SINTRA, Portugal — In a move that marks a definitive paradigm shift for global financial markets, Federal Reserve Chair Kevin Warsh has officially declared the end of "forward guidance"—the highly telegraphed communication strategy that has anchored global monetary policy for the last quarter of a century.

Speaking at the European Central Bank’s (ECB) annual forum in Sintra, Portugal, Warsh used his first major public appearance as head of the U.S. central bank to dismantle the practice of signaling future interest rate paths. His message to investors, economists, and market participants was unequivocal: the era of the highly predictable, hand-held Federal Reserve is over.

Main Facts: Warsh Rejects the Policy of Pre-Commitment

The confrontation over the future of central bank communication came to a head during a panel discussion when the moderator repeatedly pressed Warsh for clues on the Fed’s next policy moves. Rather than offering the typical diplomatic, heavily parsed response, Warsh flatly refused to play along, delivering a sharp rebuke of the practice.

“You’re back to forward guidance. I’m going to disabuse you of trying to extract that. No forward guidance, no forward guidance.”

This direct rejection of the Fed’s most relied-upon policy tool of the modern era signals a profound shift in how the central bank intends to operate. Under his leadership, the Fed will no longer offer markets a roadmap for interest rates, opting instead for maximum flexibility and genuine data-dependence.

+-----------------------------------------------------------------+

| THE FED'S NEW MONETARY POLICY STANCE |

+---------------------------------+-------------------------------+

| OLD REGIME | NEW REGIME |

+---------------------------------+-------------------------------+

| • Heavy Forward Guidance | • No Forward Guidance |

| • Highly Telegraphed Hikes/Cuts | • Real-Time Data Dependence |

| • "Fed Put" Market Backstop | • Markets Lead the Fed |

| • Focus on Demand Management | • Focus on Supply/Productivity|

+---------------------------------+-------------------------------+

Warsh’s stance is backed by a deeply divided Federal Open Market Committee (FOMC). As revealed in recent policy discussions, Fed officials remain highly fractured over the trajectory of the federal funds rate:

A significant faction of the committee favors holding rates at current levels for an extended period.

A hawkish minority is leaning toward an additional rate hike to ensure inflation is fully extinguished.

A single, more dovish member would prefer an immediate rate cut to preempt economic cooling.

With no clear consensus on the committee and no personal inclination to ease policy prematurely, Warsh emphasized his primary mandate with stark simplicity:

“We’re going to deliver price stability in the US.”

The Productivity Wildcard: AI as an Economic Cushion

While Warsh struck a stern, hawkish tone regarding inflation and communication, he left the door open to potential rate cuts down the line, pointing to a surprising source of economic resilience: artificial intelligence.

Rather than relying on demand-side weakness to bring down inflation, Warsh expressed optimism that supply-side improvements—specifically AI-driven productivity gains—could do the heavy lifting. Over the past four quarters, productivity data has shown remarkable strength, giving the Fed chair reason for cautious optimism.

“But if the last four quarters are an indication… there’s reason to be optimistic now.”

If these productivity gains prove structural rather than cyclical, they could allow the U.S. economy to grow at a healthy clip without generating inflationary pressures, potentially paving the way for monetary easing later in the year. However, true to his new policy of non-commitment, Warsh stopped well short of making any promises.

Chronology: From the Birth of Transparency to the Sintra Burial

To understand the gravity of Warsh’s declaration, one must examine the 25-year history of how central banks communicated with the public.

CHRONOLOGY OF CENTRAL BANK COMMUNICATION

│

├── 1990s: "Purposeful Obfuscation" (The Greenspan Era)

│ └── Central banks operate in extreme secrecy; policy changes are unannounced.

│

├── Late 1990s - 2000s: The Birth of Transparency

│ └── The Fed begins issuing post-meeting statements to reduce market volatility.

│

├── 2008 - 2020: The Golden Age of Forward Guidance

│ └── Bernanke and Yellen introduce explicit "forward guidance" and "dot plots"

│ to keep long-term yields low during the post-GFC recovery.

│

├── 2021 - 2023: The Inflation Trap

│ └── Forward guidance backfires. Central banks find themselves locked into

│ accommodative policies as inflation surges to multi-decade highs.

│

└── Present: The Sintra Consensus

└── Warsh, Lagarde, Bailey, and Macklem formally retire forward guidance.

1. The Era of "Purposeful Obfuscation" (Pre-1990s)

For decades, central banks operated under a veil of extreme secrecy. Under Fed Chair Alan Greenspan, the prevailing philosophy was one of "purposeful obfuscation." Markets had to guess whether the Fed had changed interest rates by observing open-market operations the following morning.

