Main Facts: The Passing of a Financial Titan

Alan Greenspan, the former Chairman of the Federal Reserve who presided over the American economy for more than eighteen years and came to embody the global archetype of the modern central banker, has died. He passed away on June 22 at his home in Washington, D.C., at the age of 100. His death marks the end of an era for global finance, leaving behind a complex, highly debated legacy of a man once celebrated as the "Maestro" of the world economy, whose later years were shadowed by the systemic crises that challenged his free-market convictions.

Greenspan’s tenure at the helm of the Federal Reserve spanned five terms and four U.S. presidential administrations. Appointed by Ronald Reagan in 1987, he served through the administrations of George H.W. Bush and Bill Clinton, before retiring under George W. Bush in 2006. During this nearly two-decade reign, Greenspan accumulated a level of institutional power and public reverence that few unelected officials in American history have ever matched. For a generation of investors, policymakers, and the public, he was the ultimate arbiter of economic health—an "Oracle" whose briefest utterances could trigger multi-billion-dollar shifts in global capital markets.

While Greenspan did not invent the modern Federal Reserve, he constructed the policy templates, communicative styles, and crisis-response mechanisms that every successor has been forced to either adopt or consciously reject. To understand the contemporary landscape of global monetary policy—with its reliance on forward guidance, liquidity injections, and delicate market management—one must return to the Greenspan era: a period defined by immense public confidence, unprecedented economic expansions, and the structural vulnerabilities that ultimately reshaped global finance.

Chronology: From Juilliard to the Temple of Money

[1926] Born in New York City

│

[1940s] Attended Juilliard; toured with Henry Jerome swing band

│

[1950s] Earned economics degrees at NYU; co-founded Townsend-Greenspan & Co.

│

[1968] Joined Nixon's campaign as a domestic policy advisor

│

[1974] Appointed Chairman of the Council of Economic Advisers under Ford

│

[1987] Appointed Chairman of the Federal Reserve by Ronald Reagan

├── Oct 1987: Handled "Black Monday" stock market crash

└── 1990s: Steered the longest peacetime economic expansion in U.S. history

│

[2006] Retired from the Federal Reserve; succeeded by Ben Bernanke

│

[2008] Testified before Congress; admitted a "flaw" in his laissez-faire ideology

│

[2026] Passed away in Washington, D.C., at the age of 100Early Life, Music, and Academic Awakening (1926–1953)

Alan Greenspan was born on March 6, 1926, in the Washington Heights neighborhood of New York City. Raised during the height of the Great Depression by his mother after his parents divorced, young Greenspan developed a sober, analytical view of money and risk from an early age. His father, Herbert Greenspan, was a stockbroker and market analyst who wrote an early, prophetic book advising his son on the mechanics of the American economy.

Greenspan’s first professional passion, however, was not economics, but music. A talented woodwind player, he attended the prestigious Juilliard School, studying clarinet and saxophone. In the mid-1940s, he toured the country with Henry Jerome’s swing band, playing alongside future jazz legend Stan Getz. While his bandmates spent their intermissions socializing, Greenspan was known to sit in the corner of the tour bus reading books on Wall Street and corporate finance.

Realizing his intellectual limits as a performer compared to his peers, Greenspan abandoned the music circuit to pursue his growing interest in arithmetic and economics. He enrolled at New York University (NYU), where he earned his bachelor’s degree in 1948 and his master’s degree in 1950, both in economics, graduating with highest honors. He pursued further doctoral studies at Columbia University under the tutelage of Arthur Burns, a future Federal Reserve Chairman who would deeply influence Greenspan’s empirical approach to economic data.

In 1953, Greenspan co-founded the economic consulting firm Townsend-Greenspan & Company. For more than two decades, he ran this highly successful enterprise, advising industrial giants on the granular realities of physical commodities like steel, aluminum, and copper. This unglamorous, highly detailed work gave him an intuitive, tactile understanding of the supply chains and real-world forces driving the American economy.

The Ayn Rand Influence and Entry into Public Policy (1950s–1980s)

During his early professional years, Greenspan encountered the novelist and philosopher Ayn Rand, the champion of Objectivism and radical laissez-faire capitalism. He became a core member of her inner circle, known as "The Collective," alongside future prominent thinkers. Under Rand’s influence, Greenspan absorbed a foundational belief that would guide his regulatory philosophy for decades: that unregulated, competitive markets are inherently self-correcting and allocate capital far more efficiently than state planners or government regulators.

