Governments possess the constitutional authority to rewrite budgets, restructure tax codes, and replace Prime Ministers. What they cannot do, however, is negotiate with the global bond market.

Over the past decade, the United Kingdom has served as a stark laboratory for a fundamental macroeconomic truth: political capital is finite, but the demands of debt arithmetic are absolute. Since the historic Brexit referendum in 2016, Downing Street has experienced an unprecedented revolving door of leadership. This level of political volatility—traditionally associated with emerging economies undergoing structural crises rather than one of the world’s premier financial hubs—underscores a deeper systemic challenge.

Every administration has arrived at Number Ten promising a fresh economic vision. Yet, regardless of political ideology, each has ultimately collided with the same fiscal wall. The UK has grown accustomed to a level of public spending that its structural growth rate cannot comfortably support, even as global investors have become progressively less willing to finance those deficits at the rock-bottom interest rates of the previous decade.

While political analysts naturally dissect the personalities, errors, and strategic choices of individual leaders, these factors alone cannot explain why vastly different administrations keep arriving at the same fiscal dead end. The explanation lies in the sovereign debt markets—a quiet, mathematically driven force that exerts a silent, binding veto over modern democracy.

Chronology: The Great Fiscal Collision (2016–Present)

To understand how the bond market became the ultimate arbiter of British politics, one must trace the timeline of leadership transitions and the fiscal realities that precipitated them.

[2016: Brexit Referendum] ➔ [May: Negotiating Deadlock] ➔ [Johnson: Fiscal Expansion]

│

[Starmer: Fiscal Realism] ◄─ [Sunak: Emergency Stabilization] ◄─ [Truss: Bond Market Veto (2022)]2016–2019: The Post-Referendum Paralysis

Following the 2016 Brexit vote, David Cameron resigned, passing a highly fractured political landscape to Theresa May. May’s premiership became consumed by complex divorce negotiations with the European Union—variables she could describe but never fully control. During this period, economic uncertainty suppressed private investment, forcing the state to rely heavily on public spending and ultra-low interest rates maintained by the Bank of England to sustain growth.

2019–2022: The Covid-19 Fiscal Shock

Boris Johnson secured a historic 80-seat parliamentary majority in late 2019, seemingly granting him the mandate to pursue an ambitious "levelling up" agenda. However, the arrival of the COVID-19 pandemic necessitated unprecedented emergency fiscal interventions. The UK Treasury financed massive furlough schemes and business support packages through massive debt issuance, which was quietly absorbed by the Bank of England’s quantitative easing (QE) program. By the time Johnson departed in mid-2022, the UK’s national debt-to-GDP ratio had crossed the threshold of 100%, leaving the state highly vulnerable to interest rate shocks.

Autumn 2022: The Truss Crisis and the "Bond Vigilante" Return

In September 2022, Liz Truss and her Chancellor, Kwasi Kwarteng, unveiled a "Mini-Budget" featuring £45 billion of unfunded tax cuts alongside massive energy subsidies. The administration bypassed the independent Office for Budget Responsibility (OBR) and failed to outline how these cuts would be financed.

The reaction from the bond market was immediate and devastating. Investors dumped UK government bonds (gilts), causing yields to spike at speeds never before seen in modern British history. Within days, the rapid depreciation of gilts threatened the solvency of British pension funds, forcing the Bank of England to launch a £65 billion emergency bond-buying program. Truss’s premiership collapsed after just 49 days—a vivid demonstration of the market’s veto power.

2022–Present: The Era of Fiscal Realism

Rishi Sunak inherited the economic wreckage, spending his tenure implementing tax increases and spending restraints to restore market confidence. When Keir Starmer’s Labour government swept to power in 2024, the administration was forced to immediately abandon many of its structural spending ambitions, declaring that there was "no money left." Starmer’s government quickly joined its predecessors in acknowledging that the debt auction calendar, managed by the Debt Management Office (DMO), dictates domestic policy far more than any debate in the House of Commons.