2. The Great Financial Crisis and the Birth of "Forward Guidance" (2008)

Following the 2008 financial crisis, when short-term interest rates hit the zero lower bound, central banks needed a new tool to stimulate the economy. Under Ben Bernanke, the Fed introduced "forward guidance"—explicit promises to keep interest rates low for an extended period or until specific economic thresholds (such as a 6.5% unemployment rate) were met. This successfully anchored long-term bond yields and gave businesses the confidence to borrow and invest.

3. The Pandemic Shock and the Inflation Trap (2021–2023)

The flaws of forward guidance became painfully apparent during the post-pandemic recovery. Locked into commitments to keep rates low, central banks were slow to react when inflation began its historic surge in 2021. Bound by their own previous communication, they feared that a sudden policy reversal would trigger a market panic. Consequently, they fell dangerously behind the inflation curve.

4. The Sintra Consensus (Present)

The panel in Sintra, Portugal, represents the final nail in the coffin for this policy. Central bankers have collectively realized that in a highly volatile, supply-shock-prone global economy, promising future policy paths is a dangerous liability.

Supporting Data: Productivity Gains, Speech Volatility, and the Week Ahead

The shift away from forward guidance is happening against a backdrop of complex economic data, an impending corporate earnings season, and an absolute explosion in central bank public communications.

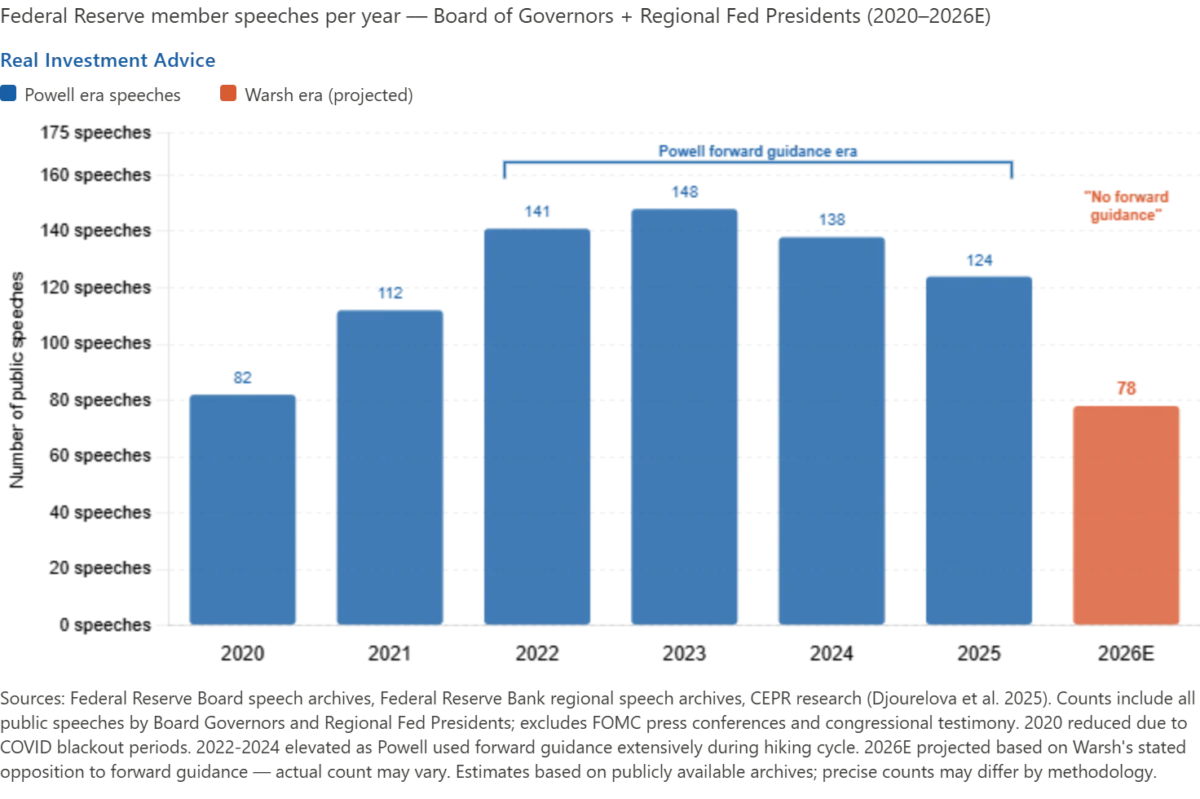

The Speech Bubble

The retirement of forward guidance comes at a time when the sheer volume of central bank communication has reached an all-time high. Over the last decade, the number of speeches delivered by Federal Reserve officials annually has skyrocketed, creating a confusing wall of noise for market participants.

Instead of clarifying policy, the deluge of conflicting speeches and the quarterly release of the "dot plots" (the FOMC’s interest rate projections) have heightened market volatility. Warsh’s new regime aims to cut through this noise by rendering individual policy predictions obsolete.

