In the modern financial landscape, individuals are inundated with data points. Between banking apps, credit card notifications, and investment portals, the average consumer receives a constant stream of information regarding their cash flow. However, financial experts increasingly argue that these fragmented data points create a "fog of war" that obscures the most critical metric of personal prosperity: Net Worth.

While monthly budgets and checking account balances capture the turbulence of daily life, they fail to provide a strategic overview of one’s long-term financial trajectory. To achieve true financial security, one must shift focus from the micro-fluctuations of spending to the macro-perspective of total net worth.

The Core Concept: Defining Financial Health

At its most fundamental level, net worth is a simple equation: Assets minus Liabilities.

Assets represent everything you own that holds value—cash in savings, retirement accounts, brokerage portfolios, real estate equity, and personal property. Liabilities represent everything you owe—mortgages, student loans, credit card balances, and personal lines of credit.

The resulting figure is the objective "scorecard" of your financial life. If your net worth is increasing quarter over quarter, you are building wealth, regardless of whether a specific month felt "messy" due to unforeseen expenses or seasonal fluctuations.

Why Checking Accounts Are Misleading

The balances you check most often are ironically the least informative. A checking account is a transactional vessel. It rises with a paycheck and falls with rent, mortgage payments, and grocery runs. It is designed for fluidity, not stability.

Many people feel a sense of financial anxiety when their checking balance dips, even if that money was used to pay down high-interest debt. Conversely, a high checking balance can provide a false sense of security while one’s long-term debt or retirement savings remain stagnant. Focusing on the checking account is akin to monitoring the fuel flow of an engine rather than the actual speed and direction of the vehicle.

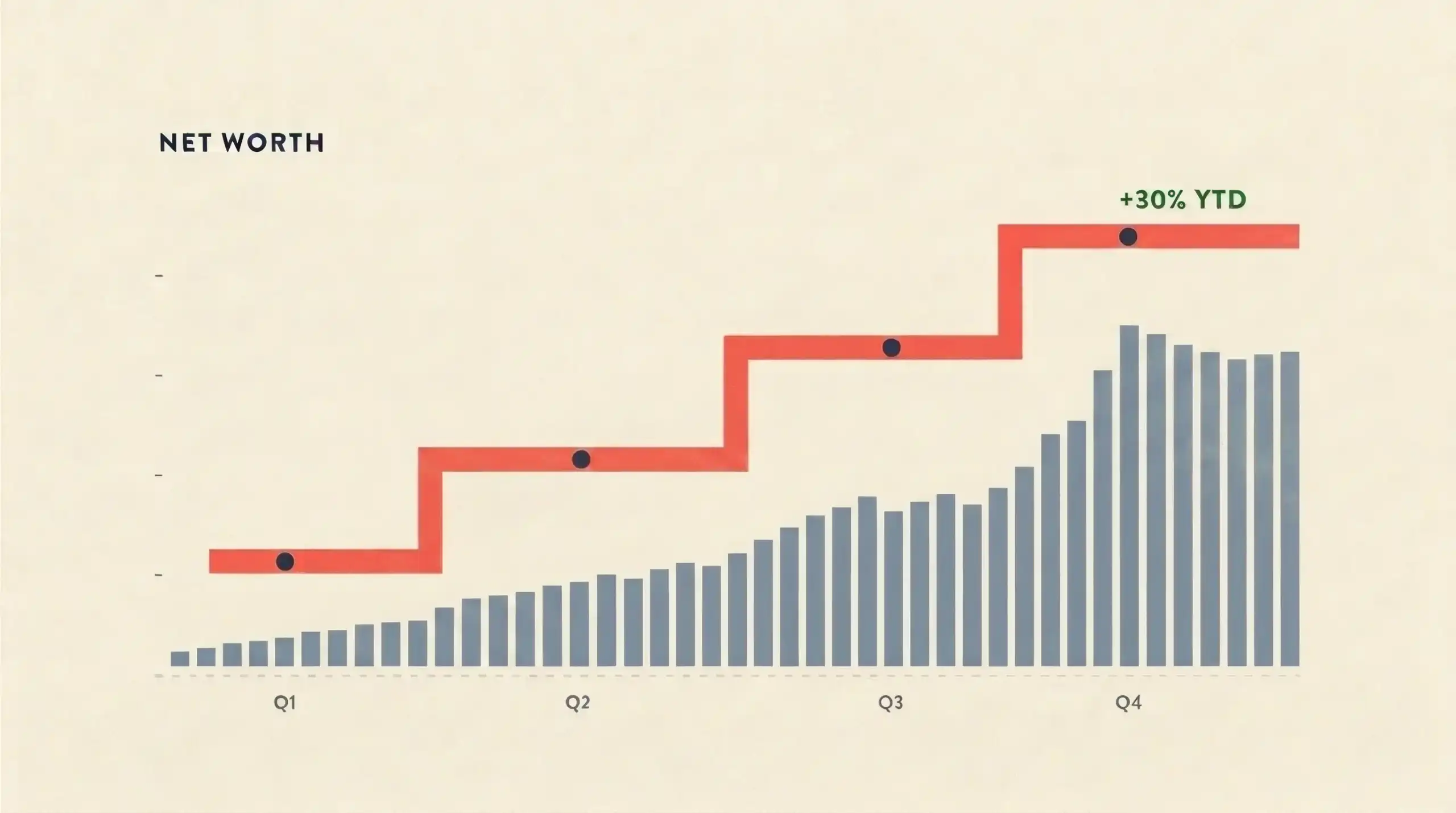

Chronology of Wealth Tracking: A Quarterly Rhythm

Establishing a sustainable routine is the greatest hurdle to effective financial management. When people attempt to track their finances, they often choose the wrong frequency.

