliminating these thresholds and focusing on systemic simplification, European nations can build a more robust, efficient, and equitable economic future.