Main Facts: The Intersection of Macro Policy and Geopolitical Tension

Crude oil markets have entered a high-stakes, policy-driven phase, balancing a nascent price recovery against a backdrop of renewed shipping disruptions and shifting monetary expectations. As investors prepare for the release of the Federal Open Market Committee (FOMC) Minutes, the broader energy complex is grappling with the duality of restrictive financial conditions and persistent, supply-side geopolitical premiums.

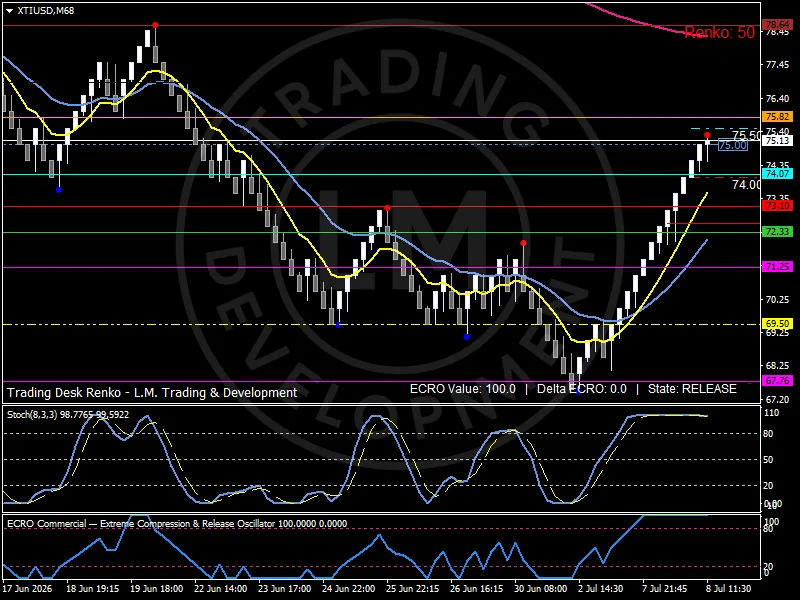

West Texas Intermediate (WTI) has successfully transitioned from a period of prolonged price compression into a distinct "release regime," characterized by increased participation and a sequence of higher highs and higher lows. This technical shift is occurring alongside heightened volatility in Treasury yields and a fluctuating U.S. dollar, both of which remain the primary macro variables dictating commodity sentiment. Simultaneously, the energy market is contending with maritime security concerns, particularly in the Strait of Hormuz, which have introduced a "High Stress" environment for global tanker logistics.

This confluence of factors—central bank signaling, inventory dynamics, and maritime threats—creates a volatile landscape where the next directional move for crude oil hinges on whether the current recovery can sustain its momentum against the headwinds of broader economic uncertainty.

Chronology: From Compression to Active Expansion

The current market environment is the culmination of several weeks of evolving data and geopolitical developments.

The Macro Context (Last Week)

The groundwork for the current week’s volatility was laid last week when updated manufacturing data provided a mixed signal to the markets. While activity moderated, it remained firmly in expansion territory, providing a stabilizing floor for energy demand expectations. However, this moderation triggered a pivot in investor focus, shifting from recessionary fears toward the upcoming FOMC Minutes. The market is seeking explicit clarity on the Federal Reserve’s "higher-for-longer" stance and how policymakers intend to balance the dual mandates of suppressing inflation while maintaining restrictive financial conditions that do not inadvertently stifle growth.

The Shift to Geopolitical Risk (Mid-Week)

As the week progressed, the narrative shifted from purely macroeconomic to heavily geopolitical. Fresh security incidents in the Strait of Hormuz—a vital chokepoint for global oil transit—suddenly regained prominence. Intelligence reports classified the maritime environment as "High Stress," with elevated alerts regarding tanker safety. This immediately injected a risk premium into crude prices, overriding concerns about potential demand cooling.

The Technical Pivot (Recent Sessions)

Technically, the market moved from a compression phase—where price action was tightly range-bound—to a release regime. Following a successful defense of the $67.75 support level, buyers re-entered the market with conviction. The reclaiming of key participation areas at $72.33 and $74.07 signaled a shift in market psychology, moving the WTI structure into a bullish configuration that is currently testing the $75.50 resistance zone.

