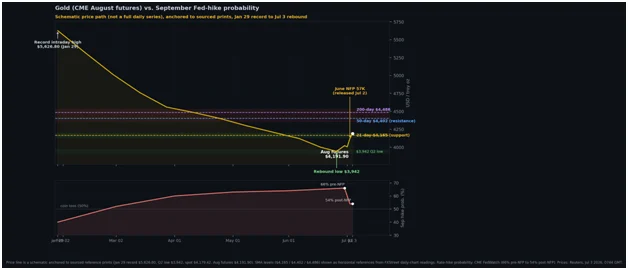

The global gold market, often viewed as the ultimate barometer of investor sentiment toward central bank policy, has staged a notable relief rally this week. Triggered by a significantly weaker-than-anticipated U.S. non-farm payrolls (NFP) print, gold prices surged as market participants recalibrated their expectations for Federal Reserve interest rate policy. As of July 3, 2026, August gold futures climbed 1.6% to reach $4,191.90, while spot XAU/USD rose 1.4% to $4,179.42—marking a six-day high and placing the precious metal on track for its first weekly gain since late May.

This rally, while substantial, represents more than a mere flight to safety; it is a fundamental reassessment of the "higher-for-longer" interest rate regime that has dominated financial markets throughout the second quarter of 2026.

Main Facts: A Payroll Miss Rewrites the Script

The catalyst for this week’s gold bid was the U.S. Bureau of Labor Statistics (BLS) report, which revealed that the economy added only 57,000 jobs in June. This figure stands in stark contrast to the consensus expectation of 110,000, representing the slowest pace of hiring in four months.

Accompanying the headline miss, the unemployment rate ticked down to 4.2%, a move largely explained by a contraction in labor force participation rather than a surge in hiring. Average hourly earnings, a key metric for inflationary pressure, grew by 3.5% year-over-year. For gold, a non-yielding asset, the importance of these numbers cannot be overstated: when the labor market softens, the pressure on the Federal Reserve to implement aggressive rate hikes dissipates. Consequently, the "opportunity cost" of holding gold—which typically rises alongside Treasury yields—has diminished, allowing the metal to reclaim lost ground.

Chronology: The Evolution of the Trade

The market’s path to this week’s rally was paved by a sequence of increasingly cautious economic signals:

- Mid-Week Signaling: The tone for the government’s Friday release was set on Wednesday by private-sector payroll data, which suggested a cooling trend in corporate hiring. This preliminary read created an undercurrent of skepticism regarding the strength of the labor market heading into the BLS report.

- The Friday Print: Upon the release of the 57,000-job figure, the reaction was immediate. Within hours, the probability of a Federal Reserve rate hike in September plummeted from 66% to 54%, according to the CME FedWatch Tool.

- The Currency and Yield Pivot: As rate hike odds moved toward a coin-flip, the U.S. Dollar Index (DXY) retreated to a two-week low. Simultaneously, Treasury yields eased, effectively removing the primary headwinds that had suppressed gold prices throughout the June sell-off.

- Technical Reclamation: By the end of the trading week, gold had successfully reclaimed its 21-day simple moving average (SMA) at $4,165.03, a critical technical threshold that had previously served as a ceiling for upside momentum.

Supporting Data: Mapping the Macro Inputs

The correlation between macroeconomic variables and gold’s price action has been exceptionally tight this quarter. The following table illustrates the shift in market conditions pre- and post-NFP:

| Signal | Pre-NFP | After NFP | Impact on Gold |

|---|---|---|---|

| Sept. Hike Odds | 66% | 54% | Bullish |

| Non-Farm Payrolls | 110K (Expected) | 57K (Actual) | Bullish |

| U.S. Dollar | Firm | Weaker | Bullish |

| Treasury Yields | Elevated | Eased | Bullish |

| 21-Day SMA | Below | Above | Supportive |

This shift demonstrates that gold’s recovery is not merely speculative; it is structurally tied to the easing of the "tight-money" constraints that have defined the 2026 fiscal environment.

