Executive Summary

A fragile geopolitical truce in the Middle East has fractured, threatening to disrupt the global economic outlook and upend central bank projections. Just three weeks after the United States and Iran signed a highly anticipated ceasefire, a sudden resumption of military strikes in the Persian Gulf has reignited volatility in energy and debt markets. This unexpected escalation has shattered the prevailing market narrative that geopolitical risk was steadily receding, forcing investors and policymakers to confront the reality of a protracted, volatile "gray zone" between war and peace.

The renewed hostilities come at a critical juncture for global monetary policy. While forward-looking economic indicators had previously suggested that inflationary pressures in the United States were poised to ease throughout the summer, the threat of prolonged disruption to Middle East energy corridors has injected deep uncertainty into these forecasts. With the Federal Reserve already deeply divided over its next steps, the return of geopolitical instability complicates the path forward, raising the stakes for upcoming policy decisions and challenging the market’s assumptions regarding interest rate cuts.

Main Facts: The Resumption of Hostilities and the Market’s Response

The primary catalyst for the renewed market anxiety is the sudden breakdown of the three-week-old ceasefire agreement between Washington and Tehran. Signed in late spring, the accord was widely viewed by international observers as a vital stabilization mechanism for the global economy. It promised to ease the geopolitical risk premium that has kept energy prices elevated and supply chains under duress.

However, military strikes launched by both sides in the Gulf region this week have effectively nullified the immediate benefits of that diplomatic breakthrough. The key developments surrounding this escalation include:

- Renewed Military Strikes: Direct military engagements in the crucial maritime corridors of the Gulf have resumed, highlighting the fragility of the diplomatic framework and demonstrating that neither side is prepared to fully retreat from defensive or offensive postures.

- Initial Market Shock: Upon news of the resumed hostilities, global crude oil benchmarks spiked, reflecting fears of supply disruptions in the Strait of Hormuz. Concurrently, U.S. Treasury yields climbed higher as investors priced in the potential for energy-driven supply shocks to keep inflation stickier for longer.

- Temporary Mid-Week Stabilization: By Thursday, markets experienced a tentative calm. Both oil prices and Treasury yields pulled back from their weekly highs, suggesting that while market participants are highly sensitive to headlines, they are also hesitant to price in a worst-case escalation scenario without further structural damage to energy infrastructure.

- Disrupted Inflation Trajectory: The renewed conflict has cast doubt on the timing and speed of inflation normalization. Economic models that had predicted a smooth decline in consumer prices starting in June must now account for a renewed risk of energy price shocks and supply chain friction.

Chronology: From Diplomatic Breakthrough to Renewed Conflict

To understand the current market volatility, it is necessary to trace the rapid succession of diplomatic and military events over the past month, which have repeatedly shifted investor sentiment from optimism to defensive caution.

+------------------------------------+

| Three Weeks Ago |

| US and Iran sign ceasefire accord. |

| Markets price in lower risk. |

+------------------+-----------------+

|

v

+------------------------------------+

| May |

| Proprietary models show transition |

| to high-inflation/high-growth. |

+------------------+-----------------+

|

v

+------------------------------------+

| June 16-17 |

| FOMC meets; minutes reveal a split |

| on persistence of inflation. |

+------------------+-----------------+

|

v

+------------------------------------+

| Early This Week |

| Ceasefire breaks; military strikes |

| resume. Oil and yields spike. |

+------------------+-----------------+

|

v

+------------------------------------+

| Thursday |

| Markets experience temporary calm; |

| Fed's Williams addresses outlook. |

+------------------+-----------------+The Diplomatic Window (Three Weeks Ago)

The United States and Iran signed a formal ceasefire agreement designed to halt active hostilities in the Gulf and pave the way for a normalization of regional trade and shipping. Following the announcement, international oil benchmarks fell, and sovereign bond yields moderated as investors anticipated a sustained period of geopolitical de-escalation.

The Warning Signals (May – Mid-June)

Even as diplomacy took center stage, underlying economic data continued to reflect structural resilience and persistent pricing pressures in the United States. Proprietary macroeconomic models began tracking a shift toward a "high-inflation, high-growth" regime. Despite hopes for a cooling economy, the U.S. economic pulse remained robust, meaning that any subsequent supply shock would hit an economy already operating at or near capacity.

The Federal Reserve Policy Review (June 16-17)

The Federal Open Market Committee (FOMC) convened for its policy meeting. While the public statement emphasized data-dependence, the internal minutes—released weeks later—revealed a committee deeply divided on the inflation trajectory, split between those favoring preventive hikes if inflation broadened and those advocating for patience or cuts if pricing pressures abated.

The Resumption of Hostilities (Early This Week)

The diplomatic progress of the preceding weeks was undone when both U.S. and Iranian forces engaged in a series of military strikes in the Gulf. The news sent immediate shockwaves through commodities desks, causing crude oil to surge and triggering a corresponding sell-off in U.S. Treasuries, pushing yields upward.

