Financial stability is rarely derailed by the predictable. Most households can effectively manage monthly recurring costs like rent, utilities, and grocery bills. Instead, the true culprits behind personal debt—and the primary reason many families find themselves reaching for credit cards in a panic—are the "lumpy" expenses: those infrequent, large-scale financial obligations that strike with the force of a surprise, despite being entirely inevitable.

The solution to this fiscal volatility is a time-tested strategy known as the "sinking fund." By transforming irregular annual or semi-annual costs into manageable monthly installments, you can flatten the peaks and valleys of your financial life, ensuring that your budget remains a tool for stability rather than a source of recurring anxiety.

The Anatomy of a Sinking Fund: Main Facts

A sinking fund is, in its simplest form, a designated savings vehicle used to set aside money for a specific future expense. Unlike a traditional emergency fund, which is meant for the "unknown unknowns"—such as a sudden medical crisis, a vehicle breakdown, or unexpected unemployment—a sinking fund is for the "known unknowns."

These are the expenses you know are coming, but which occur at irregular intervals. Examples include annual property taxes, vehicle registration fees, bi-annual insurance premiums, holiday gift-giving budgets, back-to-school shopping, and routine home maintenance like gutter cleaning or HVAC servicing.

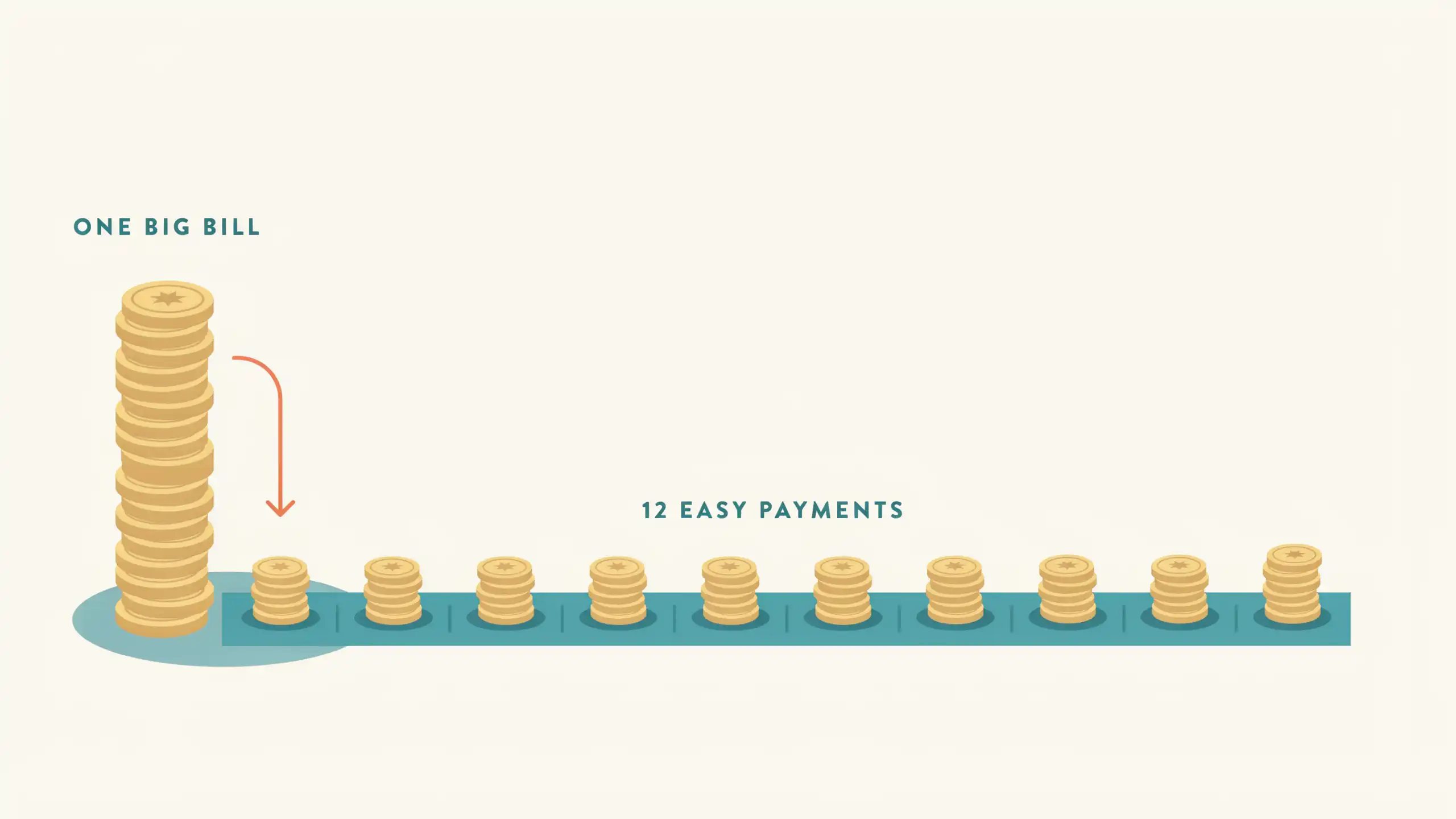

The mathematical premise is elegant in its simplicity:

- Identify the cost: Determine the total annual amount for a specific non-monthly expense.