The "Goldilocks" Frequency

- Monthly Tracking: Often considered too noisy. Because markets fluctuate and expenses are rarely linear, a monthly view can be disheartening. A single market dip or a one-time major repair can make a month look like a failure, even if your underlying habits are sound.

- Annual Tracking: Too infrequent. Waiting a full year to check your progress is the financial equivalent of driving with your eyes closed. By the time you realize you have drifted off course, 365 days of compounding interest—or compounding debt—have already passed.

- Quarterly Tracking: The "Goldilocks" zone. Checking your net worth every three months (January, April, July, and October) is the optimal rhythm. It provides enough distance to smooth out the "noise" of monthly volatility, yet it is frequent enough to allow for meaningful course correction before a bad trend becomes a permanent habit.

Supporting Data: The Psychology of Progress

The psychological impact of tracking net worth cannot be overstated. When you pay $400 toward a credit card, it often feels like a loss because your cash balance drops immediately. However, when viewed through the lens of net worth, that $400 is a victory: your liabilities have decreased by $400, meaning your total net worth has increased by the same amount.

This shift in perspective transforms the "pain" of saving into the "gain" of wealth building. Data from personal finance platforms indicates that users who engage in periodic net-worth check-ins are 30% more likely to reach their retirement goals than those who rely solely on static budgeting methods. By moving the focus from "spending limits" to "total asset growth," individuals adopt a more proactive, investment-minded approach to their personal economy.

Implementation: Building Your Dashboard

Modern technology has rendered the days of manual spreadsheets obsolete. Setting up a robust tracking system requires roughly 20 minutes of initial effort.

Step 1: Choosing a Dashboard

Platforms such as Empower or Monarch Money act as financial aggregators. These tools securely connect to your various accounts—checking, savings, investment, and debt—to provide a real-time, consolidated view of your financial life.

Step 2: The Integration

Once you have selected a platform, the process is straightforward:

- Link all accounts: Ensure every asset and liability is included. If you have a home, include its estimated market value; if you have a car loan, ensure the current payoff amount is synced.

- Automate the updates: Most modern dashboards refresh these balances automatically.

- The Quarterly Ritual: Set a recurring calendar reminder for the first weekend of the new quarter. The actual task takes less than two minutes: log in, record the total net worth number, and compare it to the previous quarter.

Official Perspectives: Financial Literacy and Long-Term Stability

Financial advisors and economists increasingly point to net-worth tracking as a foundational skill in financial literacy. Unlike a budget, which is a restrictive tool often associated with deprivation, tracking net worth is an empowering tool associated with growth.

The "Direction Over Precision" Rule

One of the most common mistakes novices make is obsessing over the exactness of the number. If your home value estimate is off by a few thousand dollars, it does not invalidate the utility of the exercise. The goal is to judge the trend, not the snapshot.

If you see four consecutive quarters of flat growth, it is a clear signal that something is wrong—perhaps your lifestyle inflation is canceling out your savings rate, or your investment portfolio is underperforming. At that point, you can perform a "deep dive" audit. Without the quarterly check-in, you might have continued on that trajectory for years.

Implications: The Shift Toward Wealth Consciousness

By adopting a net-worth-centric mindset, you effectively detach your emotional state from the daily stresses of consumerism. You stop viewing a $500 purchase as a "loss" and start viewing your entire financial life as a business.

Avoiding Common Pitfalls

- Market Volatility: Do not panic during a down quarter. A market correction is a normal part of the economic cycle. If your savings rate remains consistent, your net worth will eventually recover and grow.

- Debt Reduction: Early on, your net worth might be negative. Do not let this discourage you. The goal is to make that number "less negative" each quarter.

- The "Audit" Trap: Avoid the temptation to perform a microscopic audit every month. It leads to burnout. A quick, quarterly glance at one number consistently outperforms a detailed, complex audit that you eventually stop doing altogether.

Conclusion

Financial security is not found in the fleeting balance of a checking account, nor is it found in the occasional, panicked look at a credit card statement. It is found in the quiet, consistent tracking of your net worth. By adopting this quarterly ritual, you move from being a passenger in your financial life to being the driver. You gain the ability to see the direction of your wealth, the power to correct your course, and the peace of mind that comes from knowing exactly where you stand—and where you are going.

As the old adage in finance goes: "What gets measured, gets managed." By measuring your net worth, you take the first step toward true financial mastery.