The global energy landscape is currently navigating a period of profound uncertainty, characterized by a fragile equilibrium between recovering Persian Gulf supply chains and a conspicuous absence of robust demand from the world’s largest importer, China. While the mid-June Memorandum of Understanding (MoU) between the United States and Iran provided a temporary sense of relief, recent geopolitical flare-ups have cast a long shadow over the stability of global oil and gas markets.

The Main Facts: A Fragile Recovery

The oil market underwent a significant correction following the 17 June agreement, which aimed to de-escalate tensions and restore oil flows from the Persian Gulf. This development initially triggered a sell-off in crude futures, as the market anticipated a swifter-than-expected normalization of supply. However, the optimism was short-lived.

The reality on the ground remains far from the pre-war status quo. While oil flows have recovered from the nadir of the conflict, they remain at approximately 14 million barrels per day (b/d), significantly below the 20 million b/d levels recorded before the hostilities commenced. The bottleneck persists primarily due to the ongoing volatility surrounding the Strait of Hormuz, a critical chokepoint for global energy transit.

Simultaneously, the European natural gas market is contending with its own set of structural vulnerabilities. Unlike the oil market, which has seen some supply elasticity, European LNG imports remain constrained by intense competition from Asian markets and logistical delays in Qatari export infrastructure.

Chronology of the Crisis and Response

To understand the current market sentiment, one must look at the timeline of events that have shaped the 2026 energy landscape:

- Early 2026: Intensification of US-Iran tensions leads to severe disruptions in the Strait of Hormuz, causing oil supply to plummet and prices to spike toward the $100/bbl threshold.

- 17 June 2026: The signing of the Memorandum of Understanding (MoU) between the US and Iran signals a potential path toward de-escalation and the resumption of normal trade flows.

- Late June 2026: Market analysts observe an initial surge in tanker activity, though vessel transits remain well below pre-conflict averages.

- July 2026: A re-escalation of military tensions in the region creates a "dual-reality" for traders: the supply chain is officially "opening," yet the physical risk of maritime transit remains elevated.

- Ongoing: European gas storage levels struggle to hit target thresholds amidst sustained heatwaves and a lack of LNG inflows.

Supporting Data: The Quantitative Landscape

The fundamental outlook for oil is dictated by a shifting balance sheet. Analysts have revised their ICE Brent forecasts downward, anticipating an average of $80/bbl in 3Q26 and $74/bbl in 4Q26, reflecting the influx of supply. However, these figures are predicated on the assumption that no further meaningful disruptions occur in the Persian Gulf.

Crude Oil Flow Dynamics

The discrepancy between potential and actual output is stark. While the normalization of flows was originally projected to take the entirety of the third quarter, the current pace suggests a potential completion by the end of July. Yet, this remains highly fluid. If the geopolitical environment worsens, the market could shift from its current baseline to an "aggressive" scenario, where Brent crude potentially tests the $100/bbl resistance level once more.

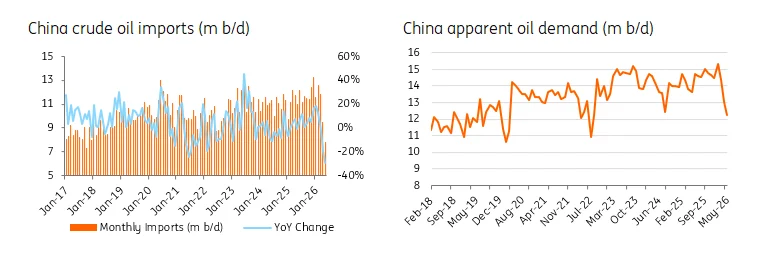

China: The Missing Engine

Perhaps the most significant variable in the global energy equation is China. During the height of the Persian Gulf disruptions, China acted as a buffer by significantly curbing its imports. In May, crude oil imports were down 30% year-on-year, with June data suggesting further contraction.

For the market to achieve sustainable stability, a recovery in Chinese domestic demand is essential. Estimates indicate that domestic consumption fell by 1.4 million b/d in 2Q26. While the Chinese government has recently relaxed export restrictions on refined products to incentivize refiners, this measure alone is insufficient. Without a broad-based recovery in the manufacturing and consumer sectors, the lack of Chinese buying will continue to exert downward pressure on prices, offsetting the bullish signals from geopolitical risk.

The European Gas Dilemma

European energy security is currently in a state of high alert. The region’s transition away from traditional supply sources has left it heavily reliant on the global LNG spot market.

Storage and Weather Factors

As of the latest reporting, EU gas storage levels have only recently eclipsed the 50% mark—a figure that pales in comparison to the five-year average of 66% for this time of year. Under current EU regulations, member states are mandated to reach specific storage targets, and current trends suggest that even the lowest threshold of 75% will be a challenge to achieve.

Compounding this is the meteorological factor. Persistent heatwaves across the continent have spiked demand for electricity for cooling purposes, drawing down gas reserves during a period typically reserved for replenishment. While some forecasts suggest that El Niño conditions might result in a milder 2026/27 heating season, providing a much-needed reprieve, such climate-dependent scenarios offer no guarantee of security. Consequently, European gas prices are expected to remain elevated and volatile until the end of the winter season.

Implications for Investors and Policy Makers

The current environment presents a complex challenge for market participants. The "wait-and-see" approach adopted by many institutional investors reflects the high level of uncertainty surrounding both geopolitical outcomes and macroeconomic indicators.

Geopolitical Risk vs. Fundamental Supply

The market is currently caught in a tug-of-war between the physical recovery of supply and the persistent "fear premium" associated with the Strait of Hormuz. Investors should be aware that while the market may experience periods of surplus in late 2026 and 2027, the near-term outlook is dominated by the risk of sudden, sharp price spikes should military tensions escalate again.

Strategic Recommendations

- Monitor Vessel Traffic: The most accurate real-time indicator of supply stability remains the volume of crude transiting the Strait of Hormuz. A return to the 20m b/d level is the primary signal for a cooling of the fear premium.

- Watch Chinese Run Rates: Investors should track the refinery run rates in China. If the easing of export restrictions leads to a sustained increase in crude intake, it will be a positive indicator for global oil demand.

- European Energy Policy: Policy makers in the EU will likely face increased pressure to expedite the diversification of energy imports. Failure to hit storage targets will likely result in increased regulatory intervention and potential price capping measures, which carry their own market risks.

Conclusion: A Precarious Future

The global energy market is currently undergoing a painful rebalancing act. The normalization of Persian Gulf flows is a necessary step toward price stabilization, but it is not a panacea. The combination of a fragile geopolitical ceasefire, the uncertain timing of a Chinese demand recovery, and Europe’s precarious gas storage situation suggests that volatility will remain the defining characteristic of the energy sector for the foreseeable future.

As we move into the latter half of 2026, market participants must remain agile. The transition from a supply-constrained environment to one of potential surplus in 2027 is the base-case scenario, but it is a path littered with risks that could easily derail current forecasts. For now, the world waits to see whether the diplomatic efforts of the summer can hold against the tide of regional instability and the shifting tides of global economic demand.

Disclaimer: This analysis is for informational purposes only and does not constitute financial, legal, or investment advice. Market conditions are subject to rapid change; readers are encouraged to perform their own due diligence before making investment decisions.