Supporting Data: Inventory, Technicals, and Market Structure

Inventory and Refinery Dynamics

Market participants are currently laser-focused on the latest U.S. inventory data. Preliminary indications suggest that refinery utilization remains at seasonally elevated levels. This high rate of activity, combined with relatively tight inventories, creates a supply-side cushion that supports prices. When inventory data is released alongside central bank communications, the resulting volatility often accelerates price discovery, making today’s FOMC release a critical juncture for the energy sector.

Technical Indicators

The technical health of the WTI market is currently defined by the following metrics:

- Moving Averages: Price is currently trading above the rising 9-day and 21-day Exponential Moving Averages (EMA), confirming a short-term bullish trend. However, the 200-day EMA remains significantly above current price action, reminding traders that the long-term structural trend has not yet fully reversed to the upside.

- Momentum: The Stochastic oscillator remains firmly in "overbought" territory, a condition that, in a strong directional market, confirms persistent buying pressure rather than immediate exhaustion.

- ECRO Analysis: The Energy Commodity Release Oscillator (ECRO) has reached a full "Release" reading. This confirms that the market has exited its period of consolidation and has entered an expansion phase, where price moves are likely to be more rapid and decisive.

Official Responses and Monetary Implications

The financial world awaits the FOMC Minutes as the primary catalyst for the next phase of market directionality. Reuters and other major news outlets have highlighted that the market is searching for "greater clarity" regarding the Fed’s assessment of inflation.

If the Minutes reveal that policymakers are becoming more concerned about the risks of a restrictive policy environment, we could see a retreat in Treasury yields and a softening of the U.S. dollar, which would provide a natural tailwind for dollar-denominated commodities like crude oil. Conversely, if the communication reinforces a commitment to maintaining current high interest rates for an extended period, the resulting strength in the dollar could act as a drag on crude, potentially stalling the current recovery.

Furthermore, the "High Stress" environment in global shipping routes has elicited a tacit, albeit cautious, acknowledgment from global trade monitors. While governments have not yet issued direct intervention mandates, the increased cost of maritime insurance and the potential for shipping delays have effectively created a supply-side constraint that mirrors the impact of a production cut.

Implications: What Lies Ahead

The current market configuration presents a series of clear technical hurdles and opportunities for traders:

The Path of Resistance

The region between $74.00 and $74.10 has emerged as the principal short-term participation area. To maintain the constructive, bullish structure, the market must hold above this zone. Failure to do so would suggest that the recovery lacks deep-seated institutional support. Conversely, a successful consolidation above this level sets the stage for a test of the $75.50–$75.80 resistance corridor. A decisive breakout above $75.80 would clear the path for a move toward the $78.60 level, a significant area of historical participation.

Downside Risks

On the downside, the $72.33 level represents the first meaningful support. If volatility spikes following the FOMC release, this is the area where buyers will likely attempt to reorganize. A failure to hold $72.33 could lead to a re-test of the lower support levels and a potential return to the compression phase that dominated earlier in the month.

Strategic Outlook

Traders should be aware that when inventory data and central bank communications coincide, liquidity often thins before widening dramatically upon the news release. Today’s FOMC Minutes represent the most significant macro catalyst capable of reshaping the current trajectory of yields, the dollar, and broader commodity participation.

Ultimately, the market is currently caught between two competing forces: the fundamental reality of a potential economic slowdown (monetary policy) and the immediate, supply-side anxiety generated by geopolitical instability (maritime shipping). The ability of WTI to sustain its recent recovery will depend on whether the macroeconomic "release" provided by the FOMC Minutes can align with the bullish technical momentum already present in the charts.

What Traders Should Watch

- FOMC Minutes Release: The primary driver for the U.S. Dollar Index (DXY) and 10-year Treasury yields.

- Shipping Security Alerts: Continued monitoring of the Strait of Hormuz for any escalation in "High Stress" classification.

- Refinery Throughput: Updates on U.S. inventory levels to confirm if current refinery utilization can offset potential demand-side concerns.

- The $74.00 Pivot: Watch for price stability at this level as a primary indicator of continued institutional participation.

- ECRO/Stochastic Divergence: If momentum indicators begin to show signs of exhaustion while the price remains near resistance, it may signal an imminent consolidation phase.