The irony that a self-described libertarian Republican would spend the apex of his career running the ultimate state monetary planning institution remains one of the most striking paradoxes of modern American political history.

Greenspan’s transition into Washington public policy began in 1968, when he served as a domestic policy coordinator for Richard Nixon’s successful presidential campaign. From 1974 to 1977, he served as the Chairman of the Council of Economic Advisers under President Gerald Ford, navigating the stagflation crises of the mid-1970s. In 1983, President Ronald Reagan appointed him to lead the bipartisan National Commission on Social Security Reform, whose eventual recommendations successfully rescued the system from imminent insolvency.

In August 1987, Reagan selected Greenspan to succeed Paul Volcker as Chairman of the Federal Reserve. Volcker had broken the back of double-digit inflation through a series of brutal, high-interest-rate recessions, leaving Greenspan with an institution that possessed hard-won, but highly fragile, credibility.

The Fed Chairmanship: Crisis and the Golden Era (1987–2006)

Greenspan’s leadership was tested almost immediately. On October 19, 1987—just two months into his tenure—the stock market suffered its worst single-day drop in history, a crash known as "Black Monday." The Dow Jones Industrial Average plunged 22.6% in a single session.

Greenspan reacted with speed and institutional force. The following morning, before the markets opened, he issued a brief, single-sentence statement:

"The Federal Reserve, consistent with its responsibilities as the Nation’s central bank, affirmed today its readiness to serve as a source of liquidity to support the financial and economic system."

The Fed aggressively injected reserves into the banking system, preventing a systemic credit freeze. Within days, the markets stabilized, establishing Greenspan’s reputation as a master crisis manager. This episode also birthed the concept of the "Greenspan Put"—the widespread market belief that the Federal Reserve would always step in to lower interest rates or inject liquidity to cushion significant declines in asset prices.

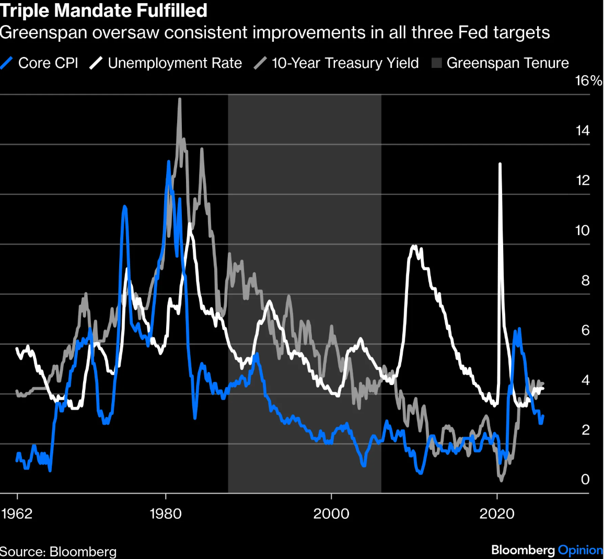

This implicit safety net underwrote the longest economic expansion in American history, which ran from March 1991 to March 2001. Throughout the 1990s, Greenspan defied traditional economic orthodoxy. As the unemployment rate steadily fell, mainstream economists urged him to raise interest rates to prevent an inevitable spike in inflation, as dictated by the traditional Phillips Curve model.

Greenspan, relying on his deep reading of corporate productivity data, resisted. He correctly hypothesized that the rapid adoption of information technology and computing had fundamentally altered the American economy, boosting productivity and allowing for high employment without triggering inflationary pressures. His intellectual courage during this period allowed millions of Americans to find work who might otherwise have been sidelined by premature rate hikes.

By the turn of the millennium, Greenspan’s reputation had reached its peak. He was widely credited with successfully navigating the 1997 Asian financial crisis, the 1998 Russian debt default, and the subsequent near-collapse of the mega-hedge fund Long-Term Capital Management (LTCM).

The Post-Fed Era and the Great Reckoning (2006–Present)

Greenspan retired from the Federal Reserve in January 2006, succeeded by Ben Bernanke. He immediately returned to the private sector, founding Greenspan Associates, commanding high fees on the international speaking circuit, and publishing his bestselling memoir, The Age of Turbulence, in 2007.

However, his retirement was quickly overshadowed by the onset of the 2007–2008 global financial crisis. The collapse of the subprime mortgage market and the subsequent failure of major investment banks like Lehman Brothers shone a harsh light on Greenspan’s regulatory legacy. As a committed deregulator, he had championed the 1999 repeal of the Glass-Steagall Act (via the Gramm-Leach-Bliley Act) and had repeatedly blocked efforts to regulate the ballooning market for over-the-counter financial derivatives, most notably dismissing the warnings of Commodity Futures Trading Commission (CFTC) Chair Brooksley Born in the late 1990s.