The Market Consolidation (Thursday)

After the initial shock, markets staged a partial recovery. Trading on Thursday saw a moderate pullback in both energy prices and bond yields. This stabilization reflected a wait-and-see approach by institutional investors, rather than a belief that the crisis had been resolved. On the same day, senior Federal Reserve officials publicly acknowledged the complex, multi-layered risk environment now facing the central bank.

Supporting Data: Inflation Nowcasting and Regime Shifts

The sudden return of geopolitical risk has complicated what was previously expected to be a relatively straightforward disinflationary trend. To evaluate the potential economic fallout, analysts look to a combination of public forecasting models and proprietary trend trackers.

The Cleveland Fed Inflation Nowcast

Prior to the latest round of military strikes, forward-looking indicators suggested that U.S. inflation was on the verge of a meaningful step down. The Federal Reserve Bank of Cleveland’s widely followed Inflation Nowcasting model had anticipated that pricing pressures would begin to ease starting with the June consumer inflation report, with the downward trend projected to continue into July.

Cleveland Fed Nowcast Projections (Pre-Strike Baseline vs. Post-Strike Risks)

----------------------------------------------------------------------------

Period Pre-Strike Baseline Expectation Post-Strike Risk Factors

----------------------------------------------------------------------------

June Report Initial easing of pricing pressure Potential energy-driven bump

July Report Continued downward trajectory High uncertainty / shipping premiumsThe model assumed stable or declining energy inputs and a gradual normalization of global supply chains. However, the resumption of hostilities in the Gulf threatens to undermine the baseline assumptions of this nowcast by introducing higher transportation costs, increased maritime insurance premiums, and volatile oil prices back into the calculation.

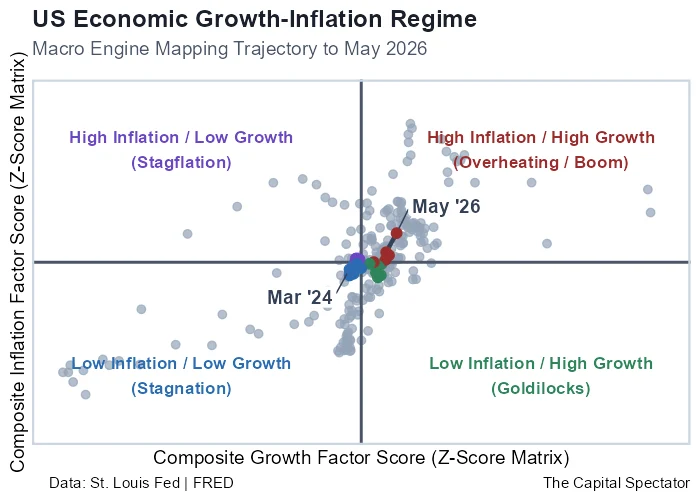

The Regime Shift Model

While public nowcasts pointed toward near-term cooling, private economic models monitored by institutional analysts were already flashing warning signs. One proprietary model utilized by The Capital Spectator to track the intersection of economic growth and inflation showed a distinct transition into a high-inflation / high-growth regime based on data compiled through May.

What made this transition particularly notable was that the rise in inflation metrics was not accompanied by a deceleration in overall economic activity. When an economy exhibits high growth alongside elevated inflation, it possesses very little margin for error. A secondary supply shock—such as an energy disruption in the Persian Gulf—is far more likely to feed directly into core consumer prices when aggregate demand is already strong, compared to a scenario where the economy is in a recessionary or low-growth phase.

Official Responses: The Federal Reserve’s Fractured Outlook

The resurgence of geopolitical instability has heightened the stakes for the Federal Reserve as it attempts to guide the U.S. economy toward a soft landing. The release of the minutes from the June 16-17 FOMC policy meeting exposed a central bank that is far from unified on its next policy steps.

The Two-Scenario Framework

The June minutes revealed that the interest-rate setting committee remains split into two distinct camps, each preparing for a vastly different macroeconomic environment:

- The Hawkish Scenario (Inflation Persistence): If inflation remains elevated, proves sticky, or begins to broaden into non-energy components of the economy, a majority of Fed officials expressed readiness to implement further interest rate hikes. This group views the risks of premature easing—which could entrench inflation expectations—as far greater than the risks of tight monetary policy.

- The Dovish Scenario (Disinflationary Progress): Conversely, if inflation resumes its steady downward trajectory toward the committee’s 2% target, most officials indicated a preference to hold the federal funds rate steady in the near term, with an eye toward eventual rate cuts later in the year to prevent the real, inflation-adjusted policy rate from becoming overly restrictive.

New York Fed President John Williams’ Assessment

Speaking on Thursday, New York Fed President John Williams addressed this divergence, emphasizing that the central bank must remain agile in the face of highly fluid global developments. Commenting on the recently released minutes, Williams noted:

"I do think [the minutes] showed that richness of these scenarios. There are certain parts of the inflation outlook that are probably maybe a little bit more benign, say on the tariffs, maybe on the energy prices, depending how that plays out. But there are other scenarios where inflation is more persistent and stays higher, which would… call for tighter monetary policy. I think that’s the right way to think about it."