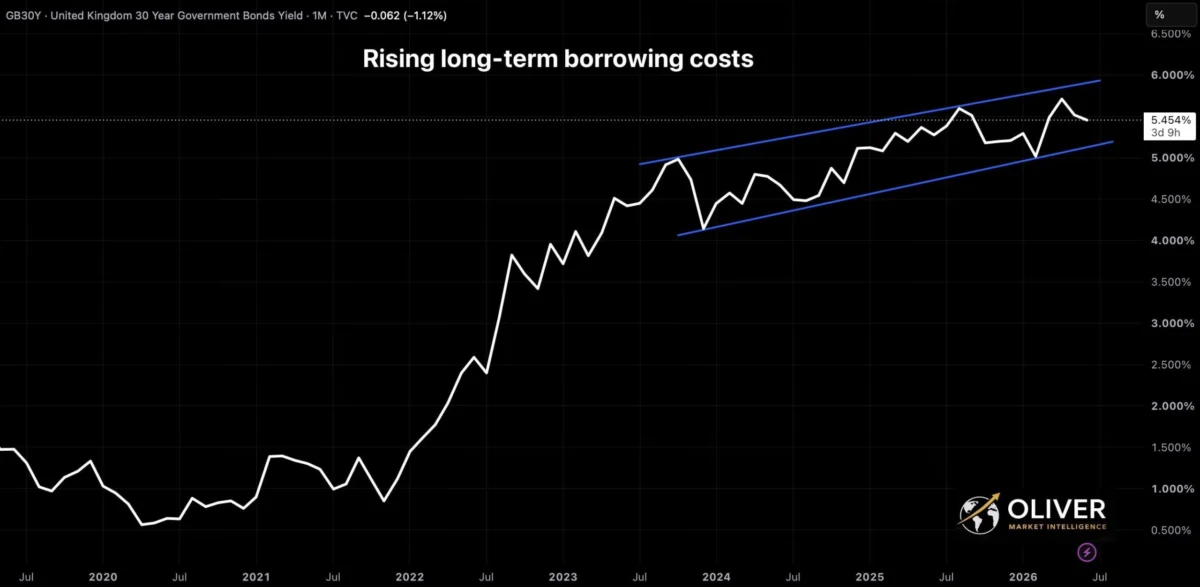

Supporting Data: The Rising Cost of Debt

The shift in the global macroeconomic landscape is best illustrated by the hard data tracking sovereign borrowing costs and debt accumulation.

For nearly fifteen years following the 2008 financial crisis, the UK operated in an artificial economic environment. Interest rates hovered near zero, and the Bank of England purchased more than £800 billion of government debt through QE. This insulated the Treasury from the true cost of its borrowing.

Global Gilt Yield Trajectory (Conceptual)

Yield %

│

5│ /

4│ / (Present Era: High Refinancing Costs)

3│ / _______

2│ /

1│ ____________/

0└───────────────────────────────────

2010-2021 2022 Crisis 2024+

(Cheap Money) (Truss Shock) (The New Normal)Today, that insulation has completely dissolved. As older, low-interest government debt matures, the Treasury must refinance it by issuing new gilts at prevailing market rates.

Key Fiscal Metrics:

- The Yield Shift: Ten-year UK gilt yields, which averaged less than 1% during the pandemic, spiked above 4.5% during the 2022 mini-budget crisis and have remained structurally elevated between 3.8% and 4.4% throughout 2023 and 2024.

- The Refinancing Burden: According to the Office for Budget Responsibility (OBR), the UK’s debt interest bill reached over £110 billion in 2023—representing more than 10% of total tax revenues. This is more than the government spends on education or defense.

- Inflation-Linked Pressures: Unlike many other developed nations, approximately 25% of the UK’s outstanding national debt is linked to the Retail Prices Index (RPI). When inflation surged into double digits in 2022 and 2023, the capital value of these bonds adjusted upward, immediately compounding the Treasury’s interest obligations.

Official Responses and Institutional Interventions

The structural tension between political ambition and market reality has forced key state institutions into unprecedented, often contradictory, interventions.

The Bank of England’s Dual Mandate

During the September 2022 crisis, the Bank of England found itself in a deeply compromised position. While it was actively raising interest rates to combat double-digit inflation, it was simultaneously forced to launch an emergency bond-buying operation to prevent a systemic collapse of the UK pension sector (specifically targeting Liability-Driven Investment, or LDI, funds).

In official statements, Governor Andrew Bailey emphasized that the intervention was a temporary financial stability measure, not a return to monetary easing:

"We had to intervene to restore market functioning, but let there be no doubt: monetary policy is designed to bring inflation back to target, and fiscal policy must align with that reality."

The Office for Budget Responsibility (OBR)

The OBR, established in 2010 to provide independent economic forecasts, has become the de facto gatekeeper of fiscal credibility. Under intense scrutiny following the 2022 crisis, the OBR has consistently warned that the UK’s long-term fiscal path is unsustainable without major structural reforms. In its recent Fiscal Risks and Sustainability reports, the OBR noted that demographic pressures—including an aging population, rising healthcare costs, and a shrinking workforce—will push public debt toward 270% of GDP over the next fifty years if current policy trajectories remain unchanged.

Global Implications: A Shared Sovereign Debt Crisis

The UK is not an isolated case; it is merely the canary in the coal mine. Across the developed world, the era of unconstrained fiscal expansion is running headlong into the reality of structurally higher interest rates.