In October 2008, Greenspan was called to testify before the House Committee on Oversight and Government Reform. In a highly publicized exchange with Representative Henry Waxman, Greenspan admitted that he had made a mistake in his free-market ideology:

"I made a mistake in presuming that the self-interests of organizations, specifically banks and others, were such that they were best capable of protecting their own shareholders and their equity in the firms," Greenspan testified. He acknowledged that he had found a "flaw" in the model that he had assumed defined how the world worked.

In 2013, he published The Map and the Territory, an analytical attempt to reconcile his economic models with the behavioral realities and systemic blind spots exposed by the Great Recession.

Supporting Data: The Quantitative Record of the Greenspan Era

To fully comprehend the scale of Greenspan’s impact, one must look at the quantitative indicators that defined his eighteen and a half years at the helm of the Federal Reserve.

| Economic Indicator | Value / Metric | Context & Significance |

|---|---|---|

| Tenure Length | 18 Years, 173 Days | The second-longest tenure of any Fed Chair in history (behind William McChesney Martin). |

| Black Monday Crash (1987) | -22.61% | Single-day percentage drop in the Dow Jones; Greenspan’s first major policy intervention. |

| 1990s Economic Expansion | 120 Months | The longest recorded peacetime economic expansion in U.S. history up to that point. |

| Unemployment Rate (2000) | 3.8% | The lowest unemployment rate achieved during his tenure without triggering inflation. |

| Core Inflation (1990s Average) | ~2.5% | Kept inflation highly stable, defying traditional Phillips Curve predictions. |

| Federal Funds Rate Peak | 9.75% (1989) | Inherited high rates from the Volcker era; steadily managed down to support growth. |

| Federal Funds Rate Low | 1.00% (2003–2004) | Reduced rates to historic lows post-9/11, a move critics argue fueled the housing bubble. |

Federal Funds Target Rate (1987 – 2006)

During his tenure, Greenspan aggressively adjusted the Federal Funds Target Rate to manage economic cycles, demonstrating both his willingness to cut rates during crises and his cautious approach to tightening during expansions.

[1987] Appointed (FFR ~ 6.75%)

│

[1989] Aggressive Tightening Peak (FFR reaches 9.75% to curb inflation)

│

[1992] Post-Recession Easing (FFR lowered to 3.00% to stimulate recovery)

│

[2000] Dot-Com Bubble Peak (FFR raised to 6.50% to cool "irrational exuberance")

│

[2003] Post-9/11 & Dot-Com Bust (FFR slashed to historical low of 1.00%)

│

[2006] Retirement (FFR systematically raised back to 4.50% by end of tenure)Official Responses and Historical Appraisals

The announcement of Greenspan’s passing at the age of 100 brought forth a wide array of reflections from prominent figures in global economics, politics, and journalism, highlighting the dual nature of his historical legacy.

Statements from Successors and Colleagues

Ben Bernanke, who succeeded Greenspan as Federal Reserve Chairman in 2006 and led the central bank through the subsequent financial crisis, issued a balanced tribute:

"Alan Greenspan was a monumental figure in the history of central banking. He guided the nation through two decades of remarkable prosperity, demonstrating an extraordinary, empirical understanding of the American economy. While our profession continues to debate the regulatory paradigms of his era, there is no question that his intellectual leadership and public service left an indelible mark on the global financial architecture."

Andrea Mitchell, the veteran NBC News Chief Foreign Affairs Correspondent and Greenspan’s wife of nearly three decades, announced his passing with a statement reflecting his personal character:

"Alan was a giant of a man who loved his country, dedicated his life to public service, and remained deeply passionate about the discipline of economics until his very last days. He was a brilliant thinker, a loving husband, and a man who, even when his policies faced intense scrutiny, was honest enough to publicly confront his own mistakes and engage with his critics."

Institutional and Critical Assessments

In contrast to the warm personal tributes, institutional reports and critical economists have offered a more severe assessment of his long-term policy impacts. The Financial Crisis Inquiry Commission (FCIC), established by Congress to investigate the causes of the 2008 financial collapse, concluded in its 2011 report:

"The sentinel was not at his post. We find that the pivotal failure was a failure of regulatory supervision, championed significantly by Federal Reserve Chairman Alan Greenspan, who consistently advocated for self-regulation and systematically stripped away the regulatory safeguards that could have prevented the systemic collapse of the mortgage market."

