Executive Summary: A Market at the Crossroads

Global energy markets are currently navigating a delicate transitional phase, shifting away from the geopolitical risk premiums that dominated the volatility landscape in previous quarters. As tensions surrounding critical maritime chokepoints like the Strait of Hormuz begin to moderate, investors are recalibrating their outlooks based on a more traditional set of macroeconomic drivers.

At the heart of current price action is a fundamental reassessment of demand-side health. With crude oil consolidating in a compressed technical range, the focus has pivoted toward U.S. manufacturing momentum and labor-market resilience. As markets await the critical U.S. payrolls data due this Thursday, the intersection of industrial output, logistics, and interest rate expectations is defining the next chapter for WTI (West Texas Intermediate) pricing.

The Chronology of Market Sentiment

The trajectory of crude oil over the past several months has been defined by a distinct "risk-off" transition.

- The Geopolitical Peak: Early in the cycle, markets were heavily influenced by supply-chain anxiety stemming from Middle Eastern instability. During this period, the "war premium" insulated prices from weakening economic fundamentals.

- The Normalization Phase: As geopolitical flare-ups failed to materialize into physical supply disruptions, the market began a systematic liquidation of risk premiums. This was facilitated by a noticeable improvement in tanker flows through the Strait of Hormuz, effectively cooling fears of a supply-side shock.

- The Data-Dependent Transition: Currently, we are in the "Macro-Pivot" phase. Traders have largely dismissed the lingering tail-risk of supply disruptions, choosing instead to focus on the correlation between industrial manufacturing activity and refined-product consumption.

- The Awaiting Catalyst: The current period is defined by intense compression. With markets braced for the upcoming labor-market release, trading volumes have thinned, and directional conviction has waned as participants seek confirmation from the U.S. Bureau of Labor Statistics.

Supporting Data and Technical Analysis

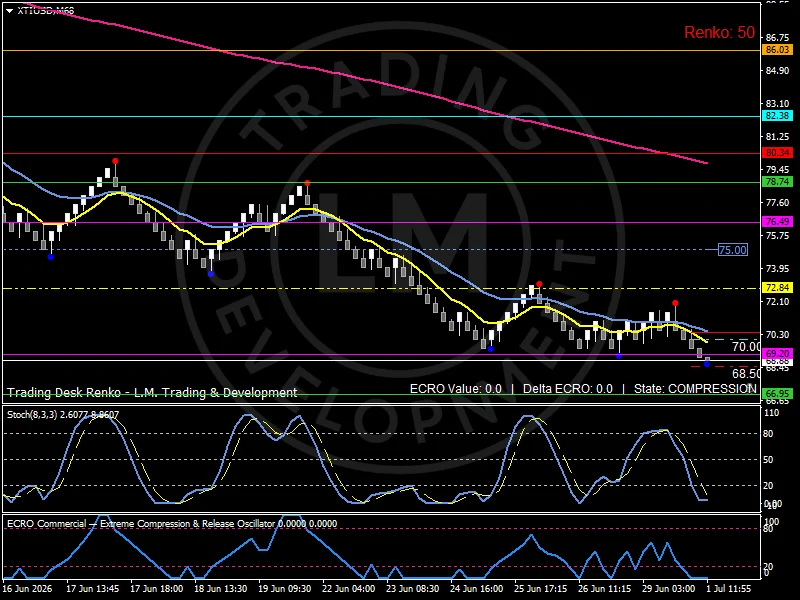

The technical structure of WTI currently mirrors the ambiguity of the broader macro environment. The market is caught in a tight range, characterized by indecisive price action and a lack of momentum.

Key Technical Levels

- Support Zones: Immediate support is anchored at the $69.20 level. A breach below this point would likely test the more robust $68.50 zone, where significant buying interest has historically emerged.

- Resistance Zones: On the upside, the path is obstructed at $72.10. Should buying momentum break through, the next targets reside at $74.40, with a major participation hurdle waiting at the $75.00 psychological mark.

- Trend Indicators: The Renko structure, combined with a declining Exponential Moving Average (EMA) configuration, paints a picture of a market in search of a trend. The lack of upward momentum suggests that the "sell-the-rally" mentality remains prevalent among institutional participants.

