The global silver market is currently defined by a striking paradox: while headlines from Western commodity exchanges suggest a cooling market with refilling stockpiles, the reality on the ground—particularly in Asia—tells a story of persistent, acute physical scarcity. As silver prices fluctuate, hovering near $61.50 per ounce, investors are finding themselves caught between the "paper" price dictated by the COMEX and the "physical" price commanded in Shanghai. Understanding this divergence is no longer optional for market participants; it is the key to decoding the current structural deficit in the precious metals sector.

The State of Play: A Market in Search of a Narrative

After a volatile start to 2026, the silver market has spent the last fortnight appearing as though it has lost its primary narrative. Following a historic peak of $121.62 on January 29, the metal has corrected significantly, shedding roughly 49% of its value. While silver remains up by approximately 66% compared to its position one year ago, the recent 13% decline from its 2025 year-end close of $71 has left many traders disillusioned.

With gold trading near $4,150 and the gold-silver ratio hovering around 67, the "soft tape" observed in Western trading venues has prompted a wave of bearish sentiment. The primary driver of this pessimism is the recent uptick in silver stocks held in New York’s futures warehouses. For many, a rising stockpile is the quintessential indicator of a well-supplied, loosening market. However, a deeper analysis of warehouse dynamics suggests that these figures may be a optical illusion, masking a fundamental tightening in global physical supply chains.

Chronology of a Divergence: From New York to Shanghai

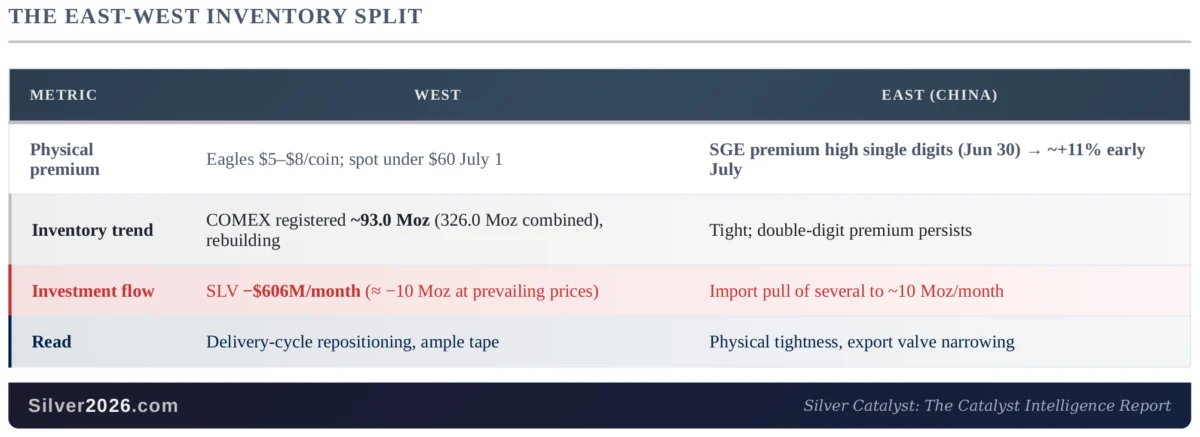

The narrative of "loosening" silver supply finds its roots in the July 6 report from COMEX warehouses. According to the data, "registered" silver—metal explicitly pledged to settle futures contracts—climbed to approximately 93.0 million ounces. When combined with "eligible" metal (stored but not currently offered for delivery), the total stock sits at roughly 326.0 million ounces.

To the casual observer, the growth of the registered pool from 82 million ounces in mid-June to 93 million ounces in just three weeks is a bearish signal. However, this is not a result of a surge in new mine production or a sudden glut of metal hitting the market. Instead, it represents a sophisticated repositioning of existing assets. Market participants have been reclassifying "eligible" metal into "registered" status to meet the liquidity requirements of the active July delivery month.

While the West focuses on these paper-based inventory shifts, the East has been contending with an entirely different reality. On the Shanghai Gold Exchange (SGE), the dynamic is one of aggressive accumulation. As of the June 30 benchmark fixes, silver was trading at a high single-digit premium over international prices. By early July, that gap had expanded to 11%.