Official Responses and Monetary Policy Context

The Federal Reserve’s stance remains the central pillar upon which the gold market rests. Earlier this week, at the European Central Bank’s forum in Sintra, new Fed Chair Kevin Warsh provided a nuanced perspective on the current economic landscape. Warsh acknowledged the progress made in easing inflation expectations while reiterating a firm commitment to price stability.

Analysts interpret Warsh’s remarks as a signal that the Fed is no longer operating on "autopilot" regarding rate hikes. Instead, the central bank appears to be entering a data-dependent phase where each monthly report—especially labor and wage data—will dictate the immediate trajectory of monetary policy. This shift in rhetoric has empowered gold investors, who view the potential for a "dovish pivot" as the primary driver for future gains.

Furthermore, market analysts, including OANDA’s Kelvin Wong, have noted that while the repricing of rate hikes extends into early next year, the risk of a "leg down" remains if incoming data surprises to the upside. The market is currently balanced on a knife’s edge, waiting to see if June’s labor softening is an anomaly or the beginning of a sustained trend.

Structural Demand: The Role of Central Banks

While tactical traders react to payroll numbers and rate probabilities, a more profound, long-term support layer is being provided by global central banks. According to the World Gold Council, central banks returned to net-buying in May, adding 41 tons to official reserves.

This institutional demand acts as a "hard floor" for the market. Poland’s National Bank led the charge with an 18-ton acquisition, continuing its strategic push toward a 700-ton target. China, Uzbekistan, and Kazakhstan also reported significant additions. The World Gold Council projects 850 tons of central bank purchases for 2026, a figure that remains well above historical averages. Because this demand is driven by long-term reserve diversification strategies rather than short-term price volatility, it provides a crucial buffer during periods of market stress, preventing deep technical sell-offs from becoming full-scale collapses.

Implications: Navigating the Road Ahead

For investors, the current market structure presents a complex, conditional landscape. Gold has successfully exited its immediate oversold condition, but it remains in a broader "countertrend" phase.

The Technical Outlook

The 50-day SMA, currently situated at $4,402.46, represents the next major hurdle. A weekly close above this level would provide the first significant technical evidence that the corrective phase is over. Conversely, failure to maintain the 21-day SMA support at $4,165.03 could see the metal retest the lows seen earlier this year near $3,942.

Scenario Analysis

- The Hawkish Trap: Should July economic data surprise with renewed strength, and if FOMC officials pivot back toward inflation-fighting rhetoric, the September hike odds could climb back to 66%. Under this scenario, gold would likely face renewed downward pressure, testing the $4,000 support level.

- The Base Case: If the labor market continues to soften at a measured pace, and the Fed maintains its "coin toss" approach to September, gold will likely consolidate between the 21-day and 50-day moving averages, allowing for a gradual technical repair.

- The Dovish Upside: A continuation of the current cooling trend—characterized by further weak payroll prints—would likely lead to the total removal of September hike expectations. This environment would provide the perfect conditions for gold to test the 200-day SMA at $4,486 and potentially challenge higher resistance levels.

Conclusion: Data-Dependent Reality

Gold’s recent performance underscores a market in transition. While the tactical move this week was driven by the "rate channel"—the interplay between the dollar, Treasury yields, and Fed expectations—the underlying structural support provided by central banks offers a safety net for long-term holders.

Ultimately, the durability of this recovery rests in the hands of the U.S. labor market. Investors should monitor the upcoming July and August payroll data closely, as these reports will serve as the final arbiters for the Fed’s September meeting. Until then, gold remains a sensitive instrument, tethered to the data that will ultimately define the next chapter of global monetary policy.

Disclaimer: This analysis is provided for informational purposes only and does not constitute financial advice, an offer to sell, or a solicitation of an offer to buy any securities or commodities. Market participants should perform their own due diligence and consult with a licensed financial advisor before making any investment decisions. Prices and technical indicators cited were accurate at the time of writing and remain subject to the inherent volatility of global financial markets.