The Wednesday FOMC Minutes: Assessing the June Divide

Investors will get their first look at the depth of the Fed’s internal divisions on Wednesday, with the release of the minutes from the FOMC’s June 17 meeting.

FOMC JUNE 17 MEETING: THE THREE-WAY SPLIT

┌─────────────────────────────┼─────────────────────────────┐

│ │ │

▼ ▼ ▼ ▼

[ THE HAWKS ] [ THE NEUTRALS ] [ THE DOVES ]

Lean toward a rate hike Prefer to hold rates Prefer to cut rates

to squash inflation. steady and observe data. immediately to protect growth.

The minutes will reveal whether the hawkish tone perceived by the media was a unanimous consensus or if the committee is deeply fractured. Market participants will scrutinize the text to see how many members align with Warsh’s strict anti-guidance stance.

Q2 Earnings: A Litmus Test for the "Higher-for-Longer" Economy

As the Fed steps back from guiding the markets, corporate fundamentals will take center stage. The Q2 earnings season kicks off this week with major financial institutions, including JPMorgan Chase (NYSE: JPM), Wells Fargo (NYSE: WFC), and Citigroup (NYSE: C).

These reports will provide critical data on how the Fed’s "higher-for-longer" interest rate environment is impacting the real economy:

Net Interest Margins (NIM): Analysts will watch bank NIMs closely. While higher rates initially boost lending profitability, prolonged high rates force banks to pay more for deposits, squeezing their margins and restricting credit availability.

Credit Loss Provisions: An increase in provisions for bad loans will signal whether consumer stress—already visible in rising credit card and auto loan delinquency rates—is accelerating.

Official Responses: Global Central Bankers Align

Significantly, Kevin Warsh was not a lonely voice in Sintra. His determination to bury forward guidance was echoed by the leaders of the world’s most powerful central banks, who expressed mutual exhaustion with the communication strategy.

Christine Lagarde (President, European Central Bank)

ECB President Christine Lagarde was remarkably candid about the limitations that forward guidance had imposed on the eurozone’s monetary policy during the inflation crisis. She admitted that the policy had severely compromised the ECB’s agility.

“My one regret is feeling bound and compelled by forward guidance in the past.”

Andrew Bailey (Governor, Bank of England) & Tiff Macklem (Governor, Bank of Canada)

Both Bailey and Macklem expressed similar reservations, noting that in an environment characterized by geopolitical tensions, energy shocks, and supply chain reconfigurations, pre-committing to interest rate paths is counterproductive. The consensus among the leaders was clear: central banks must reclaim their freedom of maneuver.

Implications: A New Regime for Wall Street and Investors

The formal retirement of forward guidance has profound implications for global financial markets, rewriting the rules of engagement that have governed investing for a generation.

+-----------------------------------------------------------------------+

| IMPLICATIONS OF THE NEW MONETARY REGIME |

+-----------------------------------------------------------------------+

| 1. High Market Volatility |

| Without Fed hand-holding, asset prices will fluctuate sharply in |

| response to raw economic data releases. |

| |

| 2. Reversal of the Fed-Market Relationship |

| The Fed will no longer lead the markets; instead, market pricing |

| and financial conditions will dictate the Fed's path. |

| |

| 3. Devaluation of the "Dot Plot" |

| Quarterly interest rate projections and member speeches will carry |

| significantly less weight in investment models. |

| |

| 4. Increased Focus on Hard Macro Data |

| Investors must shift their focus from deciphering Fed speak to |

| analyzing CPI, labor market, and productivity data in real-time. |

+-----------------------------------------------------------------------+

1. The Death of the "Fed Put" and the Return of Volatility

For years, investors operated under the assumption of the "Fed Put"—the belief that the central bank would telegraph its moves well in advance to prevent market downturns. With forward guidance gone, asset prices will likely experience significantly higher volatility. Without a central bank holding their hand, investors will have to price in genuine, unmitigated macro risks.

2. Markets Will Lead the Fed

In the previous regime, the Fed dictated terms to the market, which then adjusted asset prices accordingly. In the new regime, the dynamic is reversed. The markets will price in economic realities in real-time, and the Fed will react to those market-driven financial conditions. Investors who continue to rely on Fed speeches and dot plots for positioning are operating under an obsolete playbook.

3. A Return to Fundamental Investing

With central bank policy becoming less predictable, the correlation between different asset classes is likely to decouple. Macroeconomic data releases—such as Consumer Price Index (CPI) reports, non-farm payrolls, and productivity metrics—will trigger sharper, more immediate market reactions, as the Fed will no longer cushion these data points with pre-emptive speeches.

Ultimately, Kevin Warsh’s debut on the international stage has established a new normal. By stripping away the safety blanket of forward guidance, the Federal Reserve has challenged Wall Street to stand on its own feet. In this new era, the markets will no longer be guided; they will have to explore the path alone.