This is not merely a regional anomaly; it is a profound signal of physical market tension. When buyers are willing to pay an 11% premium—even after accounting for currency fluctuations, local taxes, and import costs—it confirms that the marginal buyer is no longer sitting in London or New York, but in Shanghai.

Supporting Data: Dissecting the Supply-Demand Split

The current state of the silver market can best be described as a "two-speed" economy. The data supporting this bifurcation is multifaceted, spanning ETF flows, retail premiums, and regulatory shifts in China.

1. Western Outflows and Retail Sentiment

The perception of a "loose" market in the West is supported by concrete data. The largest silver exchange-traded fund (ETF) has experienced significant headwinds, recording net outflows of approximately $606 million over the past month. This represents roughly 10 million ounces of metal being liquidated by investment funds at current price levels. Concurrently, US retail demand has cooled, with premiums on 2026 American Silver Eagles declining from their earlier peaks to a range of $5 to $8 per coin. This reduction in retail appetite confirms that Western investors are currently in a "risk-off" mode, contributing to the perceived softness of the market.

2. The China Factor and Export Controls

The situation in the East is exacerbated by geopolitical and regulatory developments. On July 1, Beijing implemented stricter enforcement of strategic-mineral export controls. Silver is reportedly among the minerals now subject to rigorous licensing requirements. This move effectively creates a "sink" for physical silver; metal that enters China is increasingly difficult to move back into the global supply chain. By restricting the outflow of strategic minerals, China is effectively ring-fencing its physical supply, forcing domestic buyers to pay higher premiums to secure available stock.

3. Warehouse Stocks vs. Physical Scarcity

The CME warehouse stocks, while useful for tracking exchange-level liquidity, are increasingly detached from the global physical balance. The "registered" category is highly sensitive to the immediate needs of futures contract holders, but it does not account for the massive industrial demand that characterizes the global silver market. When one compares the 11-million-ounce increase in registered stocks against the backdrop of a six-year structural deficit, it becomes clear that the warehouse build is a symptom of technical repositioning rather than a reflection of an oversupplied market.

Official Responses and Strategic Implications

Market analysts and industry bodies have been quick to point out that a structural deficit—the core of the long-term silver thesis—does not imply that every vault must empty simultaneously. A deficit means that annual global demand consistently outstrips annual mine and secondary supply. In the interim, metal "sloshes" between regions.

The primary implication for investors is that the COMEX warehouse reports should not be read as a barometer for global physical supply. The headline price of silver is set in the Western "paper" market, where institutional funds and high-frequency traders can exert downward pressure through derivative selling. Conversely, the "physical" market, represented by the Shanghai premium, is where the supply-demand imbalance manifests most clearly.

For those tracking the long-term potential of silver, the current volatility is a test of conviction. If the Western paper market continues to diverge from the Eastern physical reality, one of two things must happen: either the West will be forced to raise prices to attract metal back into global circulation, or the Eastern premium will eventually compress as the lack of available metal forces a slowdown in industrial consumption. Given that the structural deficit has persisted for six years, the former remains the more likely long-term outcome.

Conclusion: The Throughline of the 2026 Market

The divergence between the New York warehouse build and the Shanghai premium is the defining narrative of the 2026 silver market. It is a tale of two distinct mentalities: the West, which views silver primarily through the lens of investment vehicles and paper liquidity, and the East, which views silver as a strategic industrial necessity.

Investors should remain wary of placing too much weight on short-term vault data. The structural case for silver has never been predicated on the weekly reporting of COMEX stock levels. Instead, it relies on the undeniable fact that the world is consuming more silver than it can extract or recycle.

As long as the marginal buyer continues to pay a double-digit premium in Shanghai while the West treats the metal as a redundant asset, the volatility will persist. However, the "throughline" remains clear: we are witnessing the migration of physical silver toward the markets that value it most. The rebuilding of Western vaults is not a refutation of the silver deficit; it is merely a temporary regional offset to a global reality that remains as tight as ever. For the patient investor, the current disconnect between paper and physical is not a reason for despair, but a clear indicator of where the market’s underlying strength truly resides.