In a fundamental shift of the Federal Reserve’s traditional operating philosophy, new Fed Chair Kevin Warsh is charting a course that prioritizes market-driven interest rate discovery over central bank micromanagement. As real yields—the interest rates adjusted for inflation—surge past significant psychological thresholds, it is becoming increasingly clear that the "Warsh Doctrine" is designed to empower the bond market to do the heavy lifting of monetary policy.

This transition marks a departure from the era of heavy-handed forward guidance, suggesting that under Warsh’s leadership, the Federal Reserve will serve more as a responsive observer of economic data than an arbiter of borrowing costs. As Treasury Inflation-Protected Securities (TIPS) hit multi-year highs, the financial landscape is undergoing a rigorous recalibration.

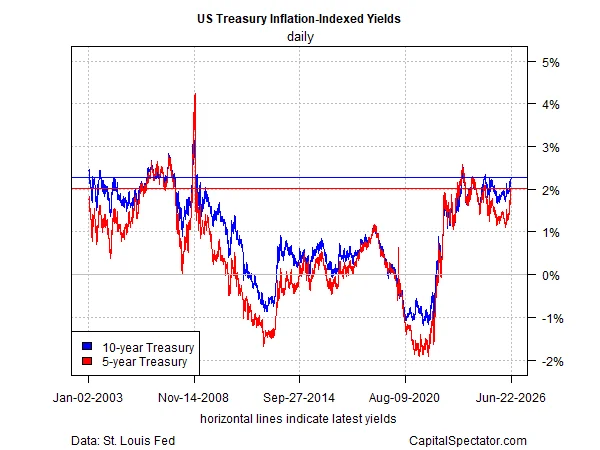

The Chronology of a Yield Surge

The recent climb in real yields is not an isolated event but the culmination of several months of inflationary pressure and geopolitical instability. To understand the current environment, one must look at the rapid ascent of TIPS across the maturity curve.

Early 2026: The Baseline

As recently as February 27, the 5-year real yield stood at a modest 1.11%. At that time, the bond market was still operating under a regime of relative calm, pricing in a gradual path for interest rates.

The Geopolitical Catalyst

The geopolitical landscape shifted dramatically with the outbreak of the conflict involving Iran. The subsequent spike in global energy prices served as a primary catalyst for a broad-based inflation surge. This shock wave rippled through the bond markets, forcing investors to demand higher compensation for the risk of purchasing power erosion.

The June 2026 Inflection Point

By mid-June, the narrative had shifted toward aggressive pricing. At the close of trading on June 16, the 5-year TIPS yield breached the 2.0% threshold for the first time in over a year. This was not a localized phenomenon; the 10-year TIPS climbed to 2.13%, and the 30-year yield reached 2.75%. This upward movement across the curve indicates that the market is not merely reacting to short-term volatility, but is fundamentally repricing the long-term cost of capital in a post-inflationary environment.

Supporting Data: Understanding Real Yields

Real yields are arguably the most important metric for understanding the "true" cost of money in an economy. While nominal rates tell us what borrowers pay, real rates reveal the actual burden on the economy after inflation is stripped away.

The current move above 2% for the 5-year TIPS is significant because it signals a transition from "accommodative" to "restrictive" financial conditions. When real yields remain low, they encourage borrowing and speculative investment. When they push above the 2% mark, they serve as a natural brake on economic activity.

Market analysts note that the current structure of the yield curve is reflecting a "data-dependent" reality. Investors are no longer waiting for the FOMC to hold a press conference to decide the direction of the economy; they are actively discounting incoming data—such as CPI reports, energy futures, and geopolitical stability—directly into the price of Treasury securities.

The Warsh Doctrine: A Paradigm Shift

Kevin Warsh’s first press conference as Fed Chair served as a manifesto for this new era. His commentary was characterized by a hawkish tone that resonated sharply with institutional investors. Warsh noted that inflation has consistently outperformed the Fed’s 2% mandate for over five years, describing the situation as a persistent burden on the American public.

The "Market-First" Philosophy

Warsh’s approach is rooted in the belief that "financial markets perform best when they react to incoming data." This is a stark pivot from the "Fed-speak" era, where market participants spent their time deciphering the nuances of central bank language rather than analyzing the economy itself.

Warsh argued that the more markets focus on the real economy—discerning the quality of data and weighing tail risks—the more efficient the pricing of capital becomes. By allowing the bond market to lead, Warsh believes the Federal Reserve can avoid the pitfalls of policy error that characterized the previous decade, where the central bank often kept rates too low for too long, fueling asset bubbles.

Official Responses and Political Context

The interplay between the White House and the Federal Reserve remains a focal point for market participants. Vice President Vance recently provided a note of cautious optimism, reporting "great progress" in ongoing diplomatic talks with Iran. This development has provided a glimmer of hope that the geopolitical premium embedded in energy prices—and by extension, inflation expectations—could soon begin to dissipate.

However, the Fed remains in a delicate position. While headline inflation remains elevated due to energy volatility, core inflation (which strips out volatile food and energy components) has shown signs of being more subdued. This dichotomy creates a difficult policy environment:

- The Case for Hikes: If the market continues to drive real yields higher, the Fed may feel empowered to hold rates steady, knowing the market is already tightening financial conditions on their behalf.

- The Case for Patience: If energy prices collapse following a peaceful resolution in the Middle East, the Fed must be careful not to overtighten based on the transitory shocks of the last few months.

Implications for Investors and the Economy

For the average investor, the era of "free money" appears to be firmly in the rearview mirror. The ability to secure a real yield of 2% or higher on government-backed debt makes TIPS an increasingly attractive component of a diversified portfolio. For over a decade, fixed-income investors were forced to move further out on the risk curve to find any semblance of return; the current environment offers a rare opportunity to capture real value in lower-risk assets.

Risks and Future Outlook

Despite the current trends, the path forward is fraught with uncertainty. The primary question facing bond traders is whether the current rise in real yields is sustainable or if it is merely a "reactionary spike."

If the conflict with Iran concludes quickly and energy prices retreat, we may see a "bull steepener" in the bond market—where long-term yields fall as growth expectations cool. Conversely, if inflationary pressures have become "entrenched" in the service sector and wage growth, the 2% threshold in real yields may only be the floor, not the ceiling.

Furthermore, the Fed’s willingness to stay on the sidelines while the market drives rates higher could lead to increased volatility. Without the "Fed Put"—the assumption that the central bank will intervene to stop a market decline—investors must be prepared for a more turbulent environment.

Conclusion

The appointment of Kevin Warsh marks the beginning of a significant experiment in modern central banking. By fostering an environment where the bond market dictates the cost of credit, Warsh is attempting to restore the Federal Reserve to its role as a steward of stability rather than an engine of market momentum.

As we look toward the upcoming FOMC meetings, the focus will shift from the Chair’s words to the bond market’s actions. Investors are now watching the TIPS curve with renewed intensity, understanding that the real cost of capital is no longer a decision made in a boardroom, but a verdict rendered by the collective wisdom—and anxiety—of the global financial markets. The "bond ghouls," as they are sometimes affectionately called, are once again in the driver’s seat, and the road ahead promises to be defined by the hard data of a complex, evolving global economy.