As the summer sun warms the nation, millions of Americans are preparing to retreat to their patios and backyards for a ritual as old as the country itself: a cold beer after a long day. However, while consumers may be focused on the brand, the style, or the craft profile of their beverage, there is a silent, invisible partner sitting at the table—and it is arguably the most expensive ingredient in every glass.

The U.S. beer industry is governed by a labyrinthine, multilayered tax structure that often goes unnoticed by the average consumer. While shoppers see a final price on the shelf, that number is "baked" into the retail cost, obscuring the fact that taxes—when aggregated—can account for as much as 40.8 percent of the final price of a beer. As the industry faces shifting consumer preferences and economic headwinds, this intricate web of excise, sales, and local taxes is increasingly coming under scrutiny.

The Anatomy of the Beer Tax Burden

To understand the price of a beer, one must look past the cost of hops, barley, labor, and transportation. In the United States, the total tax burden on beer is a cumulative result of federal excise taxes, state-level excise taxes, municipal levies, and general sales taxes.

Federal Excise Taxes: The Baseline

At the federal level, the Alcohol and Tobacco Tax and Trade Bureau (TTB) manages a tiered system of excise taxes. These rates are structured to assist smaller producers, with the tax ranging from $0.113 per gallon for the first 60,000 barrels produced by small domestic brewers to $0.581 per gallon for imported beer. These taxes are paid at the source—the manufacturer or the importer—meaning they are already embedded in the price by the time the product reaches the distributor.

State-Level Variation

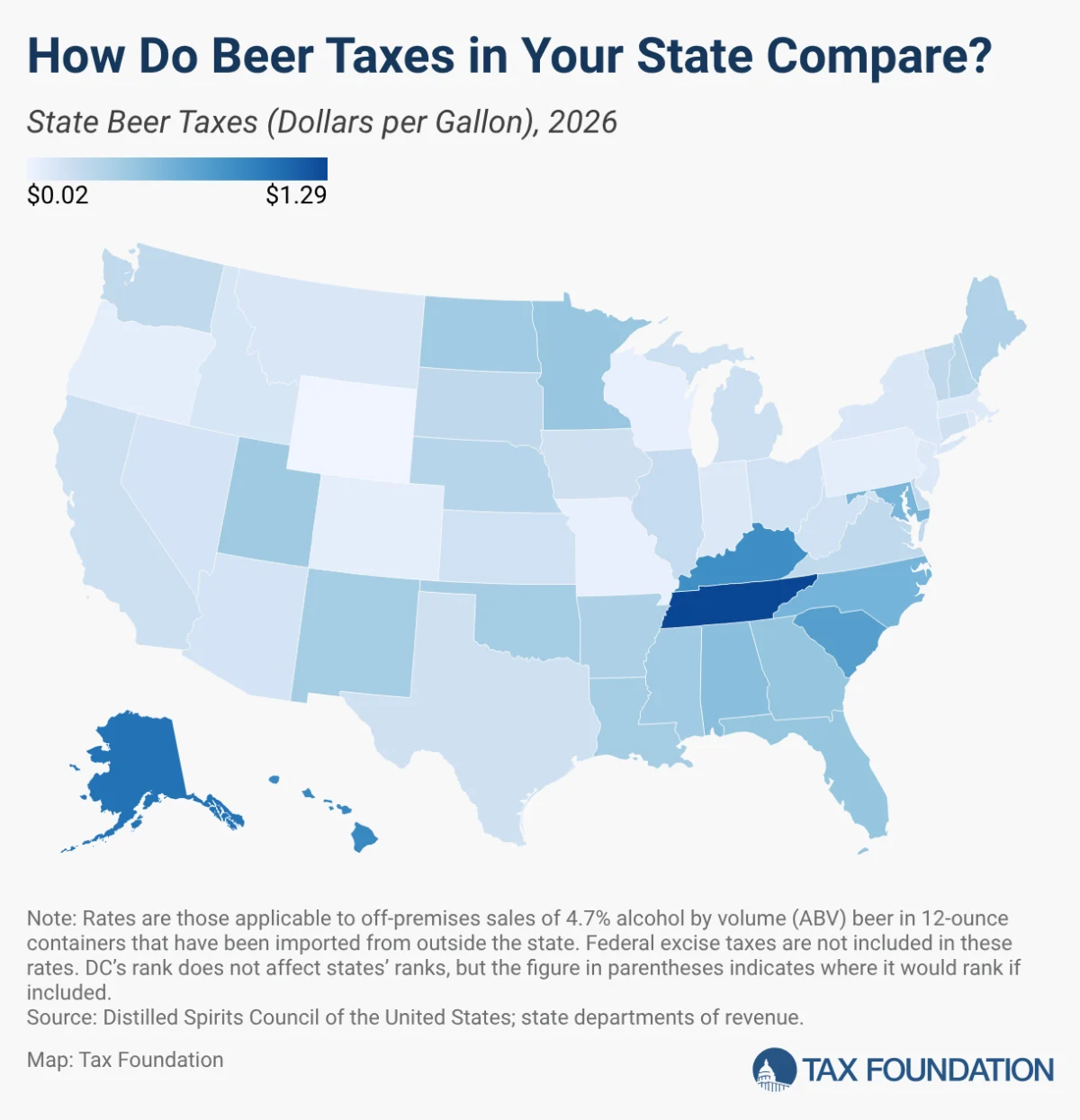

The situation becomes exponentially more complex once the product enters state jurisdiction. Every state, along with the District of Columbia, imposes its own excise tax on beer. These rates vary wildly, reflecting the disparate fiscal policies of state legislatures.