- Calculate the installment: Divide that total by 12.

- Automate the contribution: Treat that installment as a non-negotiable monthly "bill" that you pay to your future self.

By moving these funds into a separate account immediately following each payday, you effectively "pre-pay" your annual bills. When the expense finally arrives, the capital is already waiting, allowing you to pay in full without disrupting your monthly cash flow or resorting to high-interest debt.

Chronology of Financial Volatility

To understand why sinking funds are essential, one must look at the timeline of the typical household budget. Most income is structured in a linear fashion: you receive a paycheck every two weeks or once a month. Your expenses, however, are rarely linear.

The "Spike" Effect

In January, you might have light utility bills and no major obligations. By November and December, however, the "spike" hits: holiday spending, winter heating bills, and year-end property tax installments. If your budget is calibrated to your average monthly income, the massive outflow required in December creates a deficit.

Without a sinking fund, the chronology of the year looks like a series of financial crises followed by periods of recovery. You spend the spring and summer "paying off" the debt incurred during the winter holidays. This cycle of debt-recovery-debt is precisely what traps many households in a permanent state of financial fragility.

The Shift to Proactive Management

When you implement a sinking fund system, the timeline changes. You are no longer living in reaction to your calendar. Instead, you are building a reservoir of capital that builds slowly over the months. By the time the "lumpy" month arrives, your financial position is neutral. You aren’t "spending" money in December; you are simply transferring funds that were allocated months prior.

Supporting Data: Why "Lumpiness" Wrecks Budgets

Data from consumer advocacy groups consistently indicates that credit card debt often spikes in the first quarter of the year, directly correlating with holiday spending and year-end financial obligations.

Consider the average American family’s annual obligations:

- Auto Insurance: Often billed in six-month blocks ($800–$1,200).

- Holiday Spending: The average consumer spends roughly $800–$1,000 annually on gifts and decorations.

- Home Maintenance: Standard rule of thumb suggests budgeting 1% of home value annually. For a $300,000 home, that is $3,000 a year.

If these expenses are not accounted for, they represent a "surprise" hit to the budget of nearly $5,000 a year. When these costs are distributed across 12 months, the burden is approximately $416 per month. Most households can absorb $416 a month if it is planned; very few households can absorb a $5,000 hit in a single month without incurring high-interest credit card debt.

Perspectives on Financial Discipline: Expert Responses

Financial planners and behavioral economists largely agree that the psychological benefit of sinking funds is as significant as the mathematical benefit.

"The primary barrier to wealth building is not lack of income, but the lack of planning for predictable events," notes a leading personal finance consultant. "When you use a sinking fund, you change your relationship with your money. You stop viewing a $1,200 insurance bill as a ‘disaster’ and start viewing it as a bill you’ve already paid."

Critics of the sinking fund method sometimes argue that the money could be better utilized in investment accounts (like the stock market). However, proponents argue that for short-term liquidity needs (expenses occurring within 12 months), the risk of market volatility outweighs the potential interest gains. The goal of a sinking fund is not capital appreciation—it is capital preservation and liquidity.

However, modern banking tools have mitigated the "interest loss" argument. Many high-yield savings accounts (HYSAs) now offer competitive interest rates, meaning your sinking fund is working for you even while it sits in wait.

Implications: Building Your System

If you are ready to stabilize your finances, the implementation process should be methodical.

1. The Audit

Review your bank and credit card statements for the past 12 months. Flag every expense that occurred only once or twice. Create a master list and calculate the annual total for each.

2. The Infrastructure

Utilize a high-yield savings account that allows for "buckets" or "sub-accounts." This is vital for the psychological benefit of seeing exactly how much you have saved for specific goals. When you see a "Car Repair" bucket with $1,200 in it, you are less likely to raid that money for discretionary spending.

3. The Automation

Human willpower is a finite resource. Do not rely on your ability to "remember" to move money. Set up automatic transfers that trigger the day after your paycheck hits your primary checking account. If you see the money in your checking account, you are statistically more likely to spend it. By automating the transfer, the money becomes "invisible," effectively reducing your available cash for discretionary spending.

4. The Iterative Process

Don’t try to fund everything at once. Start with the expense that caused you the most stress last year. If an unexpected $500 car registration fee nearly caused a missed rent payment, make that your first sinking fund priority. Once that is automated, move to the next item on your list.

Conclusion: The Peace of Mind Dividend

The ultimate goal of personal finance is not just to accrue numbers on a spreadsheet, but to create a life free from the panic of unexpected bills. A sinking fund is one of the most effective tools for achieving this. By acknowledging that your expenses will always be "lumpy," you can proactively smooth them out, transforming your financial landscape from one of erratic spikes into a steady, manageable plateau.

As you begin to see your "buckets" fill up, you will notice a change in your behavior. You will stop dreading the arrival of the holiday season, and you will stop worrying about the next annual check-up for your vehicle. You will be operating from a position of strength, knowing that your past self has already taken care of your future obligations.

In the world of personal finance, nothing is truly a surprise if you have the foresight to plan for it. Start your sinking fund today, and reclaim your budget from the tyranny of the "lump."