Nobel laureate and economist Joseph Stiglitz has frequently pointed out the systemic risks structuralized under Greenspan’s watch:

"Greenspan’s legacy is one of short-term stability purchased at the price of long-term instability. By keeping interest rates too low for too long in the early 2000s and actively blocking the regulation of credit default swaps and other derivatives, he created a toxic environment of moral hazard that eventually brought the global economy to its knees."

Implications: The Legacy and Evolution of Central Banking

The passing of Alan Greenspan offers an opportunity to analyze how his style of leadership, communication, and economic philosophy fundamentally reshaped the practice of central banking.

The Rise and Fall of "Fed Speak"

Perhaps Greenspan’s most recognizable cultural contribution was his unique style of public communication, which became known as "Fed Speak." Recognizing that a single clear word from a Federal Reserve Chairman could instantly destabilize global markets, Greenspan deliberately constructed his public testimonies and speeches with dense layers of qualifications, passive verbs, and syntactical ambiguity.

He famously joked about this obfuscation during a congressional hearing:

"I know you believe you understand what you think I said, but I am not sure you realize that what you heard is not what I meant."

While "Fed Speak" allowed Greenspan to preserve maximum policy flexibility and avoid prematurely committing the Fed to specific rate paths, it also created an environment of intense, sometimes absurd speculation. Market participants scrutinized everything from the thickness of his briefcase on meeting days (the "Briefcase Indicator") to the subtle shifts in his adjectives.

In the years since his departure, subsequent Fed Chairs—including Ben Bernanke, Janet Yellen, and Jerome Powell—have systematically dismantled "Fed Speak" in favor of "forward guidance." Modern central banking now prioritizes clear, explicit communication regarding interest rate projections, economic targets, and balance sheet policies. The deliberate opacity championed by Greenspan has been replaced by a belief that clear communication is itself a highly effective tool for stabilizing markets.

=========================================

EVOLUTION OF CENTRAL BANK COMMUNICATION

=========================================

[ GREENSPAN ERA ] [ MODERN ERA ]

"Fed Speak" "Forward Guidance"

───────────────────────────── ─────────────────────────────

• Deliberate opacity & ambiguity • High transparency & clarity

• Avoided explicit commitments • Explicit target-setting (e.g., 2% inflation)

• Kept markets guessing • Published "Dot Plots" of rate expectations

• Preserved maximum flexibility • Managed expectations to prevent shocksThe Moral Hazard of the "Greenspan Put"

The concept of the "Greenspan Put" remains one of the most critical structural legacies of his tenure. By repeatedly intervening to lower interest rates and inject liquidity whenever major financial market disruptions occurred—such as the 1987 crash, the 1998 LTCM collapse, and the post-9/11 downturn—Greenspan inadvertently signaled to Wall Street that the downside risks of aggressive financial speculation would be socialized, while the upside gains remained private.

This dynamic created a profound issue of moral hazard. Financial institutions, operating under the assumption that the Federal Reserve would always step in to rescue the markets if conditions deteriorated, engaged in increasingly risky behavior, culminating in the subprime mortgage boom.

Modern central banks continue to grapple with the legacy of the "Greenspan Put." Every major liquidity intervention since—including the massive quantitative easing programs during the 2008 financial crisis, the COVID-19 pandemic, and the 2023 regional banking crisis—is viewed by critics as an extension of the precedent established by Greenspan in October 1987.

The Twilight of Laissez-Faire Central Banking

Ultimately, Greenspan’s intellectual journey mirrors the broader trajectory of economic thought over the past four decades. He entered public service at a time when the economic consensus was shifting rapidly toward deregulation, privatization, and an unshakeable faith in the efficiency of free markets. His policies reflected this consensus, helping to unleash a wave of financial innovation and globalization that generated immense wealth and pulled inflation down worldwide.

Yet, the systemic failures of 2008 demonstrated that markets are not always self-correcting, that financial institutions do not always act in their own long-term self-interest, and that the absence of regulation can lead to catastrophic failures. Greenspan’s public admission of a "flaw" in his worldview remains one of the most intellectually honest, yet tragic, moments in modern public policy.

As the "Maestro" takes his final bow, the discipline of economics continues to navigate the complex territory he mapped. He was a historic figure who guided his country through decades of unparalleled prosperity, but whose fundamental beliefs were tested, and ultimately broken, by the very forces of financial dynamism he sought to unleash.