Williams’ remarks highlight the Fed’s dilemma: while some structural forces (such as tariff adjustments or supply-side normalization) might offer temporary relief, external wildcards like the U.S.-Iran conflict can rapidly shift the balance of risks toward persistence, requiring a more aggressive policy stance than markets currently anticipate.

Fed Policy Alternatives Based on Geopolitical Outcomes

-------------------------------------------------------------------------

Gulf Scenario Inflation Impact Likely Fed Action

-------------------------------------------------------------------------

De-escalation / One-off Easing pressures Hold steady, eventual cuts

Protracted "Gray Zone" Sticky / Persistent Rates higher for longer

Major Energy Disruption Stagflationary spike Potential rate hike

-------------------------------------------------------------------------Market Pricing and Fed Funds Futures

Despite the hawkish contingency detailed in the minutes and the renewed tensions in the Gulf, financial markets continue to price in a relatively accommodative path for monetary policy. According to the latest readings from the Fed funds futures market:

- July 29 FOMC Meeting: Futures contracts continue to price in moderately high odds that the Federal Reserve will keep its target interest rate unchanged, reflecting a consensus that the central bank will choose to digest further data before altering its policy stance.

- September FOMC Meeting: Looking further ahead, futures pricing shows a modest shift in favor of an interest rate cut. However, this expectation remains highly vulnerable to incoming data and could quickly evaporate if the conflict in the Gulf leads to a sustained increase in energy prices throughout the summer months.

Implications: Navigating a "Brittle Equilibrium"

The breakdown of the U.S.-Iran ceasefire and the subsequent market volatility carry profound implications for global financial markets, corporate strategists, and macroeconomic policy. The primary challenge facing market participants is no longer preparing for a definitive outcome—either total war or lasting peace—but rather learning to navigate a fragile, unstable equilibrium that could persist indefinitely.

1. The Persistence of the "Gray Zone"

The events of this week serve as a stark reminder that the pre-war geopolitical calm is unlikely to return in the near future. Instead, the global economy is entering a prolonged period characterized by a geopolitical "gray zone"—an environment where formal ceasefires are signed but routinely violated, and where trade routes remain continuously vulnerable to low-level, localized military actions. For global shipping and logistics companies, this means that elevated insurance premiums, rerouting costs, and security expenses will likely become permanent structural fixtures rather than temporary operational hurdles.

2. Monetary Policy Paralysis and Volatility

For the Federal Reserve and other major central banks, a brittle equilibrium in the Middle East represents a worst-case scenario for forward guidance. Monetary policy operates with long and variable lags, requiring policymakers to make decisions based on medium-term economic projections.

When the primary driver of inflation shifts from domestic demand to unpredictable foreign policy developments, central banks struggle to make reasoned, timely policy adjustments. If the Fed cuts rates to support a softening domestic economy just as a new round of Gulf strikes sends oil prices higher, it risks reigniting stagflationary dynamics. Conversely, keeping rates elevated to combat energy-driven inflation could unnecessarily damage the domestic labor market.

3. Corporate Strategy and Capital Allocation

For multinational corporations, the combination of high borrowing costs and geopolitical instability demands a reassessment of capital allocation strategies:

- Supply Chain Diversification: The vulnerability of primary maritime trade routes in the Middle East will accelerate the trend toward nearshoring and regional supply chain redundancy, even if it results in higher structural production costs.

- Hedging Programs: Corporate treasury departments are likely to increase their hedging activities in energy and currency markets to protect profit margins against sudden geopolitical shocks, adding to overall operational overhead.

- Cautious Capital Expenditure: Faced with highly uncertain funding costs (via volatile Treasury yields) and unpredictable energy inputs, corporate leadership may adopt a more conservative approach to major capital investments, potentially slowing long-term productivity growth.

4. Investment Portfolio Positioning

For institutional investors, the transition to a high-inflation, high-growth regime punctuated by geopolitical shocks requires a defensive realignment of portfolios. Traditional balanced portfolios (such as the standard 60/40 asset allocation) may underperform in an environment where stock-bond correlations turn positive due to inflation fears.

In this context, real assets—including energy commodities, infrastructure, and inflation-protected securities—are poised to attract increased capital inflows as investors seek tangible hedges against persistent pricing pressures. At the same time, the persistent uncertainty ensures that cash and short-duration instruments will remain highly valued for their liquidity and lack of duration risk.

Conclusion

The wild card in the global macroeconomic outlook remains Iran, and it is likely to remain so for weeks, months, or even years to come. With no clear diplomatic path out of this geopolitical box in the near term, global markets will continue to struggle to find a comfortable baseline. Until a more permanent and enforceable geopolitical equilibrium is established in the Gulf, the path to lower inflation will remain uneven, keeping both the Federal Reserve and global investors on high alert.