While the headlines have focused on the potential for Iran to resume its status as a major global oil exporter following the easing of specific sanctions, the reality on the ground—or rather, on the water—is far more complex. Iran may have successfully navigated the legal hurdles to resume moving barrels, but the transition from "sanctioned" to "market participant" is proving to be a logistical and economic quagmire. As Tehran pushes crude into an already saturated market, it is discovering that finding a buyer is a far greater challenge than simply filling a tanker.

Main Facts: The Illusion of Export Freedom

The fundamental issue facing Iran is not the lack of oil, but the lack of demand. Since Washington provided a temporary window for Iranian exports, Tehran has acted with urgency to clear its storage tanks and push crude out of the Persian Gulf toward Asian markets. However, the global oil market is currently operating in a state of high inventory, leaving little room for Iranian supply.

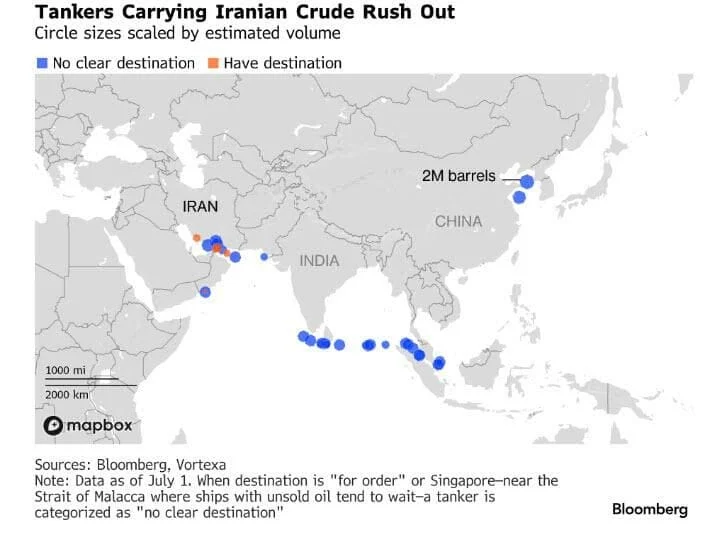

Recent data indicates that more than 58 million barrels of Iranian crude and condensate are currently floating offshore. Many of these cargoes lack a firm destination, evidenced by the high number of tankers displaying "For Orders" on their manifests. This indicates that traders are scrambling to find buyers in real-time, often resorting to quiet, back-channel negotiations involving the Malacca Strait, mid-sea storage facilities, and complex discount structures.

The core of the problem is a mismatch between supply and appetite. Iran is not merely competing against its traditional Middle Eastern rivals; it is competing against a global market that is already well-stocked. Buyers are not desperate, and the arrival of additional, discounted barrels is being met with a lukewarm reception.

Chronology: A Race Against the Clock

The current situation is defined by a rigid timeline. Iran is operating under a window of opportunity that closes roughly in mid-August. This deadline is critical for two reasons:

- Revenue Generation: Iran needs to convert its floating storage into liquid capital to bolster a struggling economy.

- Negotiation Leverage: Tehran’s ability to influence future diplomatic and economic negotiations is tied directly to its perceived strength. A nation negotiating from a position of full, idle tankers and no buyers is in a fundamentally weak position.

Key timeline milestones:

- Early Q2: Washington signals a temporary shift in enforcement, opening a window for exports.

- June: Reports indicate a sharp decline in Chinese imports of Iranian crude, marking the first sign that the initial optimism was premature.

- July: The volume of idle tankers in Asian waters begins to rise, with some cargoes remaining static for over a week—a major red flag for market observers.

- August (Upcoming): The projected closure of the current export window, which serves as a looming "doomsday" for unsold inventory.

Supporting Data: The China and India Factor

The Chinese Bottleneck

China was long considered the "natural home" for Iranian crude. Historically, independent refiners—often referred to as "teapots"—have been willing to absorb discounted barrels that state-owned entities avoid due to the risks associated with sanctions, banking, and insurance.

However, current data from the Chinese sector suggests that this reliance is misplaced. Independent refinery runs in China are currently weak. Margins are heavily compressed due to high domestic inventory levels and lackluster demand growth. When margins are thin, refiners have little incentive to chase additional, potentially "risky" barrels, even at a discount. If the Chinese teapots do not have a compelling economic reason to reconfigure their supply chains, Iranian barrels will continue to languish at sea.

The Indian Stance

India, another primary target for Iranian exports, has effectively shut the door for the time being. Indian refiners have secured Russian supplies through late summer, providing them with a stable, albeit politically complex, alternative. Furthermore, the persistent uncertainty surrounding US-dollar payment channels remains a deal-breaker. Indian refiners are unwilling to risk the financial and legal consequences of arranging financing and insurance for a cargo that may, within weeks, fall back under the purview of strict US sanctions.

Official Responses and Diplomatic Friction

While official statements from Tehran remain optimistic, highlighting the success of "breaking the blockade," the silence from potential buyers is deafening. There is a palpable lack of political appetite among major Asian importers to test the durability of Washington’s waivers.

The primary concern is the "reversibility" of US policy. No major energy firm wants to commit to a multi-million dollar transaction, secure the logistics, and then find the geopolitical window slammed shut before the oil is refined. This "policy risk" is the ultimate deterrent. The oil may be legal today, but in the volatile world of international sanctions, it may be deemed "illicit" in thirty days. This risk premium currently outweighs the benefit of discounted pricing.

Implications: A Market in Distress

The implications of this supply glut are profound, affecting both the oil market and Iran’s long-term economic strategy.

1. The Smell of Distress

In the commodity trading world, nothing discourages buyers like the scent of desperation. As tankers sit offshore for extended periods, the market recognizes that the seller is struggling to clear inventory. This inevitably leads to a "waiting game," where buyers hold off in anticipation of deeper price cuts. Once a seller is perceived as desperate, they lose the ability to set the market price; instead, the buyers dictate the terms.

2. The Price Must Do the Talking

If Iran is to move these barrels, it must fundamentally change its pricing strategy. Deep, aggressive discounts are the only mechanism by which Iranian crude can displace current suppliers. Asian refiners have the technical capacity to reshuffle their supply, resell competing grades, and free up tank space, but only if the financial incentive is high enough to justify the risk.

3. The "Fear Premium" Rebound

The initial reopening of the Strait of Hormuz was expected to lower the global "fear premium" on oil. While this has occurred, it has been replaced by a different kind of volatility: the uncertainty of a market flooded with unsold, distressed supply. The reopening of transit routes did not just allow for oil to move; it released a backlog of deferred supply into a market that was already at capacity.

4. The Strategic Clock

Ultimately, Iran’s current situation represents a failure to account for market saturation. By focusing exclusively on the "right to export," Tehran underestimated the difficulty of "market clearing." The country has successfully navigated the physical blockade of the Gulf only to sail into a much more unforgiving reality: a global market that is not waiting for their product.

As the mid-August deadline approaches, the pressure on the Iranian oil sector will only intensify. Unless Tehran can offer unprecedented incentives to overcome the risk-aversion of Asian refiners, the sight of tankers anchored off the coast of Singapore will remain a stark symbol of a strategy that has outpaced its demand. The "export machine" may be running, but the fuel is not clearing, and for a nation reliant on the rapid monetization of its resources, time is the one commodity it cannot afford to lose.