- The High-Tax Tier: States like Tennessee ($1.287 per gallon), Alaska ($1.07 per gallon), and Hawaii ($0.93 per gallon) represent the upper echelon of the tax burden. In these regions, the excise tax alone significantly inflates the per-ounce cost of the product.

- The Low-Tax Tier: Conversely, states with a more favorable regulatory environment for brewers, such as Wyoming ($0.019 per gallon), Missouri ($0.06 per gallon), and Wisconsin ($0.065 per gallon), allow for a significantly lower tax-to-retail-price ratio.

A Chronology of Regulatory Evolution

The history of alcohol taxation in the U.S. has always been tied to fiscal necessity and social policy. Following the repeal of Prohibition, the current system was designed not only to generate revenue but to maintain a controlled, observable supply chain.

The 20th Century Legacy

For decades, the system remained relatively stagnant, relying on static ad quantum (quantity-based) taxes. These taxes, however, have a fundamental flaw: they do not adjust for inflation. As the value of currency decreases, the real-dollar value of these taxes erodes, leading to periodic legislative "corrections" that often result in sudden, sharp tax hikes.

Recent Trends and 2026 Outlook

In recent years, the landscape has begun to shift toward more granular control.

- 2023–2024: Several states began re-evaluating their excise structures to encourage local economic growth. Missouri, for example, successfully pushed through legislation cutting taxes on beer manufactured in American breweries to a modest $0.02 per gallon, a move intended to stimulate the state’s craft brewing sector.

- 2025–2026: We are seeing a move toward "ABV-sensitivity." States like Idaho have set a precedent by taxing beer with an alcohol content higher than 5% at triple the rate of standard beer, treating it effectively like wine. This represents a broader trend of moving away from "categorical" taxation toward "potency-based" taxation.

Data Breakdown: The Hidden Costs

The following table illustrates the variance in tax burden across select states, highlighting how geography dictates the "invisible" portion of a consumer’s receipt.

| State | Tax Per Gallon | Contextual Note |

|---|---|---|

| Tennessee | $1.287 | Highest national excise burden |

| Alaska | $1.070 | Includes significant logistical/local premiums |

| Hawaii | $0.930 | High-cost environment, high excise |

| Wisconsin | $0.065 | Low-tax environment, strong brewing tradition |

| Missouri | $0.060 | Recent legislative cuts to support local industry |

| Wyoming | $0.019 | Lowest per-gallon tax rate in the U.S. |

Note: Data reflects tax applicable to an off-premises sale of 4.7% ABV beer in a 12-ounce container.

Official Perspectives: The Policymaker’s Dilemma

Government agencies and industry lobbyists view these taxes through vastly different lenses. For state treasuries, beer taxes are a reliable, if volatile, source of general fund revenue. Because demand for alcohol is generally inelastic, governments have historically viewed it as a "safe" target for taxation.

However, the Brewers Association and various trade groups argue that this burden is becoming unsustainable. Recent industry reports highlight that beer is currently struggling against two primary forces:

- Tariffs: Global trade volatility has increased the cost of raw materials, specifically aluminum for cans and imported specialty grains.

- Shifting Demographics: Younger consumers are increasingly gravitating toward low- or no-alcohol options, or opting for spirits and ready-to-drink (RTD) cocktails, which are often taxed differently than traditional beer.

The "Unseen" Nature of the Tax

Because these taxes are paid by the manufacturer or wholesaler, they are rarely broken out on a receipt as a "tax line item." This creates a transparency gap. When a consumer pays $15 for a six-pack, they are unaware that a significant portion of that transaction is a government levy rather than the cost of the ingredients or the brewer’s profit margin.

Implications for the Future

The current, arcane categorical system—which treats beer, wine, and spirits as distinct legal entities regardless of their actual alcohol content—is increasingly out of step with modern manufacturing.

The Argument for Modernization

Policy analysts are increasingly advocating for a move toward neutral taxation based on actual alcohol content. By taxing the ethanol rather than the liquid category, the system would become:

- Simpler: Reducing the administrative burden on small breweries that currently must navigate different tax codes based on bottle size or ABV thresholds.

- More Neutral: Removing the incentive for consumers to switch products based on arbitrary tax-induced price differences rather than quality or preference.

The Risk of Budget Gaps

For states that rely heavily on beer tax revenue, the transition to lower-alcohol consumer trends poses a structural risk. If states continue to rely on these taxes for general budget spending, they may soon face "unforeseen budget gaps." As consumption habits shift toward lower-ABV products or non-alcoholic alternatives, the revenue generated by per-gallon excise taxes will naturally decline.

Conclusion: A Toast to Transparency

As the industry navigates the complexities of the 21st century, the beer tax remains a quiet but powerful force in the American economy. While it serves as a convenient revenue stream for state and federal governments, it also acts as a drag on one of the country’s most vibrant artisanal industries.

For the average consumer, the next time you enjoy a cold beer, remember that you are not just paying for the beverage in your hand. You are participating in a century-old fiscal framework that is as complicated, layered, and occasionally bitter as the drink itself. Moving forward, a modernization of this system—shifting toward transparency and ABV-based fairness—may be the only way to ensure that this cherished American staple remains accessible and economically viable for generations to come.