Momentum and Volatility

Momentum indicators are currently subdued, reflecting the market’s "wait-and-see" posture. Stochastic readings are drifting lower, and the ECRO (Energy Compression Range Oscillator) remains in a state of flux. This compression is not merely a technical phenomenon; it is a direct reflection of the market’s reluctance to commit capital until the U.S. labor-market report provides clarity on the health of the consumer.

The Role of Manufacturing and Logistics

The relationship between U.S. manufacturing activity and energy pricing has never been more vital. Recent data showing U.S. manufacturing at a multi-year high provided a brief lift to crude, highlighting the intrinsic link between industrial output and energy demand. When factories are active, demand for refined products—specifically diesel and heating oil—tends to climb.

However, this is tempered by lingering logistics concerns. Despite the easing of broad supply fears, freight indicators continue to signal elevated operational stress. These logistics bottlenecks serve as a "shadow tax" on the energy complex, preventing a smooth transition to higher price tiers even when demand signals appear positive.

Implications of the Labor Market Report

The impending U.S. payrolls report represents the most significant catalyst for the remainder of the trading week. The implications of this data extend far beyond the labor market itself:

- Treasury Yields: Stronger-than-expected payroll data could trigger a spike in Treasury yields, potentially strengthening the U.S. Dollar. A stronger dollar historically acts as a headwind for crude oil, as it makes dollar-denominated commodities more expensive for international buyers.

- Growth Expectations: The payroll report serves as a proxy for consumer confidence. If the labor market shows signs of cooling, it could trigger recessionary fears, forcing analysts to further lower their long-term oil-price projections.

- Monetary Policy Alignment: The Federal Reserve’s stance on interest rates is tethered to labor data. A soft print might reignite hopes for aggressive rate cuts, which could provide a bullish floor for oil prices by easing financial conditions.

Institutional and Analyst Perspectives

Wall Street analysts have been revising their projections downward throughout the current quarter. The consensus view suggests that the "easy money" period of betting on geopolitical supply shocks has ended.

"We are seeing a fundamental transition from event-driven trading to data-driven trading," notes one market analyst. "Institutional desks are now prioritizing yield-spreads and manufacturing PMI over the traditional geopolitical risk models. Until we see a sustained break in the current consolidation range, we expect participation to remain tactical and short-term."

This professional caution is evident in the current lack of open interest growth. Most traders are maintaining "tactical flexibility," holding positions that allow for quick exits if the payroll data triggers a sharp, unexpected move in either direction.

What Traders Should Watch: A Strategic Checklist

As the market approaches this inflection point, traders should focus on the following variables to navigate the expected volatility:

- The Payroll Delta: Pay close attention not just to the headline "Non-Farm Payroll" number, but to the revision of previous months. Consistent downward revisions could signal a more rapid labor-market slowdown than the headline number suggests.

- Dollar Correlation: Monitor the DXY (U.S. Dollar Index) in the immediate aftermath of the data release. An inverse relationship between the USD and WTI is expected, but any decoupling could signal an exogenous shift in supply/demand dynamics.

- Freight and Logistics Indices: Keep an eye on shipping costs. If logistics stress increases despite stable crude prices, it indicates that the market is struggling with physical supply-chain integrity, which could eventually force a price adjustment.

- Treasury Yield Curve: The 2-year and 10-year yield spread remains a primary driver of risk appetite. A "bear steepening" or "bull flattening" of the curve will provide immediate insight into how the broader market is pricing in future economic performance.

- Breakout Confirmation: Avoid premature entry on the current consolidation. Wait for a high-volume close outside of the $69.20–$72.10 range to confirm that a new directional trend has been established.

Conclusion: Preparing for the Catalyst

The crude oil market is currently in a "compressed structure," a state where energy is building for a move but the direction remains tethered to external data. The shift from geopolitical theater to the cold, hard reality of labor-market statistics is a healthy, albeit volatile, development for the commodity.

As we move toward the close of the week, the combination of manufacturing expectations and payroll outcomes will determine whether crude finds the floor necessary to build a new base or if it is destined to revisit lower liquidity zones. For the professional trader, the message is clear: prioritize capital preservation, keep a watchful eye on the dollar-yield nexus, and prepare for the volatility that typically follows when compressed structures meet high-impact macro catalysts. The current environment is not one for long-term conviction, but rather for sharp, agile, and data-backed tactical maneuvering.