┌─────────────────────────────────────────────────────────────────────────┐

│ GLOBAL SOVEREIGN DEBT TRAPS │

├─────────────────┬───────────────────────────────────────────────────────┤

│ United States │ • National debt exceeds $34 trillion. │

│ │ • Interest payments exceed $1 trillion annually. │

│ │ • Structurally high deficits despite high employment. │

├─────────────────┼───────────────────────────────────────────────────────┤

│ Japan │ • Debt-to-GDP ratio exceeds 260%. │

│ │ • BoJ forced to abandon negative interest rates. │

│ │ • Rising yields strain domestic banks and pensions. │

├─────────────────┼───────────────────────────────────────────────────────┤

│ Eurozone │ • Weak growth coupled with high defense spending. │

│ │ • Stricter enforcement of fiscal rules. │

│ │ • Widening spreads between German and southern bonds. │

└─────────────────┴───────────────────────────────────────────────────────┘In the United States, the federal budget deficit continues to expand despite the economy operating close to full employment. The Congressional Budget Office (CBO) estimates that net interest costs on federal debt will double over the next decade, consuming an ever-larger portion of the federal budget.

Similarly, Japan is navigating the delicate exit from its long-standing Yield Curve Control (YCC) policy. As the Bank of Japan permits domestic yields to rise, the cost of servicing Japan’s massive debt-to-GDP ratio (which exceeds 260%) threatens to squeeze out standard government expenditures.

Global capital has become increasingly selective. Investors who once viewed all developed-market sovereign bonds as risk-free assets are now actively differentiating between nations with credible fiscal pathways and those relying on optimistic growth assumptions.

The "Quiet Tax" and the Flight to Hard Assets

When governments find themselves unable to reduce their liabilities through politically unpalatable spending cuts or tax increases, history points to a time-tested alternative: inflation.

Inflation as a Debt-Devaluation Tool

Often referred to by economists as "financial repression," sustained inflation allows a state to pay down its fixed nominal liabilities with tomorrow’s devalued currency. While this process temporarily eases the pressure on the Treasury’s balance sheet, it acts as a silent tax on the private sector. It systematically erodes the purchasing power of cash savers and fixed-income investors, shifting wealth from the public to the state without requiring a single vote in Parliament.

How Inflation Devalues Sovereign Debt:

[High Nominal Debt] + [Sustained Inflation] ➔ [Erosion of Currency Value] ➔ [Reduced Real Debt Value]

│

[Erosion of Private Savings] ◄┘The Resurgence of Gold and Hard Assets

As confidence in the long-term purchasing power of fiat currencies begins to waver, both institutional and private investors are adjusting their portfolios. For decades, sovereign bonds were considered the ultimate safe-haven asset, offering liquidity, security, and a modest yield. In a regime of negative real interest rates (where inflation outpaces nominal yields), that assumption no longer holds.

Central Bank Net Gold Purchases (Metric Tonnes, Annual Trends)

Tonnes

1200│

1000│ ▲ ▲

800│ ███ ███

600│ ███ ███

400│ ▲ ▲ ▲ ▲ ▲ ███ ███

200│ ███ ███ ███ ███ ███ ███ ███

0└──────────────────────────────────────

Pre-Pandemic Era Post-2022 EraThis structural shift explains the massive resurgence of gold. Unlike government bonds, physical gold carries no counterparty risk, cannot be devalued by monetary issuance, and requires no policy promises from a central bank.

Notably, central banks themselves have recognized this transition. According to data from the World Gold Council, central banks purchased over 1,000 metric tonnes of gold in both 2022 and 2023—the highest levels of official buying since the suspension of the gold standard in 1971. By diversifying reserves away from Western government debt and into physical gold, monetary authorities are quietly signaling their declining confidence in the international fiat system.

Conclusion: The Unyielding Laws of Arithmetic

The political drama in Westminster over the past decade has featured a rotating cast of characters, slogans, and policy platforms. Yet each administration has ultimately been forced to capitulate to the same underlying reality.

Political parties can win democratic mandates, but they cannot force the market to fund those mandates at a loss. Until the United Kingdom—and indeed, much of the developed world—confronts the structural imbalance between its public expectations and its fiscal capacity, the political cycle will remain trapped in this pattern.

Governments can reshuffle cabinets, rewrite budgets, and announce new policy directions. But they cannot negotiate with arithmetic. In the end, the market’s simple, unyielding question remains: can the numbers still be trusted? Increasingly, the answer to that question matters far more than whoever happens to be standing outside the door of Number Ten Downing Street.